Nomura Exposes The Fed’s Imminent “Mega-Shift” – Beware Quad Witch & “Untethered” Markets

“This is a big deal,” warns Nomura’s Charlie McElligott – a man not known for hyperbole – as he reflects on the sudden, dramatic changes occurring in the very deepest levels of plumbing of the world’s supposed most-liquid markets.

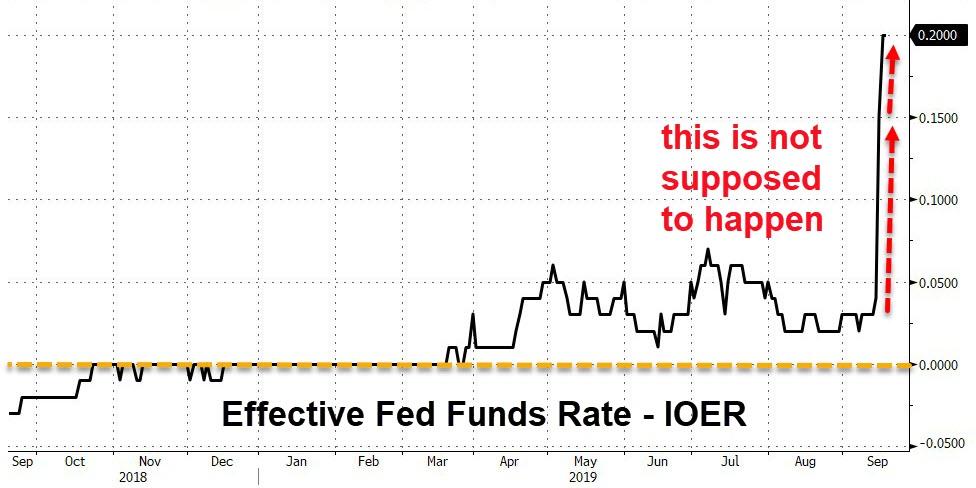

Another massively over-subscribed repo liquidity injection this morning, coupled with The Fed’s dramatic loss of control of rates suggest what McElligott calls a “potential mega-shift” in policy from The Fed.

Source: Bloomberg

Nomura Chief Economist Lew Alexander shifted his call for today’s FOMC meeting to include:

An announcement that the Fed will resume the expansion of the balance sheet again in coming weeks (in addition to a 25bps cut and likely announcement of ongoing “as needed” repo transactions in order to maintain short-term interest rates within a range that is consistent with the target range for funds rate—however, we still do NOT anticipate an imminent announcement of a “Standing Repo Facility” nor another lowering of IOER relative to the top of the FF target range today…while we also expect the dots to show no further rate cuts at this juncture, despite our “house” call for one more cut in either Oct or Dec)

McElligott’s Bottom line:

Due to the acute nature of the $funding stress dynamic in recent days, I believe the delta of a Fed “balance sheet expansion” headline today (one which would begin imminently) is significantly underpriced in the market and risks catching investors “off guard”.

The market’s “muscle memory” in the post-GFC period has condition many participants into believing that “balance sheet expansion = QE” and risks a “BULLISH risk-asset sentiment shock” (FWIW, “BS expansion = QE” is NOT actually the case per se, as what we think the Fed plans to do is much more “QE-Lite” in order to offset the Reserve depletion dynamic—NOT inject incremental liquidity “above and beyond” to actually “pump up” Reserves).

However, we also think that the Fed may more clearly signal expectations for only one more cut after today’s expected 25bps cut as well; this dynamic could risk a “hawkish” market response in Rates – and as we have seen over the course of September, the bearish Rates reversal has triggered massive “knock-on” into US Equities themes, as “Momentum” became a pure “Long Duration” expression over the course of the year.

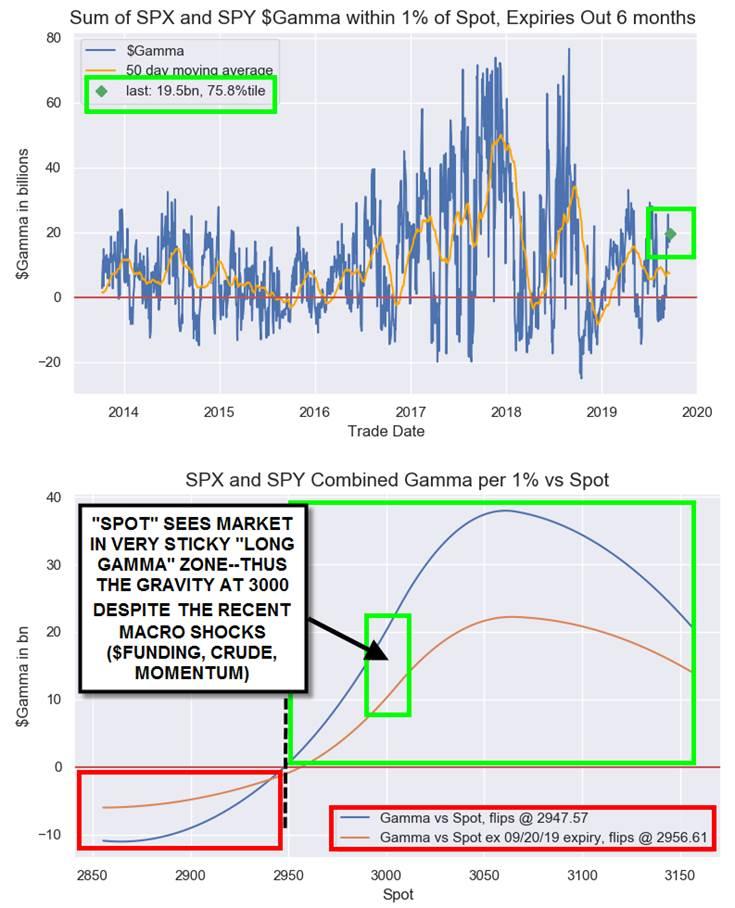

Regardless, the “risk” today is that IF we get that 1) “Fed balance sheet expansion” headline (and in imminent fashion), the Equities market risks an “overly-bullish” interpretation (QE-Lite, NOT QE outright NEW liquidity injection to add incremental reserves “above and beyond”) which in conjunction with 2) so much $Gamma coming-off following this Friday’s Op-Ex (and too, potential for an “Equities positive” VIX settlement print this morning) which acts to “untether” currently very “sticky” Stocks and 3) Low Net exposures / dour Sentiment, I see capacity where we could slingshot to the upside in Stocks, and fast (have to note the $5.2B of $Gamma at 3025, and $7.5B of $Gamma at 3050).

Why this potential mega-shift from Fed?

-

We believe that the Fed has to take a more impactful action on account of the stunning nature of the $funding squeeze in recent days into today’s FOMC announcement, where now we believe that the Committee has been forced into a more urgent stance to address the downward pressure on banking system Reserves, as recent events further exposed the structural problems in US money markets

-

This obviously too comes after having to take outright “emergency” actions yesterday (and again today), as the FRBNY had to conduct short-term repo operations to inject new liquidity into the banking system for the first time in over a decade in order to drive down the recent spike in short-term funding rates ($53B take-up yday, up to $75B today although we think there would be demand for nearly twice that)

So what does it all mean?

-

I believe that the majority of “risk” investors are set to be caught “flat-footed” upon potentially hearing of an announcement on “FED BALANCE SHEET EXPANSION,” which is obviously a “loaded” statement from the perspective of the decade-long conditioned “muscle-memory” that has been embedded in markets (and thus, investor behavior) during the post-GFC period—i.e. “liquidity IN, risk ON” (“Spooz and Blues” of the original QE era)

-

A move to expand the balance sheet (or even resume QE outright) has always, of course, been considered a “down-the-road” / “break glass in case of emergency” option in the event of recession risk escalation…but has not been part of the “NOW” vernacular

-

But due to the urgent $funding dynamic as per dysfunctional money market behavior in recent days, we believe that the time-line has been accelerated

-

FWIW, this “balance sheet expansion” can be enacted quickly, in the sense that we simply expect the Fed to effectively “upsize” the already-resumed asset purchases being conducted (restarted last month in order to offset the runoff of the existing UST and MBS securities in the Fed portfolio)

-

The thing is, this action (as we expect it) are far more “QE-Lite” than probably what the majority of investors may misinterpret as a resumption of outright “QE” – many market participants do not realize that the balance-sheet expansion was a natural dynamic PRE-crisis, as it rises alongside the amount of currency in-use

-

Most importantly and as of “right now,” the goal is to stop the shrinkage / offset the draining of Reserves…and NOT necessarily introduce (“pump”) NEW incremental Reserves above and beyond the “offset” level

-

Nonetheless, from a “stock versus flow” perspective, this matters MASSIVELY in my eyes, as it is about a TRAJECTORY or “impulse” change of the BS (“flow”) and not the absolute size of the BS (“stock”)—thus is likely to be interpreted “bullishly” for Risk assets

Market permutations—not linear:

The TRILLION DOLLAR QUESTION today is this: if our expectations for the Fed are correct today, how does the market respond to a potentially MIXED-MESSAGE where 1) balance sheet is set to be imminently expanded again via larger POMOs (and liquidity is being injected to offset this acute Reserve depletion) YET against a backdrop where 2) the market’s very dovish expectations for a deeper Fed easing-path may now be reassessed / re-priced “lower”?

-How things go “hawkish” (Yields Up / Rates sell off = More “Momentum” unwind in US Equities “Duration” trade unwind, i.e. more “Cyclical Value” over “Secular Growth” and “Defensives”):

-

It is possible that in some ways, the idea that “balance sheet expansion” may “only” be commensurate to simply expectations of increased issuance, then you could get a “hawkish” market response (although we will not get that level of detail today)

-

Obviously too, as the STIRs market has been pricing-in nearly 100bps of CUTS over the next 1Y window…a powerful “shallowing-out” message from the Fed on those aggressive easing expectations to something closer to only 50bps (today and again in either Oct or Dec), you too could get a de-facto “tightening” on the disappointment

-How things go “dovish” (Yields lower / Rates rally = resumption of US Equities “Momentum” rally as the “Duration” trade reaccelerates, i.e. Secular Growth and Defensives over Cyclical Value)

-

Markets hear “imminent BS Expansion” and think “outright QE” muscle-memory—regardless of Fed rate path disappointment risk, which is subject to economic data trajectory from here anyhow

* * *

Finally, McElligott points out that the timing of this potential Fed policy inflection development is particularly significant in the sense that Equities are likely about to become “untethered” by massive “Long Gamma” impact on markets in recent days, which have kept markets incredibly “sticky” despite a number of “shock” market moves ($Funding, Crude, Equities Momentum) and “shock” geopolitical developments (no big deal, just an Iran proxy-war strike into the heart of Saudi on a direct attack of 5% of the world’s Crude output) in recent days.

We also believe on the desk that there is a likelihood for VIX to get hit into this morning’s settlement, which can then sling-shot Equities in standard second-order fashion.

This new “Fed as macro catalyst” in the form of a BULLISH SENTIMENT SHOCK for risk-assets could then in fact override any negative seasonals, and act as the next wave up to those lumpy strikes at 3025 / 3050.

This is important then, as on the Index level, US Equities are nearing the “unshackling” of significant Dealer “Long Gamma” grip from “S&P 3000” as we approach Friday’s Quad Witch / serial op-ex: we anticipate ~32% of $Gamma to come-off thereafter.

Tyler Durden

Wed, 09/18/2019 – 10:17

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com