Platts: 5 Commodity Charts To Watch This Week

Tyler Durden

Mon, 07/06/2020 – 14:00

Via S&P Global Platts Insight blog,

Global energy markets are still fragile, with Japanese LNG imports at more than 10-year lows in May, while fuel demand recovery across Asia remains patchy. S&P Global Platts editors also report on record US gas pipeline exports to Mexico, rapidly filling European gas storage and falling French winter power prices.

1: Japan’s LNG imports lowest since April 2009

What’s happening? Japan imported 4.58 million mt of LNG in May, down 18% year on year and 12% from April, according to data from Trade Statistics of Japan, Ministry of Finance. This was the lowest level of LNG imports for the world’s largest LNG importer by volume since April 2009, and reflects weak downstream demand due to the coronavirus-related slowdown in the economy. May is typically the slowest time of the year for the country’s energy demand due to the Golden Week holidays, but this year has been weaker than usual. Japan’s June LNG imports appear to have risen slightly, according to vessel tracking data, but not by a large degree and the outlook remains highly uncertain.

What’s next? While Japanese end-users hope for demand recovery in the downstream market, the majority hold a bearish view. Japanese LNG importers are expecting muted recovery in the second half of 2020 due to extremely high inventory levels and weak fundamentals from the industrial, manufacturing and hospitality sectors. Summer demand has not been very supportive; most factories can’t run at full capacity unless the entire supply chain is backed up by strong exports, while city gas companies have been troubled by “tank-top” or full storage tank scenarios. For LNG suppliers, the last shred of hope for a market recovery is with peak winter demand later in 2020.

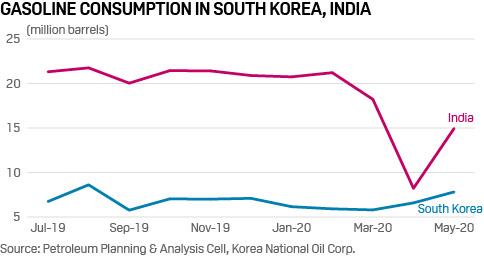

2: Asia’s fragile fuel demand recovery and shift in trading strategies

What’s happening? Uncertainties continue to surround the pace of recovery of regional demand for transportation fuels and other oil products, especially in the face of a potential second wave of the coronavirus. New cases have popped up in countries that have lifted movement restrictions, such as South Korea, Australia and Thailand, adding to the uncertainties of how fast fuel consumers will be ready to hit the streets again. South Korea’s domestic gasoline demand rebounded to 7.81 million barrels in May from 6.58 million barrels in April, but monthly consumption is unlikely to recover above 8.2 million barrels as long as the pandemic persists, according to major South Korean refiners surveyed by S&P Global Platts.

What’s next? Asian fuel producers and importers are keen to adjust their trading strategies as demand recovery remains fragile. Adapting to the uncertain demand recovery outlook, South Korean petrochemical makers said they would continue to seek ways to renegotiate their term naphtha purchase volumes. Indonesia’s Pertamina also shortened its usually half-yearly term gasoline contract to quarterly commitments. The need to ensure flexibility has also had an impact on the supply side. Japanese refiners and New Zealand’s Refining NZ have turned toward importing gasoline, as opposed to producing it themselves.

3: US Gas pipeline exports to Mexico hit record high

![]()

What’s happening? US gas pipeline exports to Mexico have surged to a record high of over 6.1 Bcf/d, recently propelled by rising summer temperatures and growing demand. While record regional consumption in northern Mexico last month coupled with hotter weather to lift Mexico’s baseline imports, the new single-day record appears to have been driven by a negative pipeline imbalance, data from S&P Global Platts Analytics shows. Imbalances on Mexico’s national grid have become more frequent recently as domestic production continues to decline alongside rising demand and poor regional pipeline interconnectivity.

What’s next? Over the next several weeks, US pipeline imports are poised to hit fresh record highs again – potentially well over 6.1 Bcf/d – as the startup of new downstream infrastructure allows imported gas to flow further south into Mexico’s central-west, southern and peninsular regions. Commissioning of the Cempoala Phase II compressor station reversal and Fermaca’s Wahalajara pipeline system would pull significant incremental supply from West and South Texas and could help to reduce the incidence of pipeline imbalances by improving regional interconnectivity, enabling gas to flow where it’s needed.

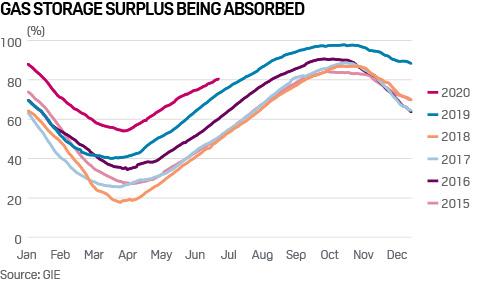

4: European gas storage surplus to be absorbed as injections slow

What’s happening? Key to the European gas supply-demand balance in the coming month is the rate of storage injections given the already high level of fullness across the continent. EU stocks are currently more than 80% full, leaving only limited space for injection with three months of the traditional injection season left. However, injection rates have slowed significantly over recent weeks, giving some respite to a market that had been under significant price pressure.

What’s next? If injection continues at current rates, there is an expectation that the current surplus of storage over last year’s level could be absorbed by August. Lower injection rates come as European gas prices have risen from their mid-May lows, making the seasonal storage play less attractive. Ukraine also remains an option for traders looking to find a storage home for their gas, despite planned maintenance on a pipeline from Slovakia potentially making it more difficult for traders to flow gas to Ukraine to make the most of the country’s cheap storage and vast spare capacity.

5: French winter power prices fall back as EDF lifts nuclear target

![]()

What’s happening: French nuclear operator EDF has lifted its 2020 nuclear output target as maintenance concerns ease. A revised target of 315 TWh to 325 TWh allows for a 4.5 GW increase in nuclear generation in the second half of 2020 versus the previous 300 TWh target. This remains materially below the 375 TWh target set in February before the coronavirus pandemic, but nevertheless has had an immediate, bearish impact on northwest European power prices.

What’s next? French winter power prices fell sharply July 3, with the Q4 baseload contract on EEX opening some 11% lower on the day. Further upside to French nuclear output could see Europe’s nuclear powerhouse resume its traditional role as Europe’s discount market this summer (outside the Nordics), with additional exports flowing to Great Britain via the new 1 GW IFA2 interconnector, set to enter testing this quarter, augmenting the 2 GW IFA-1 link. Meanwhile, a third UK-France interconnector, ElecLink, is approaching a moment of truth as the Eurotunnel’s Intergovernmental Committee debates July 9 whether to approve the pulling of cables through the tunnel. If positive, the link is scheduled to be operational mid-2021.

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com