Panic Sets In As “Everything Must Go”

Authored by Lance Roberts via RealInvestmentAdvice.com,

Headlines from the past three-days:

-

Dow sinks 2,000 points in worst day since 2008, S&P 500 drops more than 7%

-

Dow rallies more than 1,100 points in a wild session, halves losses from Monday’s sell-off

-

Dow drops 1,400 points and tumbles into a bear market, down 20% from last month’s record close

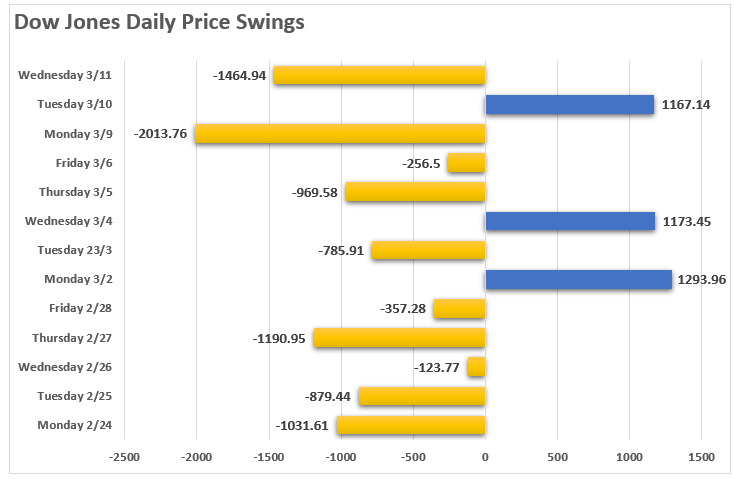

It has, been a heck of a couple of weeks for the market with daily point swings running 1000, or more, points in either direction.

However, given Tuesday’s huge rally, it seemed as if the market’s recent rout might be over with the bulls set to take charge? Unfortunately, as with the two-previous 1000+ point rallies, the bulls couldn’t maintain their stand.

But with the markets having now triggered a 20% decline, ending the “bull market,” according to the media, is all “hope” now lost? Is the market now like an “Oriental Rug Factory” where “Everything Must Go?”

It certainly feels that way at the moment.

“Virus fears” have run amok with major sporting events playing to empty crowds, the Houston Live Stock Show & Rodeo was canceled, along with Coachella, and numerous conferences and conventions from Las Vegas to New York. If that wasn’t bad enough, Saudi Arabia thought they would start an “oil price” war just to make things interesting.

What is happening now, and what we have warned about for some time, is that markets needed to reprice valuations for a reduction in economic growth and earnings.

It has just been a much quicker, and brutal, event than even we anticipated.

The questions to answer now are:

-

Are we going to get a bounce to sell into?

-

Is the bear market officially started – from a change in trend basis; and,

-

Just how bad could this get?

A Bounce Is Likely

In January, when we discussed taking profits out of our portfolios, we noted the markets were trading at 3-standard deviations above their 200-dma, which suggested a pullback, or correction, was likely.

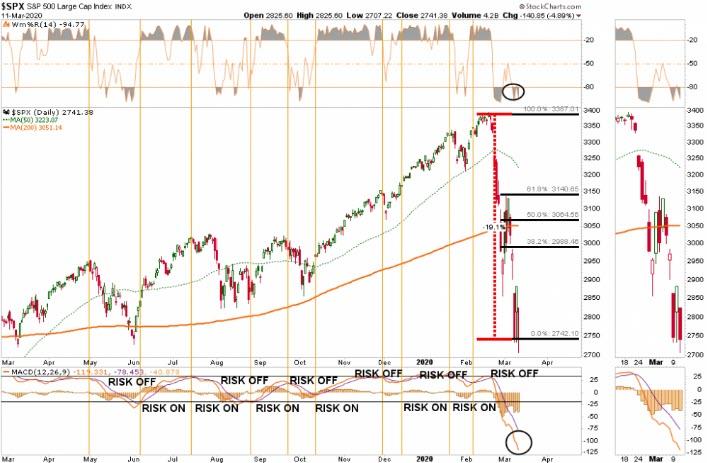

Now, it is the same comment in reverse. The correction over the last couple of weeks has completely reversed the previous bullish exuberance into extreme pessimism. On a daily basis, the market is back to oversold. Historically, this condition has been sufficient for a bounce. Given that the oversold condition (top panel) is combined with a very deep “sell signal” in the bottom panel, it suggests a fairly vicious reflexive rally is likely. The question, of course, is how far could this rally go.

Looking at the chart above, it is possible we could see a rally back to the 38.2%, or the 50% retracement level where the 200-dma currently resides. A rally to that level will likely reverse much of the current oversold condition, and set the market up for a retest of the lows.

The deep deviation from the 200-dma also supports this idea of a stronger reflexive rally. If we rework the analysis a bit, the 3-standard deviation discussed previously has now reverted to 3-standard deviations below the 200-dma. The market found support there, and with the deeply oversold condition, it again suggests a rally to the 200-dma is likely.

Given that rally could be sharp, it will be a good opportunity to reduce risk as the impact from the collapse in oil prices, and the shutdown of the global supply chain, has not been fully factored in as of yet.

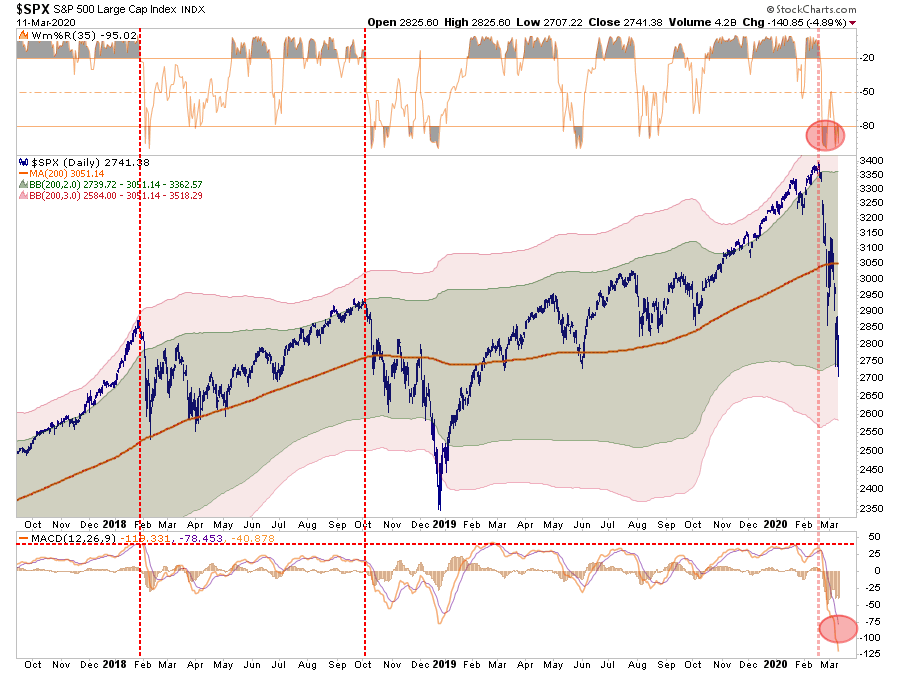

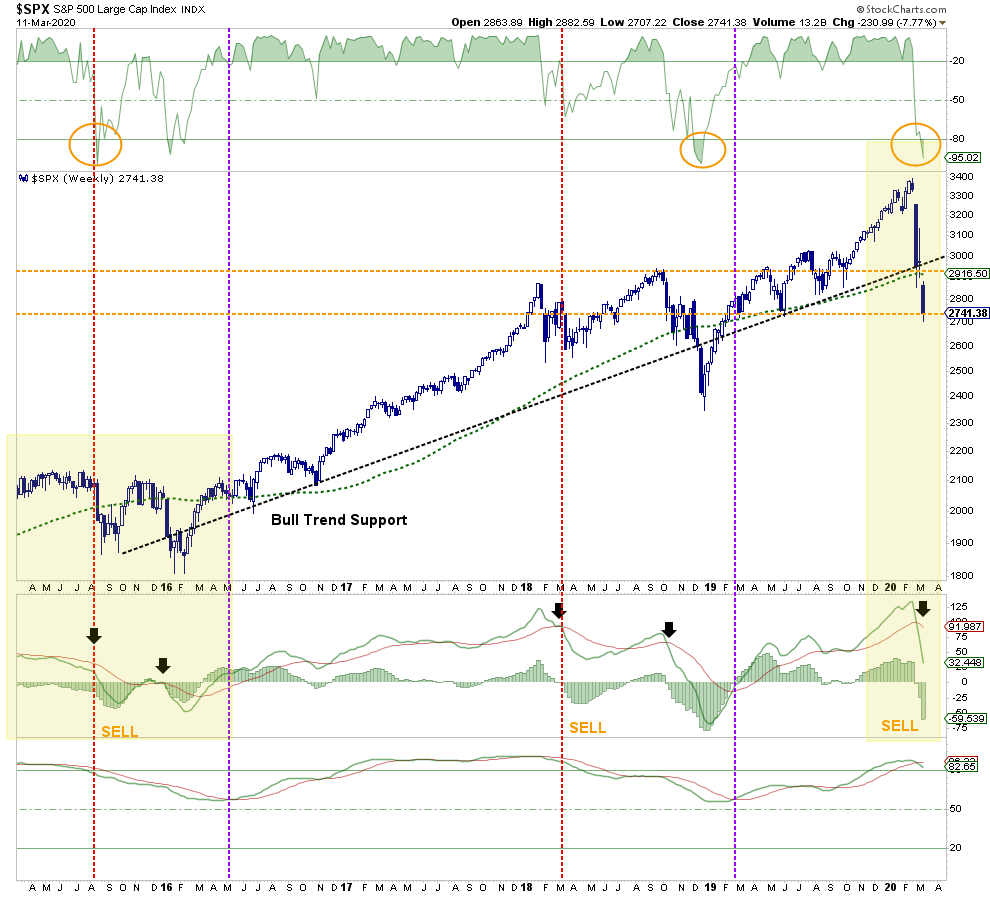

The following chart is a longer-term analysis of the market and is the format we use for “onboarding” our clients into their allocation models. (Vertical black lines are buy periods)

The triggering of the “sell signals” suggests we are likely in a larger correction process. With the “bull trend” line now broken, a rally toward the 200-dma, which is coincident with the bull trend line, will likely be an area to take additional profits, and reduce risk accordingly.

The analysis becomes more concerning as we view other time frames.

Has A Bear Market Started?

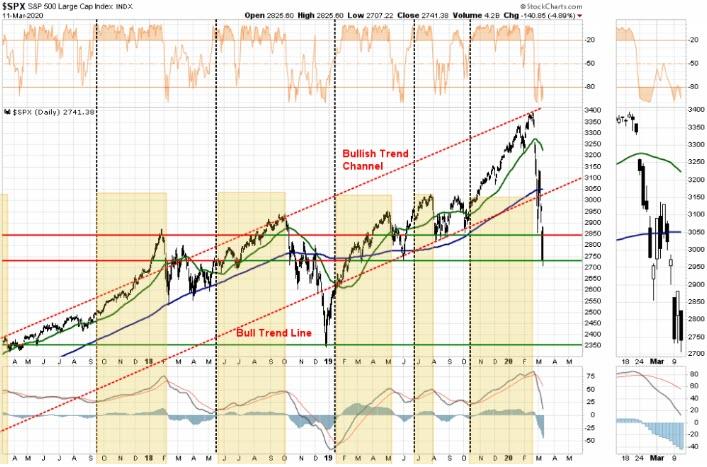

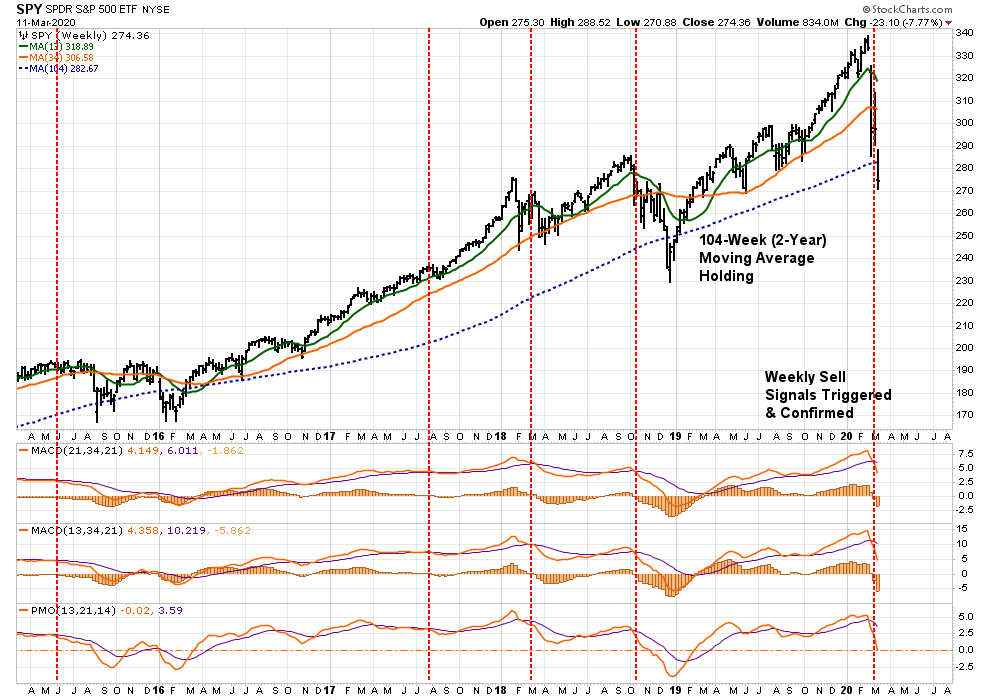

On a weekly basis, the rising trend from the 2016 lows is clear. The market has NOW VIOLATED that trend, which suggests a “bear market” has indeed started. This means investors should consider maintaining increased cash allocations in portfolios currently. With the two longer-term sell signals, bottom panels, now triggered, it suggests that whatever rally may ensue short-term will likely most likely fail. (Also a classic sign of a bear market.)

With the market oversold on a weekly basis, a counter-trend, or “bear market” rally is likely. However, as stated, short-term rallies should be sold into, and portfolios hedged, until the correction process is complete.

With all of our longer-term weekly “sell signals” now triggered from fairly high levels, it suggests the current selloff is much like what we saw in 2015-2016. (Noted in the chart above as well.) In other words, we will see a rally, followed by a secondary failure to lower lows, before the ultimate bottom is put in. If the market fails to hold current levels, the 2018 lows are the next most likely target.

Just How Bad Can It Get?

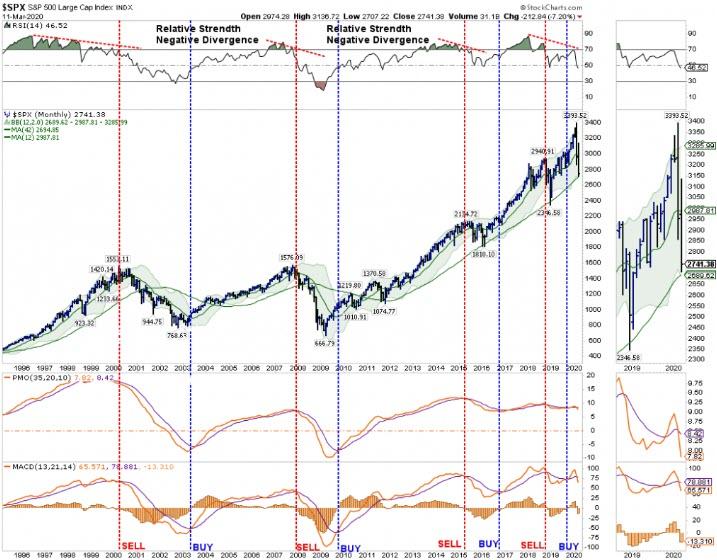

The idea of a lower bottom is also supported by the monthly data.

NOTE: Monthly Signals Are ONLY Valid At The End Of The Month.

On a monthly basis, sell signals have also been triggered, but we will have to wait until the end of the month for confirmation. However, given the depth of the decline, it would likely take a rally back to all-time highs to reverse those signals. This is a very high improbability.

Assuming the signals remain, there is an important message being sent, as noted in the top panel. The “negative divergence” of relative strength has only been seen prior to the start of the previous two bear markets, and the 2015-2016 slog. While the current sell-off resembles what we saw in late 2015, there is a risk of this developing into a recessionary bear market later this summer. The market is very close to violating the 4-year moving average, which is a “make or break” for the bull market trend from the 2009 lows.

How bad can the “bear market” get? If the 4-year moving average is violated, the 2018 lows become an initial target, which is roughly a 30% decline from the peak. However, the 2016 lows also become a reasonable probability if a “credit event” develops in the energy market which spreads across the financial complex. Such a decline would push markets down by almost 50% from the recent peak, and not unlike what we saw during the previous two recessions.

Caution is advised.

What We Are Thinking

Since January, we have been regularly discussing taking profits in positions, rebalancing portfolio risks, and, most recently, moving out of areas subject to slower economic growth, supply-chain shutdowns, and the collapse in energy prices. This led us to eliminate all holdings in international, emerging markets, small-cap, mid-cap, financials, transportation, industrials, materials, and energy markets. (RIAPRO Subscribers were notified real-time of changes to our portfolios.)

While there is “some truth” to the statement “that no one” could have seen the fallout of the “coronavirus” being escalated by an “oil price” war, there has been mounting risks for quite some time from valuations, to price deviations, and a complete disregard of risk by investors. While we have been discussing these issues with you, and making you aware of the risks, it was often deemed as “just being bearish” in the midst of a “bullish rally.” However, it is managing these types of risks, which is ultimately what clients pay advisors for.

It isn’t a perfect science. In times like these, it gets downright messy. But this is where working to preserve capital and limit drawdowns becomes most important. Not just from reducing the recovery time back to breakeven, but in also reducing the “psychological stress” which leads individuals to make poor investment decisions over time.

Given the extreme oversold and deviated measures of current market prices, we are looking for a reflexive rally that we can further reduce risk into, add hedges, and stabilize portfolios for the duration of the correction. When it is clear, the correction, or worse a bear market, is complete, we will reallocate capital back to equities at better risk/reward measures.

We highly suspect that we have seen the highs for the year. Most likely,,we are moving into an environment where portfolio management will be more tactical in nature, versus buying and holding. In other words, it is quite probable that “passive investing” will give way to “active management.”

Given we are longer-term investors, we like the companies we own from a fundamental perspective and will continue to take profits and resize positions as we adjust market exposure accordingly. The biggest challenge coming is what to do with our bond exposures now that rates have gotten so low OUTSIDE of a recession.

But that is an article for another day.

As we have often stated, “risk happens fast.”

Tyler Durden

Thu, 03/12/2020 – 10:30![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com