Platts: 6 Commodity Charts To Watch This Week

Via S&P Global Platts Insight blog,

Global gas price convergence tops this week’s pick of energy and commodities charts to watch. Plus: US LNG exports, coronavirus impact on Asian crude oil and bunker fuel trade, emerging European power market dynamics, and global steel price trends.

1. Globalized gas prices race towards rock bottom…

What’s happening? Global gas spot prices have converged again in recent weeks to the downside as the coronavirus outbreak and its impact on Chinese LNG demand adds to already very bearish sentiment across the world. Spot prices in Asia, Europe and the US have converged in an extremely narrow $1.10/MMBtu range as the global gas glut looks set to worsen amid weak demand, high storage stocks and mild winter temperatures. The JKM Asian spot price has fallen to an all-time low of just $2.95/MMBtu.

What’s next? Coronavirus has begun to weigh significantly on Chinese LNG import demand, which has been the main driver of global gas demand growth in recent years, with state-owned CNOOC declaring force majeure on some of its import contracts. With cargoes expected to be diverted to Europe, it seems likely there will be more pressure on northwest European hub prices in the coming weeks. With no improvement in global gas prices expected through 2020, the trend for price convergence looks set to continue.

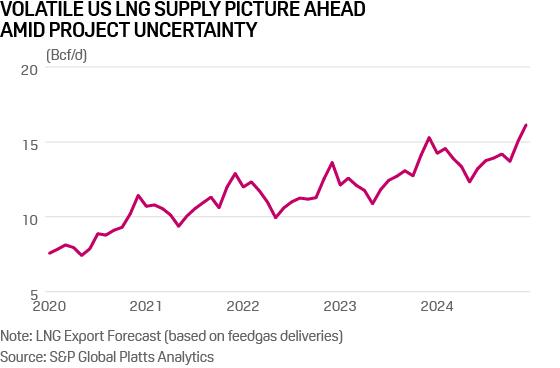

2. …setting US LNG exports on a bumpy path

What’s happening? The upward trajectory of US LNG exports is expected to stall next year before falling and rising again, leading the market on a roller-coaster ride through the middle of the decade amid uncertainty about new project start-ups, S&P Global Platts Analytics data shows. Weak prices in Asia, lower than expected demand in key markets and geopolitical concerns have been weighing on suppliers and end-users. Add in the coronavirus outbreak and a perfect storm of challenges is festering.

What’s next? Relief may depend on China’s next move. It plans to cut tariffs on imports of US crude and other products February 14, but for now is leaving duties of 25% on US LNG in place. US developers of new liquefaction projects are counting on long-term contracts with Chinese customers to help advance their terminals.

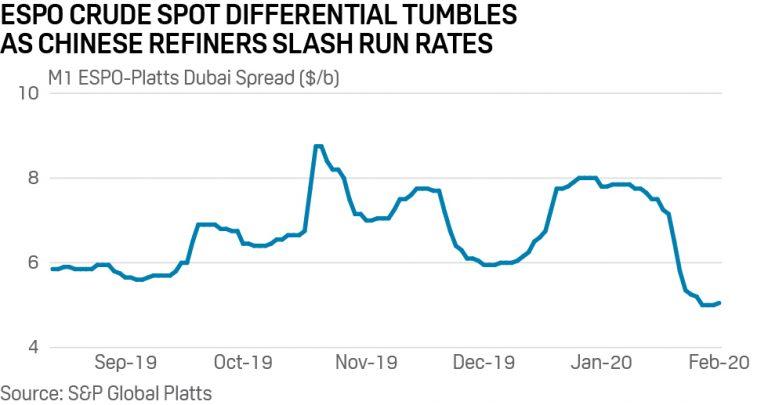

3. Chinese refinery activity drops, hitting Russia’s ESPO crude

What’s happening? China’s domestic oil demand has already drastically declined with industrial, manufacturing and construction activities coming to a halt due to the coronavirus outbreak. For example, Sinopec, the world’s biggest refiner by capacity, recently slashed overall crude throughput by about 13% and its refineries across China are currently operating at minimum run rates. Throughput levels for another state-owned refiner, PetroChina, saw sharp declines in recent weeks. Independent refiners in Shandong province have also reduced their average run rate by more than 17 percentage points from mid-January, sources told Platts.

What’s next? In the oil markets, the coronavirus outbreak continues to cast its spell on Asian Pacific crude price differentials. Far East Russian crude oil, in particular, is likely to bear the brunt of China’s economic slowdown aggravated by its outbreak, with both state-run and private Chinese refiners poised to cut imports of their favorite feedstock ESPO Blend crude amid faltering refinery throughput. Platts assessed first-month ESPO Blend crude at a premium of $4.6/b against Platts Dubai on Feb 6, marking the lowest price differential since $4.5/b on July 19, 2019.

4. Ship diversions could benefit South Korean bunker suppliers

![]()

What’s happening? In the North Asian bunker markets, bunker demand in China has fallen significantly this week as markets reopened after the extended Lunar New Year holiday, with the seasonal low demand period amplified this year by the coronavirus outbreak.

What’s next? Despite efforts by some 16 ports and port groups in China to offer exemptions and reductions in port charges in a bid to spur business, including the main ports of Shanghai and Ningbo-Zhoushan, bunker fuel traders in South Korea are expecting an uptick in demand as vessels increasingly divert from China and refuel in South Korea, where marine fuel is already available at competitive prices. Although ships en route to China were unlikely to change course mid-way, shipowners said they may consider other options for upcoming journeys. Delivered marine fuel 0.5% was assessed at $580/mt in Shanghai Thursday, higher than $550/mt in South Korea, S&P Global Platts data showed.

5. Warmer winters could reshape EU power price dynamics

![]()

What’s happening? Above-average temperatures have knocked the stuffing out of Nordic power prices, which are sensitive to the widespread use of electric heat. Reduced demand for electric heat combined with healthy hydro reservoir levels and strong wind generation to drive Nord Pool system spot prices down to a Eur17.25/MWh average in the first seven days of February – a 40% decline on month.

What’s next? In the short term, forecast precipitation in the Nordic area over the next two weeks is 50% above seasonal average, according to broker Energi Danmark, while temperatures are set to remain five degrees Celsius above average. Longer term… is this what electrification looks like? Winters are getting warmer and conventional gas-fired heat systems such as the UK’s will move towards to heat pumps and other electric-based techs. UK power prices are based on the cost of gas, in turn supported through winter by heat demand. This dynamic will ebb away as zero marginal cost renewables encroach on heat markets, UK housing stock evolves and, alas, weeks of hard frosts pass into folklore.

6. Turkish steel mills seize opportunity amid plunging scrap price

![]()

What’s happening? Prices of steel heavy melting scrap 1&2 (80:20) delivered into Turkey plunged almost 16% from mid-January to the first week in February. The product is a basic raw material for steelmaking, particularly in electric arc furnaces, and is one of the most traded scrap grades in the export markets. Prices plunged as the coronavirus outbreak weakened steel market sentiment and prices generally, and Turkish steelmakers pressured for lower prices for their key input amid slack domestic steel demand.

What’s next? A slight uptick in scrap prices at the end of last week may continue as Turkish mills seize what they perceive as an opportunity to sell more steel into export markets temporarily vacated by China due to port and other transport restrictions. Turkish mills are reportedly already increasing their steel output to plug this gap.

Tyler Durden

Mon, 02/10/2020 – 13:00

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com