“This Is An Entirely Different Bubble” – Veteran Short-Seller Warns “Central Banks Are Losing Control”

Authored by Christoph Gisiger via TheMarket.ch,

In an in-depth conversation with The Market, Kevin Duffy, the head of hedge fund Bearing Asset Management, reveals where he sees the most dangerous excesses and which stocks look attractively cheap in today’s environment.

All is good. The trade war between China and the United States comes to an end, the global economy has weathered the worst, and central banks are making sure that markets continue to go up. This is the scenario currently shaping the consensus.

Kevin Duffy remains skeptical. The experienced short seller warns that the super easy monetary policy is getting less and less effective.

Although it’s been a brutal year for short sellers, Duffy is convinced his time will come soon. In this in-depth conversation with The Market, he explains why he’s betting against stocks like BlackRock and MSCI – and which names are on his buy list.

Mr. Duffy, investors are in «risk on» mood again: concerns about a global recession are waning, the S&P 500 is at record levels. What’s your take on financial markets?

To me, it’s interesting how everything is out-of-sync: You have the bond market going down, the stock market going up and gold being sort of all over the place. I think central bankers are already starting to lose control as the recent weakness in bonds shows. Just look what’s happening with the 100-year Argentine bond: It has been cut in half since August.

In the US, the yield on ten-year Treasuries is up more than 40 basis points since late August. What’s behind the recent weakness in the bond market?

I think it’s exhaustion. This year, we’ve had this big sea change in terms of the central banks going back to easing and being more accommodative. Yet, the bond market is basically saying: no more! Easy monetary policy is not having the same stimulative effect as it had in the past.

You have been warning about a gigantic bubble in the bond market for some time now. What are the reasons for the excesses in fixed income?

Bill Bonner has a good quip where he says: «When it comes to science and technology, man learns, but when it comes to love, war and finance, he makes the same mistakes over and over again.» The big mistake of our times is the great monetary experiment which started in August 1971 when the US went off the gold standard. Every bubble has a belief system, a unifying narrative. This time it’s that the central bankers are all powerful.

What do you mean by that?

It’s this idea that there is a free lunch when it comes to printing money. That’s what Modern Monetary Theory is all about: We can have our cake and eat it, too. We don’t have to feel the pain of a recession or the pain of a severe bear market. Anytime we get close to a downturn, central banks can just print money. Of course, we know that’s sheer nonsense. There is no free lunch. Polices like negative interest rates and Quantitative Easing are doing damage to the underlying economic engine. They misallocate capital, discourage thrift and promote fast money over slowly building wealth. At the end of the day, central banks are not all powerful. They are not immune to the laws of economics.

What does that mean for investors?

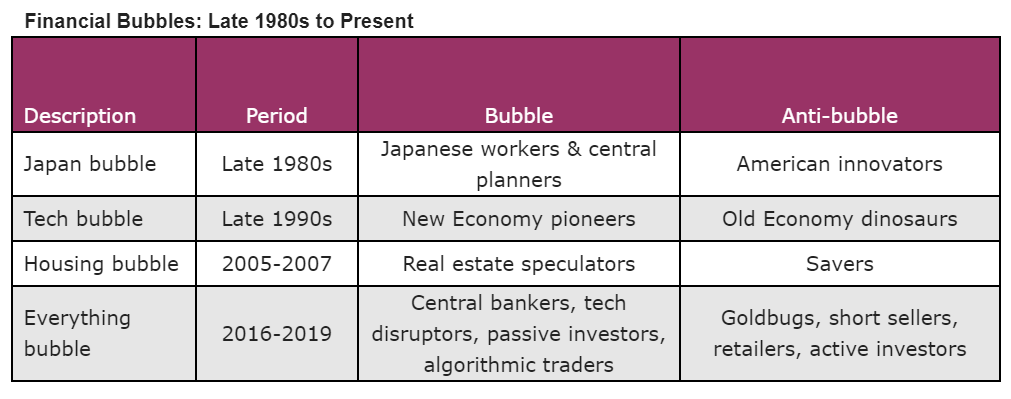

Let’s go back to the last couple of bubbles and compare them to the current one. We know that the seeds of these bubbles are artificially low interest rates. The last two bubbles were sector specific: You had the tech bubble and then the housing and credit bubble. But this one is an entirely different animal. This time, the center of the bubble is the bond market. You can even say at its core is the sovereign debt bubble. Then, you have all these other bubbles at the periphery: the high yield bubble, corporate bonds, auto finance, large cap technology, passive investing, private equity – bubbles everywhere. That’s what we’re looking at: Something on a much greater scale than anything we’ve seen before.

Since the financial crisis, we went through similar growth scares before. Each time central banks printed more money and a global recession was avoided. Why do you think it’s different this time?

With $16 trillion of the world’s bonds priced at negative yields a few months ago, it felt like all of this policy stimulus into the bond market had reached the climactic point. Since then, bond investors have started feeling some pain. One of the signatures of this bubble is the price insensitive buyer, with central bankers at the top of the list. The idea is that if the markets are on autopilot you might as well get rich by front running the central bankers and the index investors who are just blindly buying the index. It’s this narrative that we have a massive steamroller in terms of monetary policy and easy money is there for the taking. But beware the old saying about picking up pennies in front of a steamroller.

Then again, interest rates have been declining for almost four decades. Why do you think we’re at an inflection point?

Besides the absurdity of creditors paying for the privilege of lending money to governments, we’re seeing wild disconnects typical of major inflection points. In this regard, I think a lot about what happened in the late 1970s and early 1980s. At that time, you had severe price inflation and Fed Chairman Paul Volcker coming in to try to break the back of that. The first sign of a change in sentiment was the gold bubble starting to unwind in the spring of 1980. Yet, the stock market floundered and the bond market continued to decline into September of 1981. In other words, investors ignored the early signals of disinflation. The gold market was telling them that something was changing fundamentally. But at first, the other markets were completely disconnected. Then, the bond market started to get in sync and rally because it sniffed out that something was changing. The stock market continued to go down for another eleven months before it turned. That’s a classic example of these disconnects.

How is it going to play out this time?

My thesis is that when this bubble bursts, gold should rally, while bonds and stocks should crash. Against this backdrop, it’s remarkable that gold seems to have bottomed right around late April when Bloomberg BusinessWeek came out with its «Is Inflation Dead?» cover. Yet, this signal from gold was widely ignored and we got this blow-off in the bond market. Since this crazy rally peaked in August, we’ve seen a pretty good decline in bonds. Maybe this is telling us that a change is afoot. Yet, the stock market is breaking out to new highs. These markets can just disconnect for a while and it looks like stocks will be the last to get in line.

Couldn’t the recent rally in stocks and the decline in bonds also be a signal that the worst of the global slowdown is behind us and the economic picture is improving?

I think that’s not really the case. That’s not what the economic evidence is showing. We’re ten years into a recovery. It’s not like we went through an economic trough and now we’re just going to have a classic business cycle where the economy starts to recover and rates go up. Something different is happening.

What is happening?

I tend to focus on things like the fact that we have all this easy money which went into malinvestments. To me, that’s more of a forward look compared to, let’s say, labor market statistics which are backward looking. Also, I do a lot of bottom-up work by looking at companies. There, it’s fairly obvious what’s going on: You see growth rates coming down pretty much across the board. Take a look at Apple’s numbers, for instance: Annual gross profits are down over the past twelve months, yet the stock is up close to 70% year-to-date.

What do you mean when you’re referring to malinvestments?

We’re starting to see what’s behind the curtain in terms of the venture capital markets ecosystem. When these unicorns like Uber were still private, there was a tendency to assume they had substance. Now that these companies are under the light of public scrutiny we can see that the emperor is not wearing any clothes. For example, look at SoftBank’s recent $6 billion loss from the WeWork debacle and Uber racking up $20 billion in losses over the past five years. As short sellers, we were thrilled by the prospect that WeWork would go public and we’d get an opportunity to short it. The cracks in the IPO market are telling us that there are limits to easy money. That’s the common theme: we’re getting exhaustion.

In the business of short selling, you are a battle-proven veteran. How are short sellers doing these days?

I have never been through anything like this. As the ultimate price discovery agents fighting a market on auto pilot, our tiny corner of the market has been decimated. It’s been an absolutely brutal year. As of the end of October, inverse Exchange Traded Funds made up only 0.29% of total ETF assets. By comparison, in 2010, this was at 2.35%.

Very few short targets have unravelled this year. At Bearing Asset Management, we’re not only shorting stocks but bonds as well – and the bond market has been even worse up until recently. This Everything Bubble is much more difficult to short than a «normal» bubble since it’s so broad-based and persistent. I’m sure that will change. But honestly, as somebody who’s been doing this for a while, there are times I wish I had never discovered short selling. That’s what a major top feels like.

That said, where do you see the most promising short opportunities?

In auto finance, in the passive bubble and in money losing companies like Tesla or Carvana. These are a few of the themes we’re betting against. But we’re scaling back and trying to stay focused on our best ideas. It’s kind of a circle the wagons, bunker mentality at this point.

What makes this market so difficult for short sellers?

For instance, as a way to bet against the passive bubble, we’re short BlackRock and MSCI. These companies have benefited from rising asset prices and have been able to take in a good portion of the inflows into passive strategies. But they have given most of these benefits back because of fee compression as a result of investors gravitating toward lower cost alternatives. It’s amazing how much of a headwind this has been, yet investors are so far unfazed. BlackRock is up close to 25% year-to-date and MSCI around 65%. For short sellers like us this has been frustrating because I think we’ve gotten a lot of the fundamentals right.

You’re also investing on the long side. Where do you see attractive investments?

Jean-Marie Eveillard, the highly respected value investor who has been in this business for decades, once said that there has been only one market where he was not able to find any value: Japan in the late 80s. There is always value when you look hard enough. One of the things we know from past bubbles is that you often get anti-bubbles. This was clearly the case in the year 2000 when you had the new economy bubble on one side, and the old economy anti-bubble on the other side. When tech stocks peaked in March of 2000, a lot of the «boring» value stocks bottomed at the same time.

Where do you find anti-bubbles today?

One of the reigning narratives is that Amazon is going to put all retailers out of business. This may be true in a lot of cases, particularly in the mall space. But there will be survivors who benefit from their competitors going bust. Many of these names went through massive bear markets over the past three years. That’s why it may pay off to rummage through the junk pile in the retail sector.

Any specific names you have in mind?

American Eagle. They compete in the teen apparel area. Aéropostale, one of their main competitors, is bankrupt and in liquidation. Aéropostale was a poster child for financial engineering: They once had a great balance sheet and were doing well, but squandered it all on buybacks. When the business started to go sour, they didn’t have the balance sheet to weather the storm. In contrast, American Eagle has come through unscathed while everybody else was falling by the wayside. Now, they have less competition. Also, with their Aerie concept they compete with Victoria’s Secret and are trying to reach an audience that doesn’t have the perfect supermodel body. It’s one of the most successful concepts in retail, and yet it’s wrapped in this older mall-based company that has this «Amazon roadkill» stigma. Another interesting company is Urban Outfitters. The stock is up close to 50% since mid-August, so it’s not quite as cheap as American Eagle. But it’s a high-quality retailer and clear survivor.

Where else do you spot opportunities on the long side?

I’m a little bit hesitant to bang the drum for resource-based stocks and commodities because I think we’re going into a global recession. But there are some interesting areas we’ve been poking around a little bit. For instance, food-related commodities like fertilizer tend to be more defensive as opposed to things that are more sensitive to the economy like copper.

How about gold?

Precious metals and mining stocks are another example of an anti-bubble: Faith in central banking is at the heart of this bubble and precious metals are the inverse of faith in central banks. So we like gold and gold stocks. Admittedly, gold mining is not a good business since it’s very capital intensive and whenever there is a boom there tends to be tremendous waste. But if gold goes up further, these companies are going to benefit.

Are there any other bubbles or anti-bubbles investors should be aware of?

There is also a socially responsible investing aspect – along the lines of environmental, social and governance factors – to this bubble as the Millennials start to take over investing functions. It’s a filter that you have to be aware of. Certainly, Tesla appeals to this ESG crowd. Another example is Beyond Meat, which went public in early May and shot up nearly tenfold in less than three months. At its peak, the company was valued at $15 billion with just $200 million in revenue and barely about to turn a profit. Large bureaucratic companies in general have become bastions of political correctness willing to cater to the ESG crowd. On the other side, if you’re a small entrepreneurial company, you’re not hiring based on diversity quotas. You’re hiring the most competent people you can find since you don’t have time to collect a bunch of worthless statistics. I feel this will be the gift that keeps on giving for contrarian investors: You want to look for stocks that don’t neatly fit into the ESG screens. The obvious example is the energy sector, especially natural gas exploration and production stocks, which are severely depressed. Fossil fuel investments are strictly verboten in the ESG playbook. That’s an opportunity.

* * *

Kevin Duffy is a battle-proven veteran in the risky business of short selling. He co-founded Bearing Asset Management in 2002. He and his partner were vocal critics of the 2007 credit bubble, successfully shorting many of its most aggressive players including Countrywide Financial and Bear Stearns. Prior to Bearing, Kevin co-founded Lighthouse Capital Management and served as Director of Research from 1988 to 1999. He chronicled the excesses of the Japan and technology bubbles of the late 1980s and the late 1990s. Kevin Duffy bought his first stock at the age of 13. He has a passion for Austrian economics and is the author of the popular Notable and Quotable blog.

Tyler Durden

Wed, 11/20/2019 – 10:45

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com