Platts: 5 Commodity Charts To Watch This Week

Tyler Durden

Mon, 08/10/2020 – 13:55

Via S&P Global Platts Insight blog,

The diverging performance of commodities amid the coronavirus crisis, Indian oil demand and iron ore’s continued climb are explored in this week’s selection of energy and raw material trends to watch. Plus, Henry Hub rallies, and UK coal generation retreats.

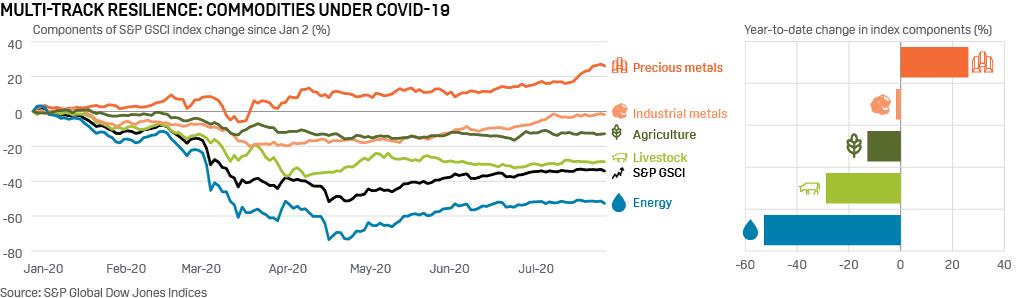

1. COVID-19’s uneven impact on commodities

What’s happening? The S&P GCSI commodity index is down 34% since the start of the year, but commodities have experienced widely different impacts from the pandemic and their recovery paths are still on multi-track trajectories. Crude prices crashed to four-decade lows while gold has jumped to all-time highs. Non-ferrous metals and power demand were initially hit hard due to lockdowns, but have staged a robust recovery. In the cereals and meat markets, most prices have remained under pressure amid ongoing demand-side uncertainties.

What’s next? Market watchers see improving macroeconomic and supply-side conditions that will broadly support the recovery of commodity prices, albeit at a gradual, uneven pace over the next 12 months. In oil, demand is stabilizing and as OPEC + maintains discipline on output cuts and stocks levels draw-down, S&P Global Platts Analytics sees Brent heading towards $50/b by end-2021, with WTI at around $45/b.

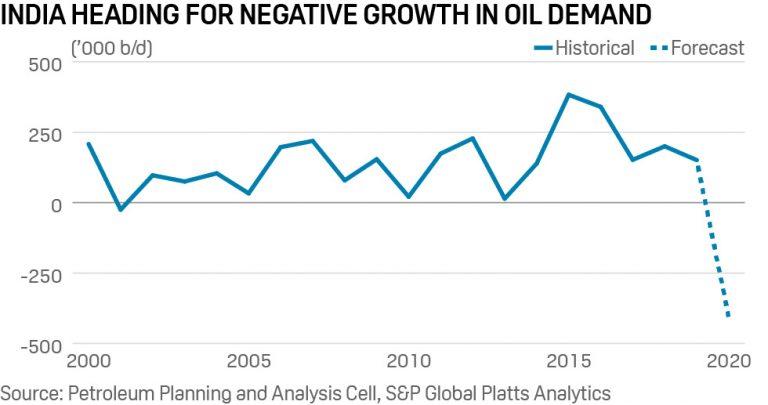

2. India oil demand forecast to drop after nearly 20 years of growth

What’s happening? India, one of the fasting-growing oil markets in Asia in recent years, is expected to end 2020 with its oil demand slipping into the red, a trend not seen for nearly two decades, according to government officials and oil analysts. The last time India witnessed negative growth in oil demand was in 2001. Refinery activity increased in June but the trend is now reversing. Run rates at Indian Oil Corp., the country’s largest state-run refiner, have fallen to 75%, from as high as 93% in the first week of July.

What next? As hopes of Indian demand recovery in H2 dwindle, with some provinces implementing partial lockdowns to battle the COVID-19 pandemic, refiners are starting to plan for lower crude runs in order to prevent an excess build-up of oil. According to S&P Global Platts Analytics, India’s oil demand is expected to be down 115,000 b/d year on year in H2, and whole-year demand will be down by 405,000 b/d on year. Some petroleum ministry officials say India’s oil demand is unlikely to reach pre-COVID-19 levels at least until March 2021.

3. Iron ore keeps rising on Chinese demand, tight supply

![]()

What’s happening? The price of 62% Fe iron ore fines delivered to China has in recent days approached its five-year high of July 2019 on market fundamentals, prompting several analysts to increase their average price expectations for the year and adopt a “stronger for longer” outlook.

What’s next? Iron ore prices are expected to remain firm for the foreseeable future, upheld by soaring steel output and low iron ore port stocks in China. The Asian giant, which takes around three-quarters of the world’s iron ore seaborne supplies is on a post-COVID-19 infrastructure drive that is pushing up domestic steel demand. Coinciding with this are lower than anticipated iron ore exports from Brazil, where production has still not fully recovered after the Brumadinho dam accident in early 2019. Recent analysis by S&P Global Platts signals that Brazilian miner Vale may need to boost iron ore exports by as much as 8 million mt/month to meet its 2020 guidance. Australian new mine developments, meanwhile, are seen being curtailed by ESG considerations. In the longer term, pressure on steelmakers from continued high iron ore prices may be unsustainable, leading to downwards price pressure, especially if companies and governments speed up moves to favor production alternatives like the use of steel scrap in electric arc furnaces.

4. Pipe maintenance, higher demand support Henry Hub rally

![]()

What’s happening? Henry Hub cash prices continue to rally in recent trading, rising into the low $2s/MMBtu, or their highest since late 2019, S&P Global Platts data shows. The recent uptick has accompanied tighter supply-demand fundamentals in the Gulf Coast region. In the nearby Haynesville, production continues to decline. In the Permian, pipeline maintenance has prompted a steep decline in output to an average 10.6 Bcf/d this month, down from recent highs of over 12 Bcf/d in July. Stronger gas demand from the region’s industrial and LNG export facilities this month has also supported the rally.

What’s next? Over the balance of summer, higher gas prices could reduce US power burn demand, as generators begin switching away from gas to coal. In July, record-low gas prices and above-average temperatures helped to propel power burns to previously unrecorded levels at over 46 Bcf/d. Assuming cash, futures and forwards prices remain above $2/MMBtu, a continuation of hotter weather this month is unlikely to be enough to push generator demand to highs seen in July.

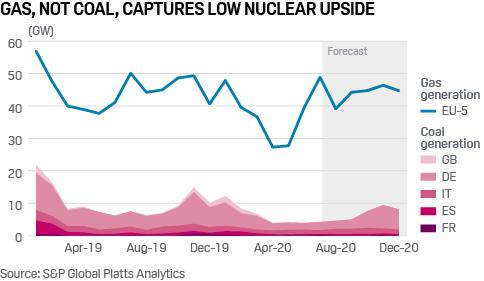

5. GB set for zero commercial coal generation in Q4: Platts Analytics

What’s happening? Britain’s 5.2 GW coal fleet averaged a paltry 140 MW of generation in April and since then has been almost completely absent due to high carbon costs, cheap gas and lower demand. The continental European situation has been similar, if less marked, with gas, not coal, compensating for poor French nuclear availability and a dip in hydro. Poor coal economics are encouraging operators like SSE, Drax, Enel and EDP to bring forward plant closure plans, while the first compensation-for-closure auction in Germany began in early August.

What’s next? Current fuel and carbon economics mean S&P Global Platts Analytics is now assuming zero commercial generation from GB coal plant for the rest of 2020, an unprecedented event if true. Drax may run out of merit, but this would be to use up stocks ahead of closure in March next year. On the continent, Platts Analytics forecasts that, even if coal and carbon prices see some downside, in normal weather conditions fuel economics will keep coal running in EU-5 (DE, FR, GB, IT, ES) markets below 5 GW until October. Plus-44 GW levels are forecast for EU-5 gas plant through September and the whole of Q4, peaking above 46 GW in November.

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com