Platts: 4 Commodity Charts To Watch This Week

Tyler Durden

Mon, 06/29/2020 – 13:33

Via S&P Global Platts Insight blog,

As oil markets begin to recover from the shocks of recent months, side-effects like falling VLCC rates and congestion at Chinese ports are emerging, write S&P Global Platts news editors. Plus, competition heats up among corn exporters amid low ethanol demand, and UK power prices reflect improving demand.

1. Freight rates dive as call on VLCCs for floating oil storage lessens

![]()

What’s happening? The amount of crude stored on tankers is showing signs of a descent in response to the waning economics for storage, as production cuts and a measured demand recovery aids a rebalancing of the global oil market. The slowdown in storage is already starting to have a significant impact on freight. Rates on VLCCs have plunged dramatically in the past month as a gradual fall in floating barrels prompts an influx of tonnage, which has coincided with fewer spot crude cargoes due to the OPEC+ production cuts. Freight rates for a West Africa-Far East voyage, carrying a 260,000 mt cargo, dropped to an almost year-low last week, according to S&P Global Platts data. Rates on this voyage were assessed at Worldscale 37.50 or $13.51/mt on June 26.

What’s next? “The direction of spot rates will now be dictated by how quickly vessels engaged in floating storage are returned to active trade, and the timing and magnitude of the reversal of the OPEC+ production cuts implemented in May,” S&P Global Platts Analytics said. There are currently close to 190 million barrels of crude on floating storage compared with 200 million barrels earlier in the month, according to data from Platts trade flow software cFlow.

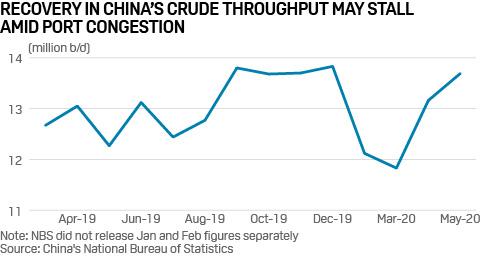

2. China’s oil import surge clogs ports, threatens refinery operations

What’s happening? China’s crude oil imports jumped 19.2% on the year to an all-time high at 11.34 million b/d, or 47.97 million mt, in May as refiners took full advantage of ultra low crude prices and ample storage capacity. But the recent flurry of tankers arriving in Chinese waters has been hampered by limited port capacity. As of June 24, at least 41 ships carrying a combined total of around 51.07 million barrels of crude were waiting to be discharged at Shandong ports for more than a week. Making matters worse, there at least seven cargoes of crude oil have jumped the queue to deliver into storage facilities designated by the Shanghai International Energy Exchange, or INE, since late May.

What next? The port congestion and the subsequent logistical constraints could put brakes on the upward momentum in independent refiners’ run rates and crude throughput levels. Daily crude throughput at an 8 million mt/year Weifang-based refinery was briefly cut by half to around 10,000 mt for about two to three weeks earlier this month because of the congestion and subsequent delay in crude feedstock delivery. The prolonged congestion could seriously affect operations and fuel output at many more refineries as they struggle to replenish their feedstock inventory on time, industry and market sources said.

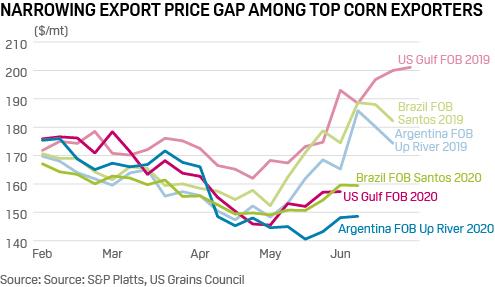

3. Race between top corn exporters to heat up amid big harvests

What’s happening? For most of 2019, US corn remained expensive for buyers due to weather-related issues, which helped shipments from South American producers Brazil and Argentina gain ground in global markets. However, unprecedented ethanol demand destruction has made corn prices in the US cheaper this year. An analysis of the corn FOB prices from the top three exporters, the US, Brazil and Argentina, shows the wide gap in prices observed last year has not developed so far this year.

What’s next? Bumper harvests in all the three top corn exporting countries, amid low demand from the energy sector, are likely to keep FOB corn prices at lower levels. Corn harvesting has begun in Brazil, and is already completed in 60% of the planted area in Argentina. This is likely to weigh on corn prices in the coming weeks and further narrow the price difference, especially in Brazil. Prospects for the US corn crop already look favorable so far, with acreage seen at an eight-year high. As a result, competition in the corn export market is likely to heat up during the current marketing season of Brazil and Argentina, with US supplies coming into the market later on.

4. UK forward power prices perk up on signs of demand recovery

What’s happening? UK forward electricity prices are now back above pre-lockdown levels for the first time, the third quarter 2020 baseload contract up 25% since the start of June. The lift reflects gains across the commodity complex – not least carbon which has surged to a 2020 high (see chart) – with UK clean spark spreads for gas plant at GBP4/MWh now more double lockdown lows seen in early March.

What’s next? The surge reflects increased optimism around the pace of lockdown easing – not just in the UK but also across Europe and beyond. While European power demand is set to remain below normal levels into Q3, French nuclear’s poor state of availability looks set to support prices for the period. “Our current base case scenario assumes that year-on-year losses in nuclear output outweigh the drop in demand, while net imports into the region are boosted by strong Nordic hydro reservoir levels,” S&P Global Platts Analytics’ head of European power analysis Glenn Rickson said.

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com