South Sea Stock Price Bubble Is Good Reminder, Even 300 Years Later

Tyler Durden

Sun, 10/04/2020 – 09:20

Authored by Tim Shaler via The Epoch Times,

Three hundred years ago, a stock market bubble popped that almost destroyed the United Kingdom.

As with other quickly inflating assets, the stock market price of the South Sea Co. rose so much so quickly that lots of other people started “panic buying”—buying so that they could get in on the action of such an investment opportunity that had made so much money for other people.

Also, as with other asset price bubbles, South Sea’s investors thought the lofty valuations made sense; after all, the crown had given the company exclusive rights to trade between the UK and Spain’s colonies in the Caribbean and South America. It seemed profits would keep going up “forever”—until they didn’t.

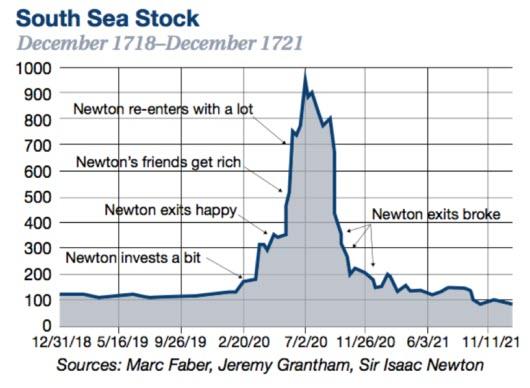

In the fall of 1720, share prices plummeted and many investors witnessed their savings disappear practically overnight.

We are wise to remember these lessons.

There have been many instances of amazing speculation leading to spectacular price inflation, only to have all that speculation prove wrong and that highly inflated asset “bubble” suddenly pops.

That’s why investors are wise to consider whether an asset price really does make sense, given the long-term prospects of the company’s profits.

In the late 1990s, shares of Gap Inc. were trading at such a high multiple, the share price was implying that the company would soon be selling the equivalent of all of the clothes sold in retail stores in all of the G-7 countries. That obviously didn’t happen and share prices sold off.

Some investments do make sense, of course. For example, according to MacroTrends.net, after adjusting for stock splits, one share of IBM 50 years ago would have cost $6.51; it’s now trading at about $119 per share—an almost 20 times increase in that time span. That equates to a 50-year compound annual growth rate of 6 percent.

But many other investments have famously not gone as well.

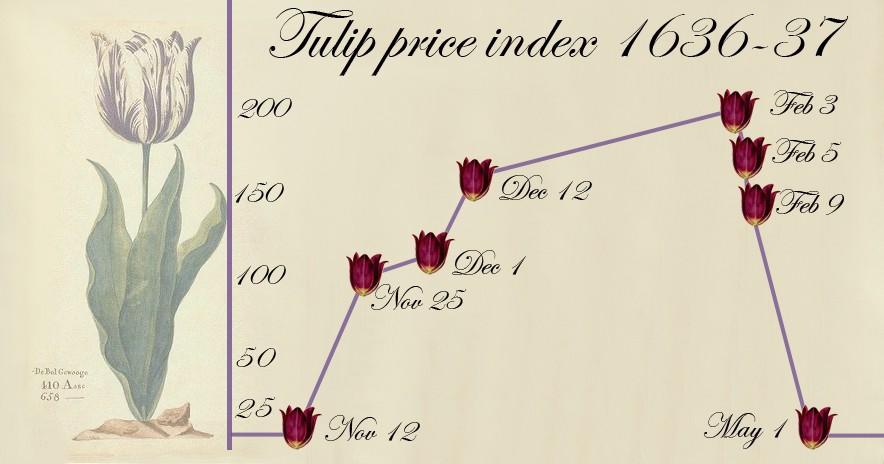

In 1634, much of Amsterdam was all abuzz about tulip bulbs. They were exotic and expensive and seemed only to go up in value. According to Investopedia, prices for some exotic bulbs eventually came to equal the value of a mansion along the Grand Canal. Then, three years later, in 1637, tulip bulbs lost their value and, by 1638, were only worth the ascetic value associated with the pretty tulip flower that would bloom in the springtime.

More recently, of course, the U.S. stock market crash of 1929 ended the “Roaring ‘20s” and ushered in the Great Depression, while the frenzy in the U.S. housing market from 2004 to 2006 also finally came to end, triggering massive job losses and banking crises in countries where banks were convinced to buy debt backed by mortgages lent to U.S. homebuyers.

More trouble occurred when banks could no longer lend to those countries because banks were encountering such bad losses on loan portfolios tied to the U.S. mortgage borrowers. Countries that experienced massive recessions in the years after the 2006 U.S. housing bubble popped included Iceland, Ireland, Portugal, Spain, Greece, and Cyprus.

Before then, the U.S. property market had never gone down in value since the deflationary years of the Great Depression of the 1930s, even as challenges affected some regional markets: Texas, when oil prices fell; Boston, when a major bank there had collapsed, and so on. And with a strong economy and immigration still positive, it seemed to many that U.S. property values could not go down.

It took about 85 years for Londoners to forget the lessons of the Tulip Bulb craze and bubble of Amsterdam before they themselves bid up investment prices in the South Sea Co. to unsustainable levels, only to have values come crashing down and destroy the savings of many in the UK.

Then, it took 85 years for global investors to forget the lessons of the 1930s and think the U.S. property market couldn’t fall in value. Obviously, the lessons of 2008–2009 proved otherwise.

Investors today would be wise always to ask themselves whether the investments they are making are at values justified by future profits and not just by the hope of selling to some future, greater fool.

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com