Seth Levine: COVID-19 Is Not The Last War

Authored by Seth Levine via RealInvestmentAdvice.com,

These are truly remarkable times in the investment markets. The speed, intensity, and ubiquity of this selloff brings just one word to mind: violence. It would be remarkable if it wasn’t so destructive. Sadly, the reactions from our politicians and the public were predictable. The Federal Reserve (Fed) faithfully and forcefully responded. Despite its unprecedented actions, it seems like they’re “fighting the last war.”

Caveat Emptor

My intention here is to discuss some observations from the course of my career as an investor and try to relate them to the current market. I won’t provide charts or data; I’m just spit-balling here. My goal is twofold: 1) to better organize my own thoughts, and; 2) foster constructive discussions as we all try to navigate these turbulent markets. I realize that this approach puts this article squarely into the dime-a-dozen opinion piece category—so be it.

Please note that what you read is only as of the date published. I will be updating my views as the data warrants. Strong views, held loosely.

The Whole Kit and Caboodle

Investment markets are in freefall. U.S stock market declines tripped circuit breakers on multiple days. U.S. Treasuries are gyrating. Credit markets fell sharply. Equity volatility (characterized by the VIX) exploded. The dollar (i.e. the DXY index) is rocketing. We are in full-out crisis mode. No charts required here

With the Great Financial Crisis of 2008 (GFC) still fresh in the minds of many, the calls for a swift Fed action came loud and fast. Boy, the Fed listen. Obediently, it unleashed its full toolkit, dropping the Fed Funds rate to 0% (technically a 0.00% to 0.25% range), reducing interest on excess reserves, lowering pricing on U.S. dollar liquidity swaps arrangements, and kick-starting a $700 billion QE (Quantitative Easing) program. The initiatives are coming so fast and so furious that it’s hard to keep up! The Fed is even extending credit to primary dealers collateralized by “a broad range of investment grade debt securities, including commercial paper and municipal bonds, and a broad range of equity securities.” Really?!

Reflexively, the central bank threw the whole kit and caboodle at markets in hopes of arresting their declines. It’s providing dollar liquidity in every way it can imagine that’s within its power. However, I have an eerie sense that the Fed is (hopelessly) fighting the last war.

The Last War

There are countless explanations for the GFC. The way I see it is that 2008 was quite literally a financial crisis. The financial system (or plumbing) was Ground Zero. A dizzying array of housing-related structured securities (mortgage backed securities, collateralized debt obligations, asset-backed commercial paper, etc.) served as the foundation for the interconnected, global banking system, upon which massive amounts of leverage were employed.

As delinquencies rose, rating agencies downgraded these structured securities. This evaporated the stock of foundational housing collateral. Financial intuitions suddenly found themselves short on liquidity and facing insolvency. It was like playing a giant game of musical chairs whereby a third of the chairs were suddenly removed, unbeknownst to the participants. At once, a mad scramble for liquidity ensued. However, there simply was not enough collateral left to go around. Panic erupted. Institutions failed. The financial system literally collapsed.

This War

In my view, today’s landscape is quite different. The coronavirus’s (COVID-19) impact is a “real economy” issue. People are stuck at home; lots are not working. Economic activity has ground to a halt. It’s a demand shock to nearly every business model and individual’s finances. Few ever planned for such a draconian scenario.

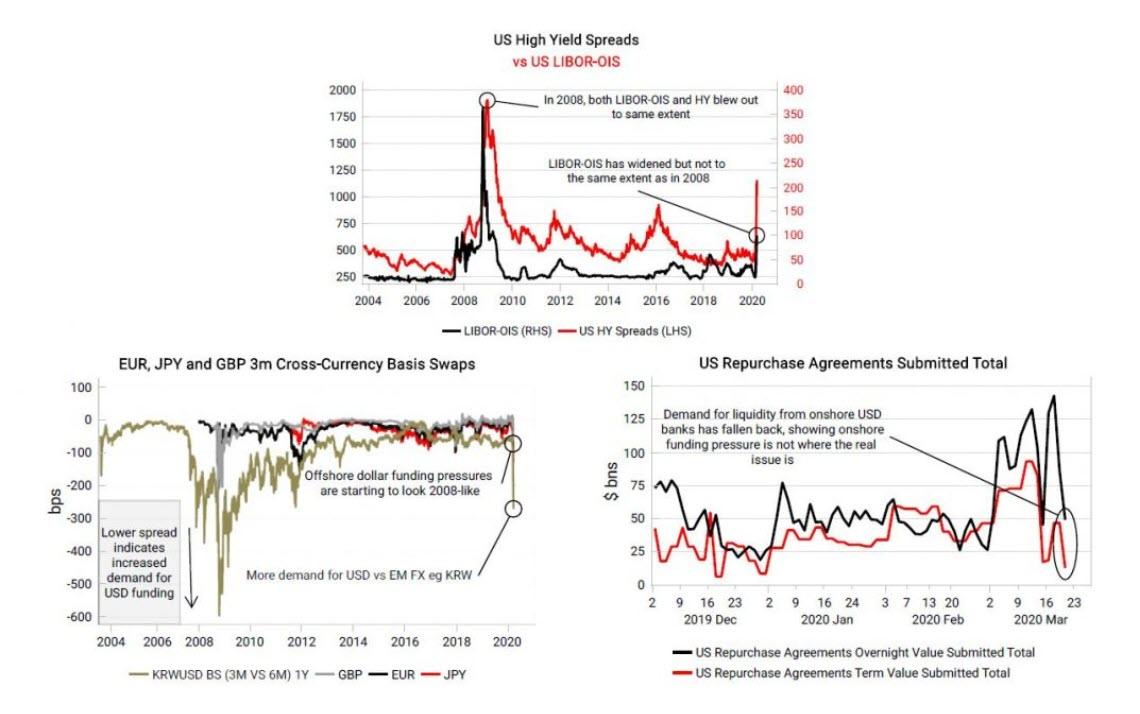

Source: Variant Perception

Thus, this is not a game of musical chairs in the financial system. Rather, businesses will be forced to hold their breaths until life returns to normal. Cash will burn and balance sheets will stretch. The commercial environment is now one of survival, plain and simple (to say nothing of those individuals infected). Businesses of all sizes will be tested, and in particular small and mid-sized ones that lack access to liquidity lines. Not all will make it. To be sure, the financial system will suffer; however, as an effect, not a primary cause. This war is not the GFC.

Decentralized Solutions Needed

Given this dynamic, I’m skeptical that flooding the financial system with liquidity necessarily helps. In the GFC, a relatively small handful of banks (and finance companies) sat at the epicenter. Remember, finance is a levered industry characterized by timing mismatches of cash flows; it borrows “long” and earns “short.” This intermediation is its value proposition. Thus, extending liquidity can help bridge timing gaps to get them through short-term issues, thereby forestalling their deleveraging.

Today, however, the financial system is not the cause of the crisis. True, liquidity shortfalls are the source of stress. However, they are not limited to any one industry or a handful of identifiable actors. Rather, nearly every business may find itself short on cash. Availing currency to banks does not pay your favorite restaurant’s rent or cover its payroll. Quite frankly, I’m skeptical that any mandated measure can. A centralized solution simply cannot solve a decentralized problem.

Fishing With Dynamite

The speed and intensity at which investment markets are reacting is truly dizzying. In many ways they exceed those in the GFC. To be sure, a response to rapidly eroding fundamentals is appropriate. However, this one seems structural.

In my opinion, the wide-scale and indiscriminate carnage is the calling card of one thing: leverage unwinding. It wouldn’t surprise me to learn of a Long Term Capital Management type of event occurring, whereby some large(?), obscure(?), new (?), leveraged investment fund(s) is (are) being forced to liquidate lots of illiquid positions into thinly traded markets. This is purely a guess. Only time will tell.

Daniel Want, the Chief Investment Officer of Prerequisite Capital Management and one of my favorite investment market thinkers, put it best:

“Something is blowing up in the world, we just don’t quite know what. It’s like if you were to go fishing with dynamite. The explosion happens under the water, but it takes a little while for the fish to rise to the surface.”

Daniel Want, 2020 03 14 Prerequisite Update pt 4

What To Do

This logically raises the question of: What to do? From a policy perspective, I have little to offer as I am simply not an expert in the field (ask me in the comment section if you’re interested in my views). That said, the Fed’s response seems silly. Despite the severe investment market stresses, I don’t believe that we’re reliving the GFC. There’s no nail that requires a central banker’s hammer (as if there ever is one). If a financial crisis develops secondarily, then we should seriously question the value that such a fragile system offers.

Markets anticipate developments. I can envision a number of scenarios in which prices reverse course swiftly (such as a decline in the infection rate, a medical breakthrough, etc.). I can see others leading to a protracted economic contraction, as suggested by the intense market moves. Are serious underlying issues at play, even if secondarily? Or are fragile and idiosyncratic market structures to blame? These are the questions I’m trying to grapple with, weighing the unknowns, and allocating capital accordingly.

As an investor, seeing the field more clearly can be an advantage. Remember, it’s never different this time. Nor, however, is it ever the same. This makes for a difficult paradox to navigate. It’s in chaotic times when an investment framework is most valuable. Reflexively fighting the last war seems silly. Rather, let’s assess the current one as it rapidly develops and try to stay one step ahead of the herd.

Good luck out there and stay safe. Strong views, held loosely.

Tyler Durden

Sat, 03/28/2020 – 16:15![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com