Lebanon Lost $10BN In Bank Deposits Since August; Bond Yields Soar Past 100% Into “Venezuela Territory”

Protest-racked Lebanon over the past month has seen its banks opened for only half that time. First, the deteriorating security situation since Oct. 17 forced their closure for two weeks, with the country’s association of banks then fearing a run on deposits, and after a brief opening staff went on strike, citing personal safety at the hands of angry citizens demanding their cash from the “thieving” banks (literally in some cases involving clients with guns).

Banks reopened Tuesday after the latest week-long closure interval, though with security personnel-enforced restrictions on hard currency withdrawals and transfers abroad.

This as Lebanese parliament was prevented from holding a session Tuesday when protesters blocked the outside of the building, forcing SUVs carry Lebanese MPs to turn back when demonstrators rushed their convoy, also amid gunfire ringing out. Parliament postponed the session indefinitely, according to Reuters.

{kind=link}

And now the predicted and long expected tidal wave capital flight, despite dubious “silver bullet” attempts at imposing controls, is underway.

Lebanon has lost over $10 billion of its bank deposits since August, Bloomberg reports, citing The Institute of International Finance (IIF). In a new report, IIF chief economist Garbis Iradian writes, “Half of this decline represents withdrawals from the country, while the other half remains as cash under mattresses in Lebanon.”

Video showing protesters chasing away members of parliament as they attempted to approach the building Tuesday:

An MP’s convoy of 3 cars tries to drive past protestors blocking the road, who then try to stop the car & throw bottles and other small objects

One bodyguard opens the window & shoots warning shots into the air — then appears to detour.

(Video via an eyewitness)#Lebanon pic.twitter.com/KXwKYVWmbq

— Kareem Chehayeb | كريم (@chehayebk) November 19, 2019

https://platform.twitter.com/widgets.js

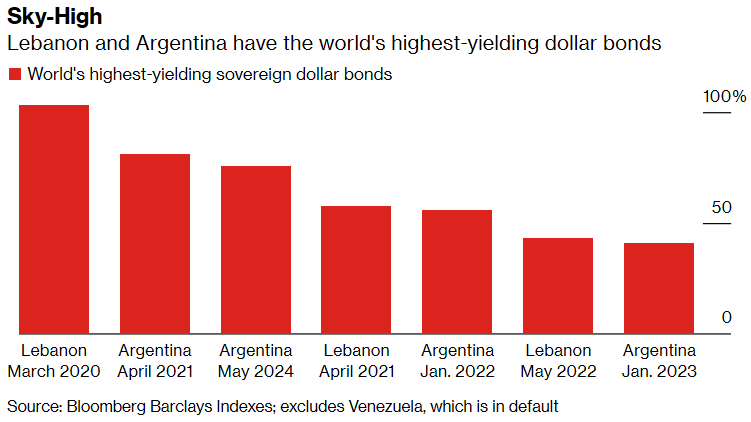

Further alarming is that yields on some of the country’s dollar bonds are now entering socialist Venezuela territory, Bloomberg writes:

The political crisis in Lebanon has sent yields on some of its dollar bonds into triple digits.

Rates on the government’s $1.2 billion of notes maturing in March next year have climbed 28 percentage points this week to 105%. They were at 13% five weeks ago, just before the start of protests that led to the resignation of Prime Minister Saad Hariri and exacerbated the nation’s economic woes.

Dollar yields reaching 100% is extremely rare, territory which debt-strained Argentina has yet to even enter.

“With Lebanon viewed by many bond traders as a default waiting to happen, cash prices have become more important than yields as they factor in potential recovery rates,” the Bloomberg analysis continues.

“That’s inverted the government’s curve and distorted yields at the shorter end. The price of Lebanon’s 2020 debt is 77 cents on the dollar, while that of its April 2021 securities is 56 cents,” the report adds.

Though Lebanon can boast it’s never defaulted on its sovereign debt — now standing at $86 billion, or 150% of GDP and with the finance ministry vowing it can pay off a $1.5bn bond maturing this month — it’s never seen a crisis of this magnitude, causing economists to urge Beirut to pursue a debt restructuring plan as the default risk worsens.

{kind=link}

Given that most of the country’s debt is held by local banks, and with the scene of police literally standing at teller windows having to enforce controls and restrain patrons from removing all of their own money, a vicious cycle has clearly begun.

Tyler Durden

Thu, 11/21/2019 – 02:45

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com