“Option Insanity” Leads To Furious Meltup: Apple Bigger Than Russell, Emini New Record High

Tyler Durden

Tue, 09/01/2020 – 16:04

For better or worse, the market continues to be defined by AAPL, which today crossed a historic threshold when thanks to its latest 4% ramp, it surpassed the entire market cap of the Russell 2000.

This is how AAPL now looks compared to all the public small cap companies:

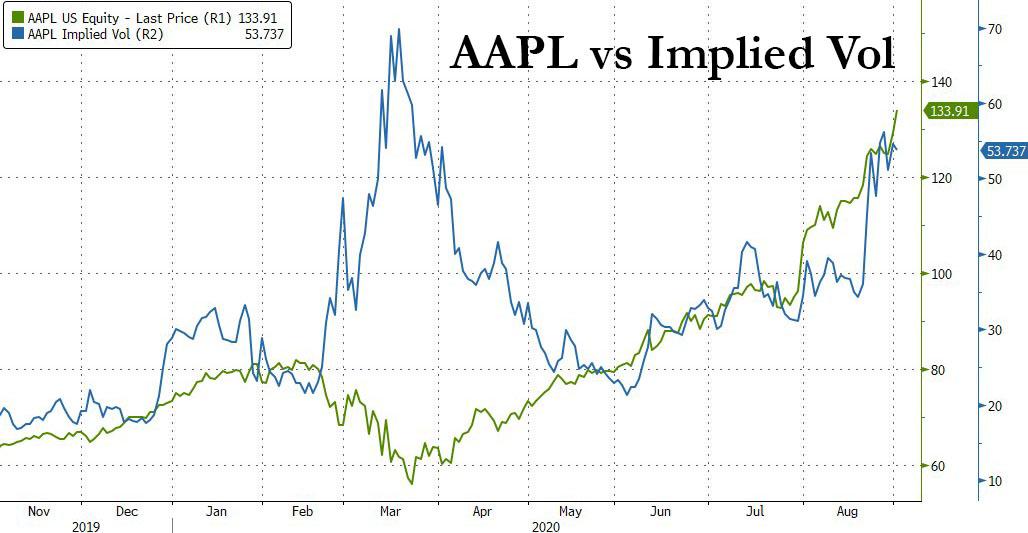

As discussed earlier, the chief reason for the relentless AAPL surge in recent weeks has been the so-called “option insanity” as the company’s implied vol has been rising alongside the stock.

And while the AAPL ramp accelerated, in no small part thanks to another price target increase this time from BofA, the other stock that has come to define market euphoria, Tesla, saw its rally halted after the company announced a $5BN “At the market” equity offering.

Yet even with today’s 4.5% drop, TSLA is now back to levels last seen… yesterday.

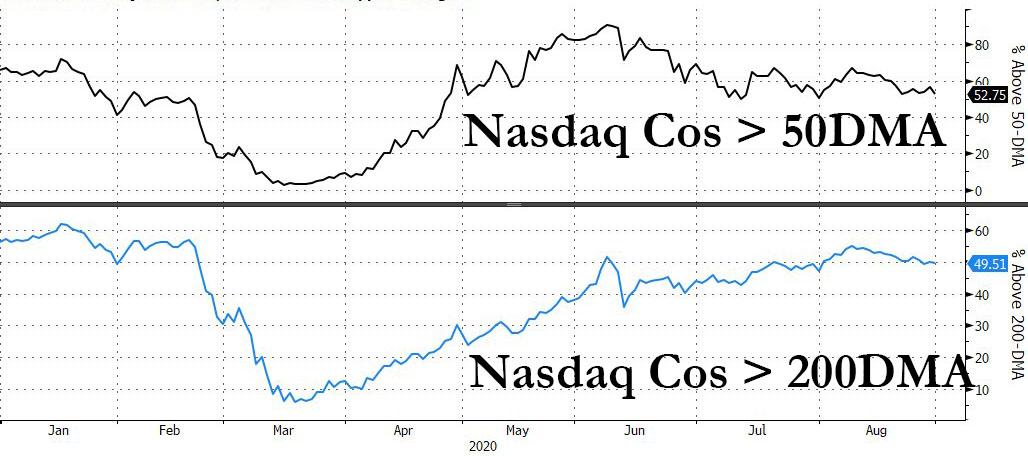

Meanwhile, due to the outsized impact of AAPL on the Nasdaq, the tech index was up more than 1% even with a second consecutive day in which decliners far outpaced advancing stocks.

Predictably, Nasdaq breadth continued to sink, with the number of tech companies trading below their 200DMA dropping below 50%, and just over half trading above their 50DMA.

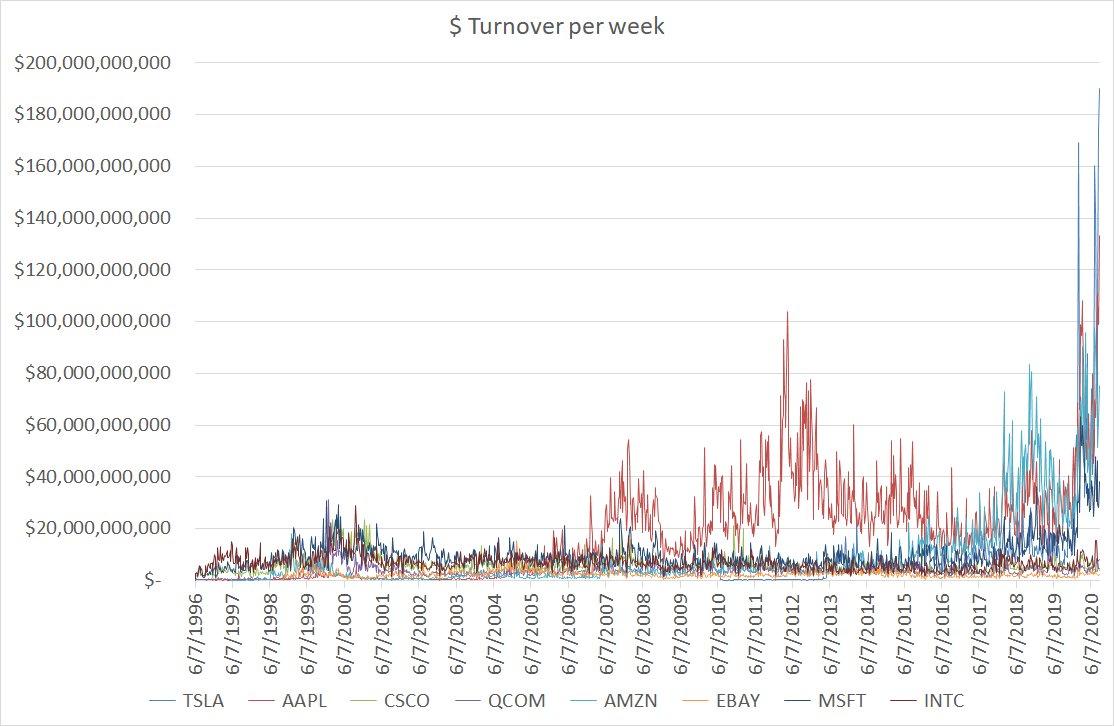

One more chart showing what Michael Krause called the biggest bubble in history: on a dollar basis, the turnover in tech names as retail investors and delta-(un)hedged dealers flood in, is simply stunning.

To be sure, it wasn’t just tech names with Walmart’s 7% surge boosting the Dow Jones Industrial Average which is also rapidly approaching its all time high thanks…

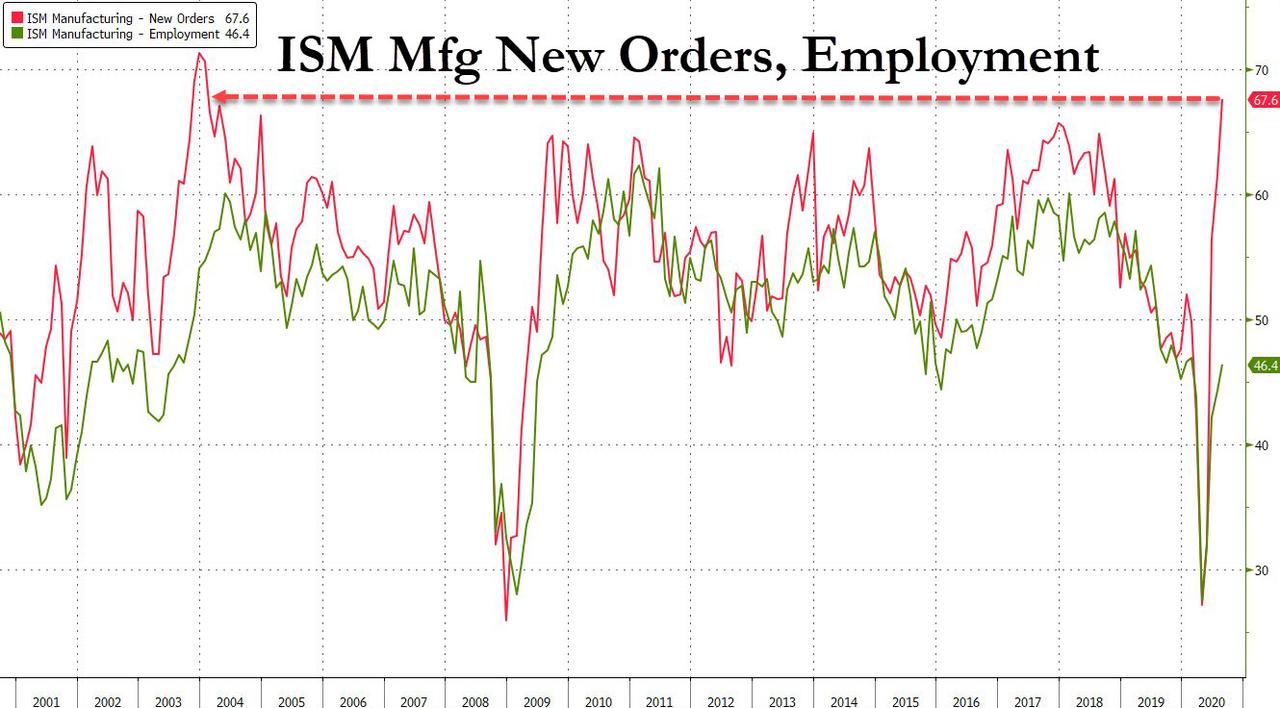

… to a large extent stellar Markit and ISM manufacturing PMI readings which saw the New Orders surge to the highest level since 2004 (even as employment remains deep in contraction)…

… this failed to spark a broad reflation wave, with yields on the 10Y Treasury sliding 3bps and declining for the 3rd day in a row.

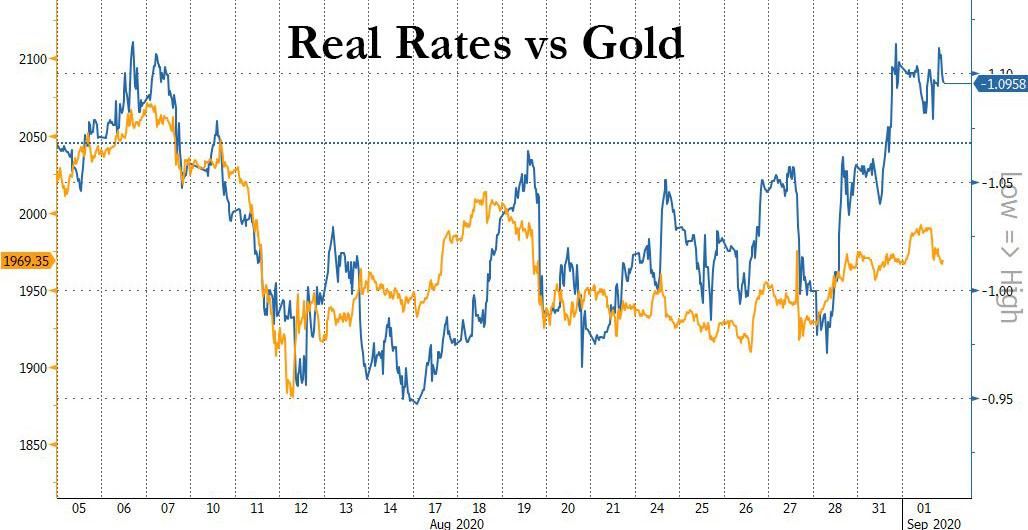

And since breakevens actually dropped today despite the strong eco data, this means that real rates also slumped back to their post-crisis lows of -1.08%, hardly the stuff the Fed’s AIT mandate wants to see.

Yet while real rates slumped to new cycle lows, gold – which has tracked real rates very closely for much of the past decade – failed to make a new high above $2,000.

How come? Perhaps due to expectations that the dollar is oversold and will squeeze higher, a glimpse of which we caught today when after sliding to fresh 2 year lows, the Bloomberg dollar index jumped back to green on the day shortly after the EURUSD briefly rose above 1.20

Unfortunately, one can look at the macro until one is blue in the fact in hopes of deciphering the market, the sad reality is that for all intent and purposes, only Apple and Tesla continue to matter, and until there is a decisive breach in the upward trajectory of both, the melt up will only accelerate as we are now well in the blow off top phase, as the action in the EMini in the last minute of trading showed so clear, when the S&P future surged by 10 points in seconds despite a $1.3 billion MOC imbalance for sale, just so the ES could hit a new record high on the back of another massive gamma squeeze.

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com