China To “De-Risk” Both Monetary And Fiscal Policy In 2021: SocGen

While the U.S. continues to print money as though there will be zero consequences and while a China-borne virus (or, rather, the response to the virus) continues to ravage economies globally, China is planning on shoring up and “normalizing” both its fiscal and monetary policy heading into 2021.

A new note from SocGen to clients on Monday of this week says that the Chinese government at the annual Economic Work Conference telegraphed that it is “poised to scale down both monetary and fiscal policy impulses from here, and that the focus have been shifted back toward controlling risks, including local governments’ implicit debt, banks’ capital adequacy, housing stability and too-big-to-fail companies.”

Regarding fiscal policy, SocGen predicts that China will be “still proactive but less accommodative.”

The stance was described as “proactive”, focusing on “effectiveness” and “sustainability”. The wording signals a less accommodative stance signalled up until 3Q, when it was stated that “proactive fiscal policy has to be even more proactive”. While the government should support important tasks such as promoting technological development, accelerating structural adjustment and improving income allocation, it also needs to further mitigate the risk of implicit local government debt.

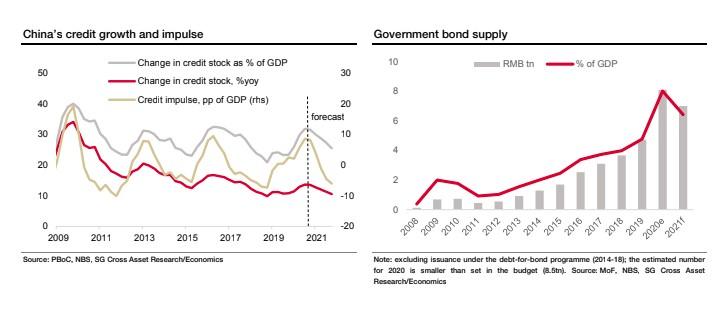

“This echoes comments from policymakers that expressed concerns over local government debt sustainability,” SocGen said. “We expect the government to announce a smaller fiscal deficit target of 3% of GDP (versus above 3.6% this year), the quota of special LGB issuance to decline considerably from RMB3.75tn this year to around RMB3tn next year, and no special CGB issuance.”

But the bigger shock to the global financial system could be the result of “normalization” continuing for China’s monetary policy. At the CEWC, China said it would stick to “prudent” monetary

policy that aims to be “flexible”, “targeted” and “reasonably appropriate”. Which, naturally, contrasts with the rest of the world – especially the U.S. – whose monetary policy has become “print money and buy anything that isn’t bolted to the floor”.

SocGen said that China’s statements regarding “maintaining M2 and TSF growth” and “keeping the macro leverage ratio largely stable” is likely a “clear reconfirmation that monetary policy intends to continue to normalise back toward a status of stable leverage, after credit growth significantly outpacing economic growth throughout 2020.”

The bank predicts that “TSF growth will slow from 13.5% currently to around 10% by end-2021.”

Among other initiatives, take on housing problems in big cities and promote green development. The note also says China’s focus will turn to expanding domestic demand in 2021. SocGen wrote:

The CEWC acknowledged that the key to expanding consumption is to increase employment, enhance the social security system and improve income allocation. It pledged to remove administrative measures that obstruct purchases in order to unleash the potential of rural consumption; to improve the occupational training and education system in order to support quality employment; and to increase public spending on education, healthcare and pensions in order to lower savings. Regarding investments, like this year, the government will focus on new infrastructure, manufacturing upgrades, old town renovation and logistics infrastructure upgrades. Mindful of debt sustainability concerns, it also stressed that over-investment in emerging industries needs to be avoided.

Assuming China’s idea of monetary normalization is different from Jerome Powell’s (to hike interest rates once before capitulating horrifically and, only months later, implementing infinite QE while embarrassingly explaining on national television that “we print it digitally”), the country could wind up taking the lead on leading the global economy onto a drastically different path in 2021.

What would be even more interesting would be if part of China’s “de-risking” includes the country deciding it no longer wants the “risk on” position of owning too many U.S. Treasuries.

Maybe there’s a reason China has been hoarding all that gold after all…

Tyler Durden

Wed, 12/23/2020 – 19:20![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com