Diesel’s Decline One For The Ages: Biggest In Almost 6 Years

By John Kingston of FreightWaves,

Commodity diesel prices fell Thursday by an amount seen only a handful of times since 2000. The decline, coming on top of downward moves in the price of ultra low sulfur diesel on the CME commodity exchange earlier in the week, raises the strong prospect that the record 19-week run of increases in the weekly Department of Energy/Energy Information Administration diesel price has likely run its course.

Ultra low sulfur diesel on the CME declined 12.19 cents a gallon Thursday to settle at $1.7842 a gallon. However, the 6.4% decline in ULSD was less than the 6.94% decline in the price of Brent, the world’s crude benchmark, and the 7.12% decline in the price of West Texas Intermediate, the U.S. crude benchmark.

ULSD was slightly lower in early trade Friday.

The steep decline in the commodity price of diesel was notable for several reasons:

-

It took the settlement price down to a level it had not seen since Feb. 12.

-

If you take out the steepest one-day declines in the earliest days of the pandemic, when double-digit drops were regular features of the market, the decline in price Thursday was the largest since July 6, 2015, when the price declined 13.1 cts/g, or 7.12%. (That excludes final-day-of-the-month declines when traders sometimes needed to get out of long positions before the front month contract closed. That sort of action is not viewed as indicative of market fundamentals but the deadline nature of physically settled commodity contracts.)

-

Since the start of 2000, it was the eighth-largest one-day decline in the price of ULSD or the heating oil contract that preceded it. (Again, that’s excluding the early crazy days of the pandemic as well as price drops tied to contract rolls).

What happened to create such an enormous decline? The weekly EIA inventory figures, closely watched more than normal because of still-lingering market impact from the Texas deep freeze, showed a roughly 3.58 million-barrel increase in total crude and product inventories, a number somewhat bearish but not too far off the weekly predictions of S&P Global Platts. Reports from the Texas Gulf Coast are showing that the refining sector should be fully back from the impact of the deep freeze within the next week, which could be viewed as bearish for diesel (more will be produced) and bullish for crude (more will be consumed). But diesel fell less than crude, a sign that oil’s movements from its trade as a financial asset rather than a commodity — which affects crude far more than products — was at play Thursday.

The decline in diesel and crude came on the same day that a wide variety of financial assets fell on fears of higher interest rates and inflation, with the NASDAQ down roughly 2% and the S&P 500 falling 1.48%. Helping to drive oil down was the continuing rise in the strength of the dollar, a financial factor that usually works to push oil prices down but which the stronger oil market has resisted for several weeks. That countercyclical move appears to have ended Thursday.

Wholesale diesel prices do react quickly to changes in the commodity market. The national average wholesale diesel price was down almost 10 cents a gallon by Thursday, according to the ULSDR.USA data series in SONAR.

However, the DTS.USA retail diesel price series is showing mostly flat prices, signaling that any decline in the DOE/EIA price next week is going to be nowhere near the level of the fall in commodity and wholesale prices.

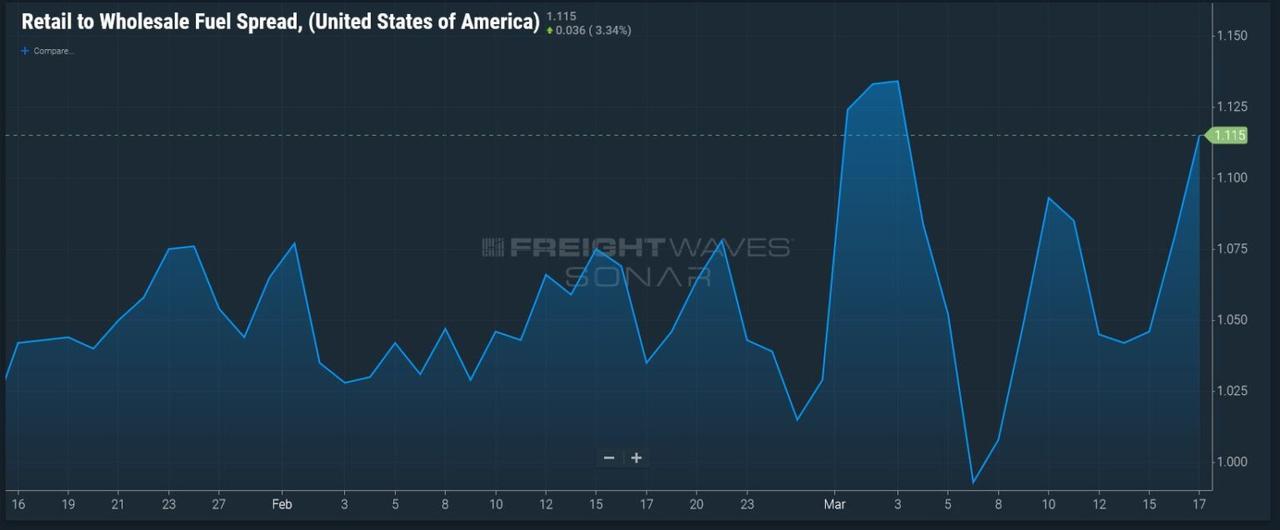

Retail prices always lag wholesale moves, particularly on the way down, and that can be seen in the uptick in the FUELS.USA data series in SONAR, which reflects the wholesale-to-retail price gap. A few weeks ago it was at its lowest level in months but has now moved up sharply.

On a more macro level, the collapse in oil prices occurred during a week when the closely watched International Energy Agency projections produced a pair of reports that were relatively bearish to stable in the short term but decidedly bullish long-term.

The oil market had been supported by the decision earlier this month taken by the OPEC+ group to not increase production, even as most forecasters thought the group of oil exporters would do so. In its report, the IEA noted that even with that decision, there is plenty of spare capacity on the market and that inventories “in tanks and under the ground” will be able to “keep global oil markets adequately supplied.”

But longer term, the IEA’s medium-term report issued in conjunction with its monthly report saw oil markets tightening longer-term. Although consumption growth rates have been thrown off their path by the pandemic, the IEA still sees global consumption at 104.1 million barrels a day in 2026, 4.1 million barrels a day more than in 2019.

But where will that supply come from? With U.S. growth constrained by a tightening of lending standards, the IEA sees global production capacity rising 5 million barrels a day by 2026. But given the normal rate of depletion and decline, the agency said production would need to rise 10.2 million barrels a day “to meet the expected rebound in demand.”One positive aspect of the report for diesel consumers: There will be plenty of capacity to process crude. Refining capacity is suffering from a “massive overhang” that will need significant closures to become balanced, the report said.

Tyler Durden

Sat, 03/20/2021 – 15:00![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com