“The Dam Is Going To Break”: We Are In The Early Innings Of A Colossal Migration Into Commodities

From Larry McDonald, author of the Bear Traps Report

The great awakening is upon us, millions of investors are loaded to the gills with deflation bets.

Imagine being wedded to big tech stocks since July only to watch commodity plays pass you like a Ferrari on Sunset Boulevard. The psychology must be respected and it’s showing up in classical technical analysis.

We must be cautious, our trade is maturing. The empty meadow has become a fairground with patrons out for a walk in the midday sun. Over the last week, both Goldman Sachs and JP Morgan have implored their sales force to embrace the “commodity super cycle”. Just months ago they were talking down this “un-investable” sector. We must buy every dip we see, especially coming from commodity producing countries like ECH Chile (copper) and EWZ Brazil (oil, agriculture and iron ore).

Bottom line, we are overbought but still the early innings of this colossal migration into commodities. The dam is going to break, there is still far too much capital in big tech. If the rate move is too aggressive we crash.

The Nasdaq has 50% downside from here, rebalance the portfolio before the market forces you to. Think 2020-2030, NOT 2010-2020. Remember: it is normal to be overbought in bull markets, and to stay that way much of the time.

In a bear market you might get slightly overbought for a few days. But when markets become so overbought for this long means we are in a new bull market.

Buy the commodity dip. There is a classic line from our global bestseller – “A Colossal Failure of Common Sense.” The late Larry McCarthy loved the fierce impact of market psychology on both bull and bear markets. He said; “just when you think it cannot possibly get any better it always does. And just when you think it cannot get any worse it always does.”

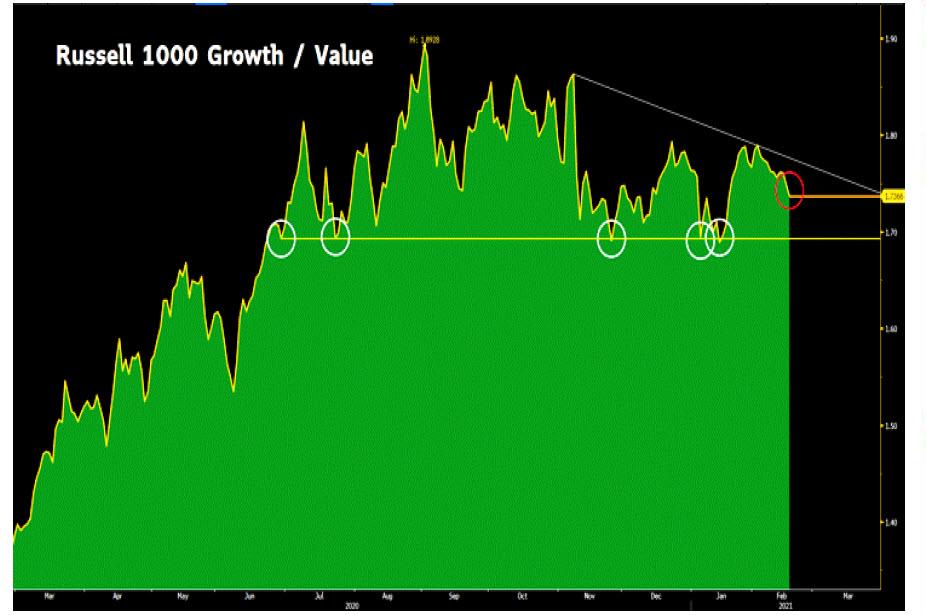

Russell 1000 Growth to Value

Tremors before the Quake – We really want to emphasize this point to clients , the 1.69 level in the Russell 1000 growth to value ratio (IWF / IWD) is highly important, in our view. We have had numerous growth to value tremors since last June and we suspect when the dam gives way, a violent wall of capital will be running…

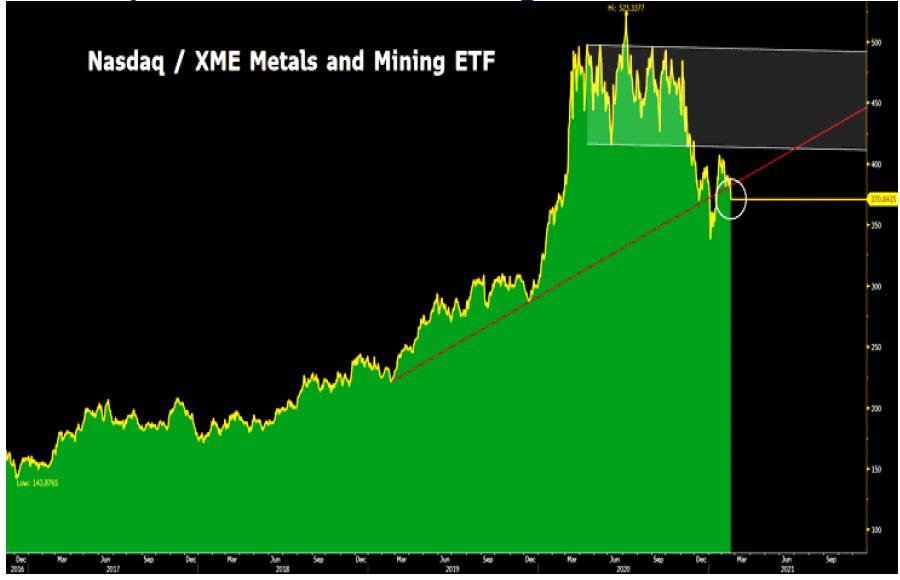

Nasdaq / XME Metals and Mining Rollover

With rates grinding higher, the Nasdaq continues to breakdown relative to the XME Metals and Mining ETF. Despite a brief bounce in recent weeks, the ratio is back below the support trend. We continue to see commodity exposed equity outperformance relative to tech over the long term.

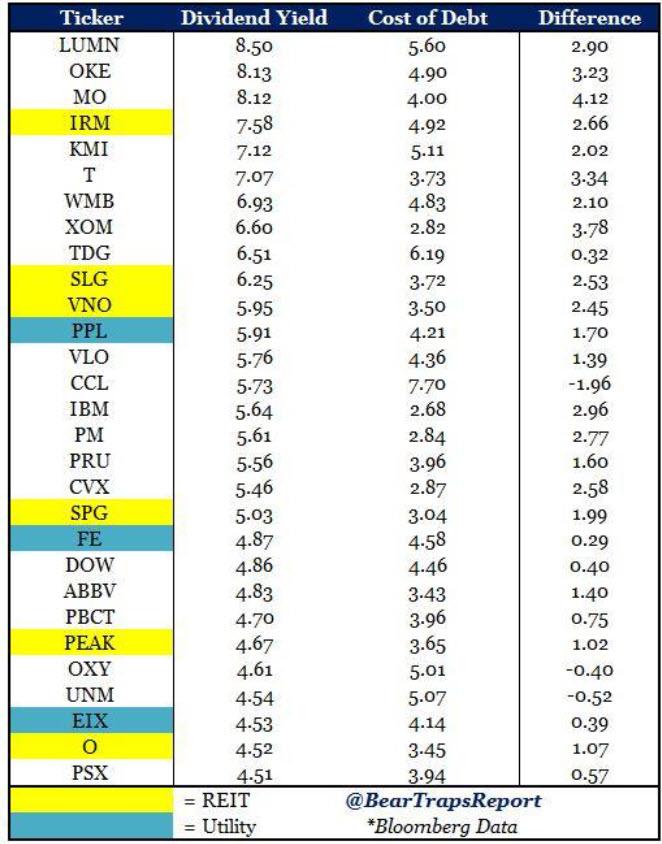

Dividend Yield and Cost of Debt

Some of the best credit investors we know always look at stock dividend yields vs. the company´s ten year corporate bonds. Interesting data here. These are the top 30 S&P 500 dividend yielders, but we also show their cost of debt. Many of the top dividend payers in the S&P are paying out much more than their cost of debt (average bond yield) and many of them have strong balance sheets as well. The top 3 highest spreads of dividend yield cost of debt are 1. Altria 2. Exxon Mobil and 3. AT&T. This speaks to how cheap true value names are.

Tyler Durden

Tue, 02/23/2021 – 12:55![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com