European Central Bank Has One Item Left In Its Toolkit: Dual Rates

Authored by Eric Lonegren via BondVigilantes.com,

There is a widespread assumption that the European Central Bank – like other major central banks – has reached the limits of monetary policy, and that the best we can hope for with Christine Lagarde’s reign is political astuteness in cajoling reluctant politicians to embrace a fiscal stimulus.

This is not the case.

As Ms Lagarde prepares to launch a strategic review of the ECB’s policies and objectives, she has a final item left in the toolkit: dual interest rates.

In practice, this entails the central bank targeting different interest rates for loans and deposits. Such loans can also be restricted to specific sectors, such as renewable energy. The policy would be more effective than quantitative easing, forward guidance or negative interest rates. It would provide a powerful monetary stimulus and could be used to turbo-charge Europe’s Green Deal.

The effects of dual interest rates are easiest to understand in contrast to standard policy. Typically, when a central bank reduces interest rates we expect this to boost spending in the economy through three basic effects:

-

Interest rates fall for households with mortgages;

-

asset prices rise, making people feel wealthier; and

-

the cost of borrowing for companies falls, which should boost investment spending.

But serious problems emerge when interest rates are very low or negative. The interest income which savers receive collapses — weighing on spending — and bank profitability is damaged, causing many unintended consequences.

The application of dual interest rates

What would happen if the central bank raised the interest rate on deposits, and cut the interest rate on loans? Both savers and borrowers benefit. History tells us that such an approach will always raise demand.

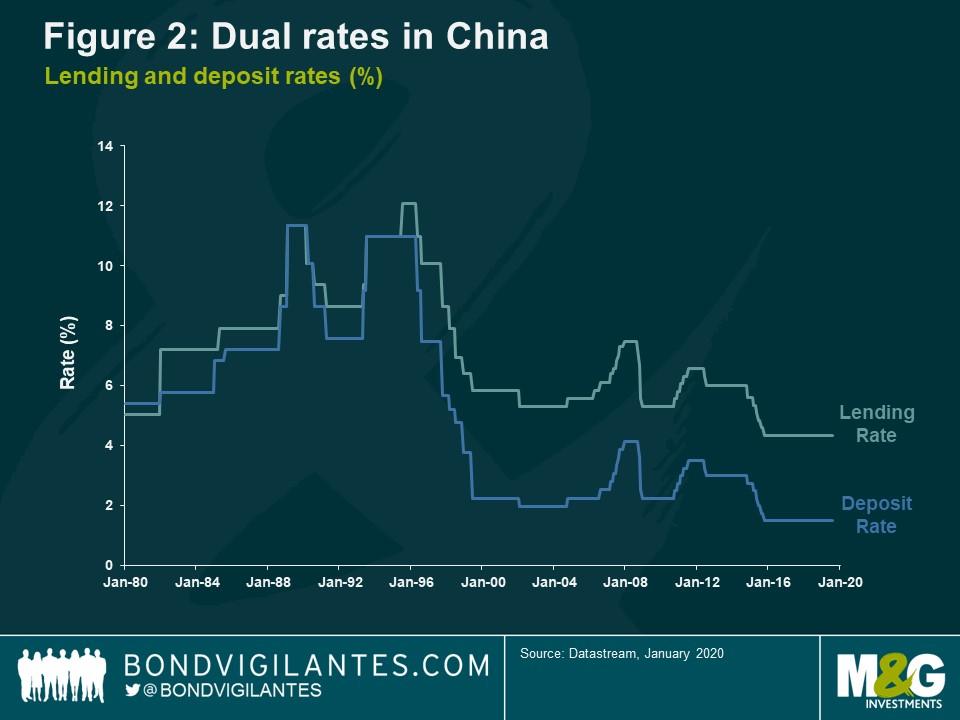

The strongest recent evidence is from the Chinese banking system in the 1980s and early 1990s (see the differential movements in figure 2, prior to more parallel shifts in recent years).

Interest rates on deposits and loans were set independently. When stimulus was required, interest rates on loans could be reduced by more than interest on deposits. In an economy with fiat money, nominal spending can always be stimulated.

Can such a policy work with a private banking system and an independent central bank? Many commentators seem unaware that in his final act as president, Mario Draghi showed precisely how it is done.

For some time now the ECB has had a method of independently affecting lending rates. Its targeted longer-term refinancing operation — or TLTRO — allows the central bank to lend to commercial banks at negative interest rates, on condition that they extend new loans to the private sector. TLTROs also exclude lending to unproductive parts of the economy, such as mortgages.

Mr Draghi’s final innovation was to introduce “tiered reserves”. This allows the central bank to set the rate of interest on the deposits that banks hold with the central bank independently of the policy rate which determines money market rates.

In one subtle gesture, the ECB in effect reduced the interest rate at which banks can fund lending to the economy and raised the average interest rate that banks receive on their deposits. This is a policy of dual interest rates.

Dual interest rates in the future

Let us consider how this policy could be extended. If Ms Lagarde needs to provide further stimulus to the eurozone due to inflation persistently undershooting the ECB’s close to 2 per cent target, she could increase the term of TLTROs to five or 10 years, at a steeply negative interest rate, say minus 1 per cent. At the same time, the bank could increase the interest rate on deposits through tiering.

Progress could also be made on how to target this TLTRO funding. Currently, the only requirement for banks to access the programme is that they use it to extend new loans, excluding mortgages. Ms Lagarde has expressed a desire to make ECB policy consistent with the eurozone policy on climate change.

TLTROs at negative interest rates should be available only to banks that are directly using the funds to finance sustainable energy investments. In one relatively simple policy move, the supposed impotence of monetary policy becomes an enhanced Green Deal.

It came as little surprise that the take-up of the recent programme was muted. For example, the current three-year TLTROs at minus 0.5 per cent are only a marginal improvement on available market-based funding. But a 10-year loan at minus 1 per cent or minus 2 per cent would be game-changing.

Dual interest rates and sustainable TLTROs should be at the heart of Ms Lagarde’s review. Monetary policy is very far from running its course. There is scope for a major shift in its power. Therein lies the challenge for the bank’s new president. She has promised openness and transparency. Being explicit about the effects, and powers, of this policy would be a great manner in which to begin.

Tyler Durden

Fri, 01/10/2020 – 05:00

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com