Futures, Rates Calm Ahead Of FOMC As Copper Crumbles

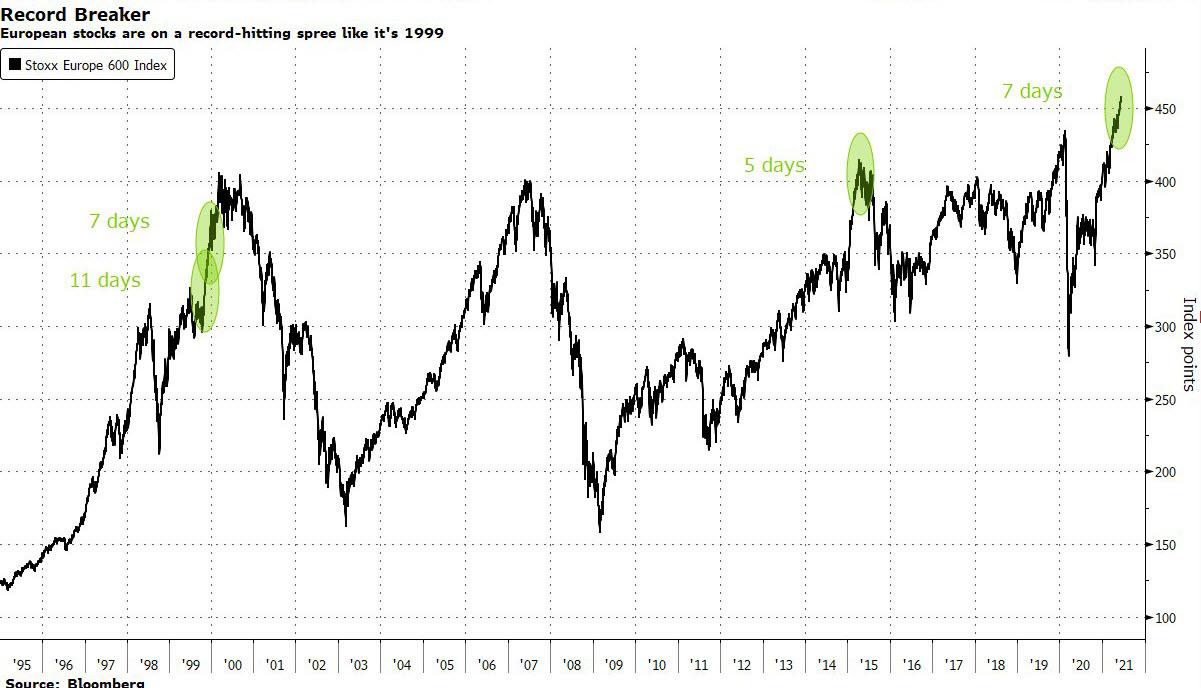

World stocks and S&P futures hit another record high on Tuesday, with European stocks poised for their longest record streak since 1999 as investors bet likely “transitory” inflation pressures will stay the U.S. Federal Reserve’s hand from signalling a shift in policy settings. After a powerful ramp in the last 30 minutes of Monday trading, pushing them to new all time highs, S&P 500 futures pared an early gain and were up 0.1% last at 4,250 while as European equities were led higher by chemical firms, despite a sharp drop for European miners after copper touched the lowest level in seven weeks over concerns over U.S. monetary tightening and a pull-back in Chinese demand. The 10-year Treasury yield pulled back under 1.5%, nd the dollar was steady and bitcoin traded just over $40,000.

At 730 a.m. ET, Dow e-minis were flat, S&P 500 e-minis were up 4.50 points, or 0.11%, and Nasdaq 100 e-minis were up 22.75 points, or 0.16%. The S&P 500 , the Dow Jones and the Nasdaq have gained 13.3%, 12.3% and 10%, respectively so far this year as investors tried to find their ground between inflation concerns and optimism about an economic reopening.

In corporate news, Biogen fell 0.9% in premarket trading after the drugmaker’s potential therapy for choroideremia, an inherited disease that leads to vision loss, did not meet the main goal in a late-stage study.

Other notable premarket movers include:

- Cryptocurrency-exposed stocks rise after Bitcoin topped $40,000 per token, its highest level since May. Ebang (EBON) gains 3.2% and Bit Digital (BTBT) climbs 2.7%, while Riot Blockchain (RIOT) advances 1%.

- Document Security Systems (DSS) plunges 41% in premarket trading after the company announced a stock offering at a discount.

- Eloxx Pharmaceuticals (ELOX) rises as much as 17% after Swiss drugmaker Roche reported a passive stake in the biopharma firm on Monday.

- Fusion Pharmaceuticals (FUSN) soars 26%, extending postmarket gains, after the company announced preliminary results from a Phase 1 study of cancer treatment FPI-1434.

- Microbial genetics analysis company OpGen (OPGN) jumps 24% after filings showed buying by Chief Executive Officer Oliver Schacht and Chief Operating Officer Johannes Bacher.

- Pet stocks TDH Holdings (PETZ) and Dogness (DOGZ) gain 13% and 5% respectively, extending an advance from Monday’s after-hours session, after peer Petco was touted on WallStreetBets.

- Retail trader-favorites are mixed in premarket trading, with spikes in certain names and muted moves for a few of the most prominent meme-stock names. Clean Energy Fuels (CLNE) jumps 8.1%, while AMC Entertainment (AMC) and GameStop (GME) fall 3% and 1.5% respectively.

- Spirit Airlines (SAVE) gains 2.4% after Citi upgraded the stock to a buy from neutral following “solid” 2Q update on Monday.

- Torchlight Energy (TRCH) rises 35% in premarket trading, extending a 15% increase on Monday, after the company declared a special dividend of preferred shares in connection with its combination with Metamaterial.

As Bloomberg notes, the day before the Fed’s next policy decision and possible hints about when the central bank will slow the pace of emergency asset purchases as well as a possible increase in the Fed’s IOER/RRP rates, there were few nerves on display. The statement is set to include updated forecasts, and expectations are that officials would broadcast any taper plans well in advance, and is expected to point to continued strength in the economy and acknowledge the first conversations among its policymakers about when and how fast to pare back the massive bond-buying program.

“We think that market could remain relatively complacent in a low conviction environment ahead of the Fed meeting tomorrow,” according to Xavier Chapard, global macro strategist at Credit Agricole SA. “We continue to think that starting tomorrow the Fed could be slightly less ultra-dovish than it has been. While it will try not to trigger a significant market reaction, the question is whether it will succeed.”

Complacency was also written all over the latest BofA fund manager survey in which a majority of polled investors said inflation was transitory, a marked change from March, when worries about more sustained price rises had sent U.S. 10-year Treasury yields surging to nearly 1.8%. With the yield now pinned below 1.5%, BofA expects the Fed to signal a dial back in stimulus by September.

“Several factors that have pushed up inflation are likely to fade in the coming months,” said Mark Haefele, chief investment officer at UBS Global Wealth. “We don’t expect inflation to prompt a premature tightening of monetary policy or to derail the equity rally,” Haefele added.

Nearly 60% of economists in a Reuters poll expect a taper announcement will come in the next quarter, despite a patchy recovery in the job market.

“Whilst no immediate changes in monetary policy are anticipated, an increase in the share of FOMC members who think rates will need to increase in 2023 is expected,” analysts at ANZ wrote in a note to clients. “If three more members pencil in rate rises for 2023, that would tip the majority in favour of moving rates relatively soon,” they said.

Easing inflation fears helped European shares also scale new highs, with the pan-regional STOXX 600 rising 0.2%, fading a bigger gain earlier in the session, but still its eighth straight day of gains. European equities are on their longest push into new-record territory since 1999. Germany’s DAX Index was the best-performing major benchmark, also poised for yet another record.

The Stoxx Europe 600 Basic Resources Index (SXPP) dropped for a second day after copper touched the lowest level in seven weeks over concerns over U.S. monetary tightening and a pull-back in Chinese demand. The sub-index dropped 1.4%, the biggest drop among the 20 industry groups on the benchmark Stoxx 600 gauge. Anglo American -2.8%; Glencore -1.4%; Rio Tinto -0.7%; ArcelorMittal -2.5%. Here are some of the biggest European movers today:

- CD Projekt shares gain as much as 9.6% after Sony allowed players to add Cyberpunk game to their wishlists, a move seen as signaling that a comeback for the game to the PlayStation store is nearing, and news that may trigger a squeeze on record short positions on the stock.

- Atlantia gains as much as 5.8% in Milan trading; Bestinver says dividend policy and buyback announcements are positive news as they increase visibility on shareholder compensation and should “encourage a recovery” in the stock.

- Nel shares rise as much as 7.1%, with RBC preferring Nel to ITM Power in the green hydrogen space as the risk-reward is more attractive on the former, the broker writes in notes initiating Nel at outperform and ITM Power at sector perform.

- Scandic Hotels falls as much as 3.2% after an update on its occupancy rates.

- Equinor drops as much as 2.4% after unveiling its strategy update, with Jefferies saying the shareholder renumeration policy implies a 6% yield in 2022, below most sector peers.

Earlier in the session, Asian equities advanced as continued gains in the region’s technology stocks outweighed losses in financial shares. The MSCI Asia Pacific Index rose by as much as 0.5% before paring gains. Its subgauge of information-technology stocks climbed for a fourth day, providing the biggest support. Finance sector shares slumped, led by those trading in Hong Kong, pushing the Asian benchmark lower by 0.1% at one point.

Japan’s Nikkei rose 1% and the Australian benchmark traded up 0.93%, but Chinese blue chips fell 1.1%. New Zealand was the day’s best performer, followed by benchmarks in Japan and Australia. Markets in China and Hong Kong underperformed as they resumed trade following a public holiday. China’s CSI 300 Index fell more than 1%, dragged lower by materials, health-care and financials firms. China’s markets were closed on Monday for a holiday, meaning this was their first response to a joint statement by the Group of Seven leaders that had scolded Beijing over a range of issues which China called a gross interference in the country’s internal affairs.

“Views on the outcome of the FOMC are split but with long-term yields taking a breather ahead of the event, there’s a sense of relief spreading among investors,” said Tomoichiro Kubota, a senior market analyst at Matsui Securities in Tokyo. Still, with the meeting results yet to be seen, “now isn’t the time to rush ahead in buying up stocks.” Futures on the S&P 500 rose after the underlying gauge climbed to a fresh record in New York. The Treasury 10-year yield rose to 1.50% after hitting three-month lows on Thursday amid the biggest weekly slide since December.

Japanese stocks rose for a second day amid hopes that benign inflation will enable continued global central bank support. Electronics and auto makers were the biggest boosts to the Topix, which rose 0.8% to its highest close since April 5. Tokyo Electron and Eisai were the biggest contributors to gains in the Nikkei 225, which advanced 1%. A recent calming of commodities prices may prompt the central bank to remain patient on tapering its policy assistance. “Concerns over inflation are fading for now and coronavirus cases are falling — it’s a good market environment as there are expectation for the economy to normalize,” said Hideyuki Ishiguro, a strategist at Daiwa Securities. “There is a bit of wait-and-see mode ahead of the FOMC meeting, but the Fed will likely indicate a careful exit.” Terminal users can read more in our markets live blog

In FX, the Bloomberg Dollar Spot Index was little changed as most G10 currencies were rangebound ahead of tomorrow’s Fed meeting; the euro pared a modest advance to trade little changed versus the greenback; European government bond yields were lower. The pound fell to a day low in the European session as traders weighed signs of an economic recovery in the U.K. against the government’s extension of the lockdown: U.K. companies stepped up hiring as coronavirus lockdown rules eased, delivering the biggest surge in payrolls on record. The number of employees on company books surged 197,000 in May from April. The Australian dollar led losses among G-10 peers and neared a one-week low after minutes of the central bank’s meeting showed members deemed it premature to consider ceasing the bank’s bond-buying program. The yen touched more than a one- week low as players adjusted positions. Turkey’s lira fell for a second day, continuing to shed last week’s gains after a much- anticipated meeting between the U.S. President Joe Biden and Turkey’s Recep Tayyip Erdogan failed to produce a breakthrough that would ease political tensions.

In rates, Treasury yields were steady to slightly lower, last seen just below the technical 1.50% level. The curve is steeper heading into early U.S. session as Asia advance unwinds and the long-end starts to trade heavy ahead of 20-year bond auction. Yields slightly cheaper on the day across long-end of the curve, steepening 5s30s by ~1bp; bunds lag, cheapening after the EU set a size of EU20b on its sale of 10-year recovery fund bonds A packed U.S. economic data slate is headed by retail sales, PPI and Empire State manufacturing survey. U.S. supply resumes with $24b 20-year reopening at 1pm ET; WI yield around 2.115% is ~17bp richer than May’s sale, which tailed the WI by 1bp in a weak offering.

In commodities, WTI ticked up 0.38% to $71.15 a barrel. Brent crude rose to $73.15 per barrel as talks dragged on over the United States rejoining a nuclear agreement with Tehran suggesting any surge in supply from Iran is some time away. Goldman chief commodity strategist Jeffrey Currie said oil could hit $100 (Goldman is notorious for catastrophically top-ticking oil moves; just recall their $200 target in the summer of 2008… we all know what happened next).

Even bitcoin was fairly quiet, fluctuating a little above $40,000. It rose on Sunday and Monday after Elon Musk said Tesla could resume accepting payment in the world’s largest cryptocurrency at some point in the future.

To the day ahead now, and the data highlights include US retail sales, industrial production, capacity utilisation and PPI for May, along with the Empire state manufacturing survey and the NAHB housing market index for June. The data dump could spark some modest dollar volatility, wrote analysts at CBA in a research note. Central bank speakers include BoE Governor Bailey, and the ECB’s Rehn, Hernandez de Cos, Lane, Panetta and Holzmann. And finally, an EU-US summit will be taking place in Brussels.

Market Snapshot

- S&P 500 futures up 0.13% to 4,260.25

- STOXX Europe 600 up 0.27% to 459.55

- MXAP up 0.3% to 210.54

- MXAPJ little changed at 705.39

- Nikkei up 1.0% to 29,441.30

- Topix up 0.8% to 1,975.48

- Hang Seng Index down 0.7% to 28,638.53

- Shanghai Composite down 0.9% to 3,556.56

- Sensex up 0.6% to 52,841.33

- Australia S&P/ASX 200 up 0.9% to 7,379.47

- Kospi up 0.2% to 3,258.63

- Brent Futures up 0.25% to $73.04/bbl

- Gold spot down 0.12% to $1,863.98

- U.S. Dollar Index little changed at 90.522

- German 10Y yield fell 0.9 bps to -0.260%

- Euro little changed at $1.2125

Top Overnight News from Bloomberg

- The European Union drummed up 107 billion euros ($130 billion) of orders for its debut bond sale under the recovery fund, the first sign that investor appetite is robust for the AAA-rated securities

- The cash glut in U.S. money markets has pushed rates on commercial paper down to record lows, setting the scene for Libor fixings to drop even further

- Global funds are ramping up wagers for a flatter yield curve in Australia’s $650 billion sovereign bond market ahead of a pivotal monetary policy decision by the central bank

- Real estate prices around the world are flashing the kind of bubble warnings that haven’t been seen since the run up to the 2008 financial crisis, according to Bloomberg Economics and New Zealand, Canada and Sweden rank as the world’s frothiest housing markets

- The U.K. is set to announce the broad terms of a free-trade deal with Australia on Tuesday, its latest post-Brexit accord as Prime Minister Boris Johnson seeks to expand commerce beyond the European Union

- The European Union is set to lift travel restrictions for U.S. residents as soon as this week, in the latest step toward a return to normal despite concerns over the spread of potentially dangerous coronavirus variants

A quick look at global markets courtesy of Newsquawqk.com

Asia-Pac bourses were mixed as the early positive bias following a late ramp up on Wall St that propelled the S&P 500 and NDX to fresh all-time highs, was offset after Chinese markets returned from the extended weekend and digested the increasing global criticism following the G7 and NATO summits. ASX 200 (+0.9%) followed suit to its stateside peers in which it also reached unprecedented levels with advances led by consumer stocks and financials, with risk appetite also helped after the RBA minutes affirmed the central bank’s accommodative stance. Nikkei 225 (+1.0%) was boosted by a weaker currency and although PM Suga’s cabinet is facing a no-confidence vote submitted by the opposition, the ruling party members are to vote against the motion. Hang Seng (-0.7%) and Shanghai Comp. (-0.9%) were subdued amid the global frictions as aside from being called out for human rights abuses at the G7, NATO also designated China’s behaviour as a systemic challenge. This prompted a response from China which urged NATO to stop exaggerating China’s threat and said that it does not pose systemic risks to other countries, while the announcement by the PBoC to inject CNY 200bln through its one-year medium-term lending facility did little to spur risk appetite. Finally, 10yr JGBs continue on the gradual retreat from the 152.00 resistance with demand hampered as Japanese stocks remained afloat and amid weaker headline results at the enhanced liquidity auction for longer-dated JGBs.

Top Asian News

- China Fans Liquidity Worry With Rollover That Weighs on Markets

- Singapore’s Hyflux May Get Under $151 Million in Liquidation

- Evergrande Slides After Caixin Reports Talks on Banking Stake

- Rob Arnott’s Big Bet on Emerging Markets Is Paying Off

Bourses across Europe now see more of a mixed picture (Euro Stoxx 50 +0.4%) after the region opened with broad-based gains before diverging. US equity futures see horizontal trade with the ES and NQ just off all-time highs (ATH) of 4,257 and 14,146, respectively, heading into tomorrow’s FOMC. Back to Europe, performance varies with the DAX (+0.4%) continuing to notch fresh ATHs and narrowing its distance to the 16k mark. The FTSE 100 (+0.3%) came under some early pressure due to miners’ losses as copper prices collapse. In the periphery, Spain’s IBEX (-0.5%) and Italy’s FTSE MIB (-0.3%) reside as the regional laggards – pressured by their respective banking sectors. The sectorial performance in Europe is mixed with Basic Resources, the underperformer amid price action across the base metal complex upon China’s return (see commodities section below), whilst the banking sector remains suppressed but the recent pullback in yields. Travel & Leisure is also a straddler after the UK confirmed a four-week extension to COVID restrictions for vaccinations to outpace the Delta variant. Meanwhile, the upside sees Tech coat-tailing from the sectorial performance on Wall St, whilst Construction reaps the rewards from lower raw material prices. Some of the more defensive names also reside towards the top, including Healthcare and Staples. In terms of individual movers, Airbus (+1.3%) cheers the US-EU accord on the Airbus/Boeing (+1% pre-mkt) dispute – with the suspension of tariffs seen for five years under the deal, according to sources. Meanwhile, Deutsche Lufthansa (-1.0%) reversed earlier gains seen in the wake of new targets set amid surging summer demand. Turning to commentary, BofA’s European Fund Manager Survey suggests that investors are still bullish on European equities despite the sharpest rally in decades – 51% of survey respondents expecting the bull market to continue until next year (up from 36% last month), while the proportion believing that equities will peak in H2 this year has declined from 47% to 38%. In terms of broader risks, 72% of fund managers believe that inflation is transitory; 63% believe the Fed will signal tapering in August or September – with the Fed Jackson Hole Symposium slated for August 26-28.

Top European News

- Draghi Reins In Italy State Bank That Wanted to Copy Wall Street

- Lira Declines After U.S.-Turkey Meeting Failed to Make Progress

- Rampant Variant Derails U.K.‘s Plan to Lift Virus Measures

- EU’s Landmark Bond Sale Wins $130 Billion in Orders

In FX, not the biggest G10 movers or grouped together due to their standings within the major ranks, but all potentially under the influence of expiry option interest, barring any big factor or event that may prompt a significant change in circumstances from a technical or fundamental perspective. Indeed, the Euro is among the best performers or most resilient and edged nearer 1.2150 vs the Greenback at one stage, while Sterling still seems relatively cautious when above 1.4100 following strong UK wage data and confirmation that ‘Freedom Day’ will not be next Monday, but on July 19 pending a review in another 2 weeks. Hence, the Eur/Gbp cross is probing 0.8600 and 1.1 bn expiries residing from the round number up to 0.8610, while the Yen did paring declines from 110.15 and could yet trigger 1.26 bn sitting at the 110.00 strike irrespective of the challenge against Japanese PM Suga and ongoing spread of COVID-19. Elsewhere, dovish RBA minutes and weakness in metals alongside other non-oil commodities may be undermining the Aussie, but it remains close to the 0.7700 handle and has touched the base of 1.3 bn rolling off between 0.7715-30.

- CHF/NZD/CAD/USD – The Franc rebounded quite firmly against the Buck, albeit less so vs the Euro from sub-0.9000 and sub-1.0900 lows respectively in wake of mixed SECO forecasts for growth and inflation ahead of the SNB policy review on Thursday, while the Kiwi is consolidating within 0.7161-31 extremes in advance of NZ Q1 current account data tonight and GDP on Wednesday when the Loonie will have already seen Canadian CPI for some independent pre-Fed impetus. Usd/Cad is currently meandering between 1.2129-65 amidst some retracement in oil prices and the DXY is straddling 90.500 off a lower 90.343 base vs 90.547 at best awaiting NY Fed manufacturing, PPI, Retail Sales and IP before the Usd 24 bn 20 year auction that could all impact directly or via any Treasury yield and curve reaction.

- SCANDI/EM – Somewhat divergent data and the aforementioned pull-back in crude could well be attributed to marginal Sek outperformance in relation to the Sek as Sweden’s registered jobless rate declined to 7.9% from 8.2% in May, but Norway’s trade surplus narrowed to Nok 15.5 bn from Nok 17.0 bn. Meanwhile, the Cny/Cnh have taken on board a softer PBoC midpoint fix on return from Monday’s Chinese market holiday and more post-G7 angst after NATO also delivered a damning verdict on Beijing’s behaviour, though the real EM loser is the Try on the back of Turkish President Erdogan’s insistence that the US gave the country no choice other than buying Russia’s S-400 missile system.

In commodities, WTI and Brent front-month futures remain within recent ranges around the USD 71/bbl (70.81-71.55/bbl range) and USD 73/bbl (72.79-73.56 range) marks respectively as eyes remain on the Iranian nuclear talks from a complex-specific standpoint, whilst the FOMC policy decision is on the radar for a more macro impulse. In terms of the nuclear negotiations, the prospect of an imminent deal has diminished as key sticking points remain unresolved. Analysts caution that if an agreement is not reached by the Iranian election day (June 18th), the incoming government may take a different approach that could threaten the June 24th deadline – when Iran’s extended technical agreement with the IAEA expires. The morning, however, has thus far seen an abundance in oil-related commentary at the FT Commodities and Global Summit, with the Vitol and Glenore oil heads both dismissing an oil super-cycle, whilst the former also suggests that the Iranian return to the market has been priced in and sees oil prices around USD 70-80/bbl this year owing to OPEC+ support. Aside from that, the morning has seen very little to shift the dials from a fundamental perspective, with traders eyeing US PPI data for any sentiment-induced action ahead of the weekly Private Inventory Report. Turning to metals, spot gold and silver remain steady within recent ranges. As a reminder, spot gold sees its 200 and 50 DMAs at USD 1,838 and USD 1,828, respectively – with technicians on golden-cross-watch. Focus this morning has been on the demise of copper – with 3M LME seeing intraday losses of almost USD 400/t – triggered upon China’s return from its long weekend, and with some reports overnight speculating that the largest copper consumer may attempt to stem the consistent price rise with the release of copper reserves.

US Event Calendar

- 8:30am: May PPI Ex Food, Energy, Trade YoY, est. 5.1%, prior 4.6%; MoM, est. 0.5%, prior 0.7%

- May PPI Ex Food and Energy YoY, est. 4.8%, prior 4.1%; MoM, est. 0.5%, prior 0.7%

- May PPI Final Demand YoY, est. 6.2%, prior 6.2%; MoM, est. 0.5%, prior 0.6%

- 8:30am: May Retail Sales Advance MoM, est. -0.7%, prior 0%

- May Retail Sales Ex Auto MoM, est. 0.4%, prior -0.8%

- May Retail Sales Ex Auto and Gas, est. 0%, prior -0.8%

- May Retail Sales Control Group, est. -0.5%, prior -1.5%

- 8:30am: June Empire Manufacturing, est. 22.7, prior 24.3

- 9:15am: May Industrial Production MoM, est. 0.7%, prior 0.7%, revised 0.5%

- May Manufacturing (SIC) Production, est. 0.8%, prior 0.4%

- May Capacity Utilization, est. 75.1%, prior 74.9%, revised 74.6%

- 10am: April Business Inventories, est. -0.1%, prior 0.3%

- 10am: June NAHB Housing Market Index, est. 83, prior 83

- 4pm: April Total Net TIC Flows, prior $146.4b

DB’s Jim Reid concludes the overnight wrap

With investors awaiting tomorrow’s Federal Reserve decision and their latest thinking on higher inflation and tapering, sovereign bonds sold off on both sides of the Atlantic yesterday as some jitters set in that the Fed could move to bring forward their timetable for withdrawing policy support. It wasn’t a massive selloff compared to some of the days we saw back in Q1, but yields on 10yr Treasuries were still up +4.2bps to 1.494%, which is their biggest daily move higher in over a month. And although it’s only one day, this marks a reversal from a run of 4 successive weekly declines in the 10yr Treasury yield, which coincided with investors becoming increasingly relaxed that inflation would prove transitory as the Fed has indicated, in spite of the stronger-than-expected CPI readings in the last 2 months.

It was a similar story in Europe too, where yields on 10yr bunds (+2.3bps), OAT (+3.0bps) and BTPs (+3.7bps) all rose yesterday. We had a couple of comments from ECB policymakers, although there wasn’t a massive amount of new information, with Banque de France Governor Villeroy saying that the ECB would maintain stimulus at least as long as the Fed, while Austria’s Holzmann, who’s a traditional hawk, struck a more concerned tone on inflation relative to the ECB consensus, saying that they must be vigilant on the issue.

We’ll have to see what tomorrow brings from the Fed, but global equities continued to reach new highs as they awaited the next catalyst, with the S&P 500 (+0.18%), Europe’s STOXX 600 (+0.18%) and the MSCI World (+0.24%) all climbing to fresh records. Even as global yields rose, cyclical industries weighed on the S&P, with banks (-1.58%), materials (-1.28%) and consumer durables (-1.10%) strongly underperforming. On the other hand, tech outperformed as the NASDAQ was up +0.74% and the FANG+ index was up +1.34%, in spite of some jitters over the potential for higher interest rates. This also marked a new record for the NASDAQ, which last reached an all-time high on 26 April. In Europe however, energy stocks made the biggest gains, which comes amidst a further rise in oil prices that saw Brent crude (+0.23%) reach fresh 2-year highs of $72.86/bbl. Another story to watch with implications for inflation.

Overnight in Asia, markets are seeing a mixed performance with the Nikkei (+0.73%) and Kospi (+0.16%) moving higher, whereas the Hang Seng (-0.62%) and Shanghai Comp (-0.99%) have lost ground after yesterday’s holiday. Meanwhile, equity futures in the US pointing to yet further highs for the main indices, with those on the S&P 500 up +0.13%, though yields on 10yr US Treasuries have softened slightly from yesterday, having fallen -1.0bps to 1.484%. However, commodities are generally trading a bit lower this morning with copper futures down -2.62%, DCE iron ore futures down -1.48% and SHF steel rebar futures down -2.36%.

Turning to the geopolitical sphere, the NATO summit yesterday once again demonstrated the deterioration in relations between China and many Western nations after the communique issued said that “China’s stated ambitions and assertive behaviour present systemic challenges to the rules-based international order and to areas relevant to Alliance security.” This follows the G7 summit over the weekend in which President Biden said that he wanted the “Build Back Better World Partnership” to be an alternative to China’s Belt and Road Initiative. The succession of summits will actually continue today as Biden is set to meet with EU Commission President von der Leyen and Council president Michel in Brussels. This is the first EU-US leaders’ meeting since 2017, and the two sides are expected to discuss the pandemic, climate change, trade issues and foreign policy. We’ve also had a report from the FT overnight that the EU and the US are looking set to resolve the trade dispute over Airbus and Boeing, with a deal likely to be a multiyear agreement on subsidy limits. Finally, another deal that looks possible is a trade agreement between the UK and Australia, with the BBC reporting that there’ll be a formal announcement today.

Back in the US, there are still divisions among President Biden’s Democratic colleagues on whether they should work with Republicans to pass a smaller infrastructure package through a bipartisan process or pass a larger, more-encompassing bill that would also address climate change but would need to be passed on a straight party line vote. A group of 10 Senators, made up of 5 more moderate members from each party, submitted their bill late last week for $579 billion in new spending and cost $1.2 trillion over the next eight years. The plan does not change any of the Trump tax cuts or an increase to the gas tax, but it also does not have the child care or elderly care initiatives that President Biden has advocated. The overall size of spending and any tax changes will be entirely dependent on which wing of the party Democratic leadership sees as more vital to its passage.

Staying on the political theme, it’s a little more than 3 months to go until the German election now, and our research colleagues there have put out a new note (link here) following the Green party convention that looks at their policies as well as potential coalition options. They’re sticking to their baseline call of a conservative-green coalition afterwards, though they say that it’ll require compromises on both sides, most likely on climate policy for the CDU/CSU, and tax policy for the greens.

In terms of the latest on the pandemic, UK Prime Minister Johnson announced that he would be delaying the planned easing of restrictions in England for 4 weeks, so that limits on social gatherings would now be removed on July 19, rather than Monday as had previously been hoped. He said that by that point they aimed to have given 2 doses to around two-thirds of the adult population, although it was announced that rules on weddings would be eased slightly so they could happen with more than 30 people if social distancing remained in place. The move to prolong restrictions comes amidst the spread of the delta variant in the UK, with yesterday seeing a 6th consecutive day of cases above the 7,000 mark. That said, relative to earlier in the year, the distribution of cases in England is much less focused on the oldest age groups, which is something we looked at in Jim’s chart of the day yesterday (link here).

In better news on the pandemic, we did get confirmation that the vaccines were still broadly effective at preventing hospitalisations as a result of the delta variant. According to Public Health England, the Pfizer-BioNTech vaccine was 96% effective against hospitalisation after 2 doses, and the figure was 92% for the AstraZeneca vaccine. Meanwhile, a Pfizer official said that they would examine cases where fully vaccinated people caught Covid-19 to decide if and when boosters are needed. And in other vaccine news, Novavax reported that their Covid-19 vaccine was 90% effective in a late-stage trial with 100% protection against moderate and severe disease.

There really wasn’t much data of note at all yesterday, though we did get the Euro Area’s industrial production for April, which grew by +0.8% (vs. +0.4% expected). Separately in the US, the New York Fed’s Survey of Consumer Expectations for May saw the median one-year-ahead inflation expectations rise to +4.0%, which was its highest since the series began in 2013 and the 7th consecutive increase.

To the day ahead now, and the data highlights include US retail sales, industrial production, capacity utilisation and PPI for May, along with the Empire state manufacturing survey and the NAHB housing market index for June. Meanwhile in Europe, there’s also April data on UK unemployment and the Euro Area trade balance. Central bank speakers include BoE Governor Bailey, and the ECB’s Rehn, Hernandez de Cos, Lane, Panetta and Holzmann. And finally, an EU-US summit will be taking place in Brussels.

Tyler Durden

Tue, 06/15/2021 – 07:54![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com