Industrial metals such as copper continue to stagnate this year as major funds take an increasingly bearish view on global macro.

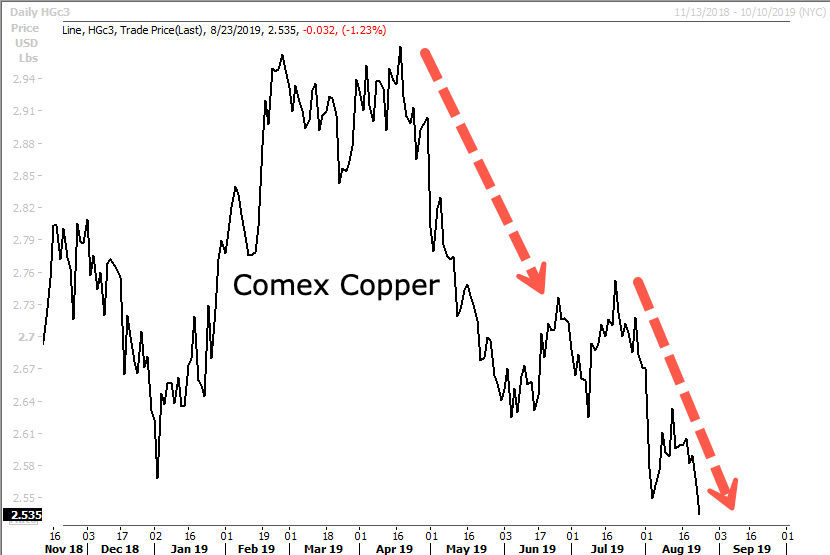

The spot price of Comex copper on Friday fell 1.23% to 2.535, the lowest level in at least 115 weeks, dating back to the summer of 2017.

Copper dropped 3.34% this past week amid new fears the US economy is quickly slowing. IHS Markit’s flash reading for the manufacturing purchasing managers index, recorded 49.9 for August on Thursday, the first contraction since 2009. This is an indication a manufacturing recession could be imminent, seems plausible since a freight recession across is already underway; explains how the Trump bump in the economy has been exhausted and reveals further why President Trump is demanding 100bps rate cuts, quantative easing, and emergency payroll taxes: it’s because the cycle is rolling over. We even mentioned last week how President Trump might hold an emergency meeting next week with advisors and top donors about how a mild recession could materialize before the 2020 election.

In the last 89 days, copper is down nearly 15% from its high in April.

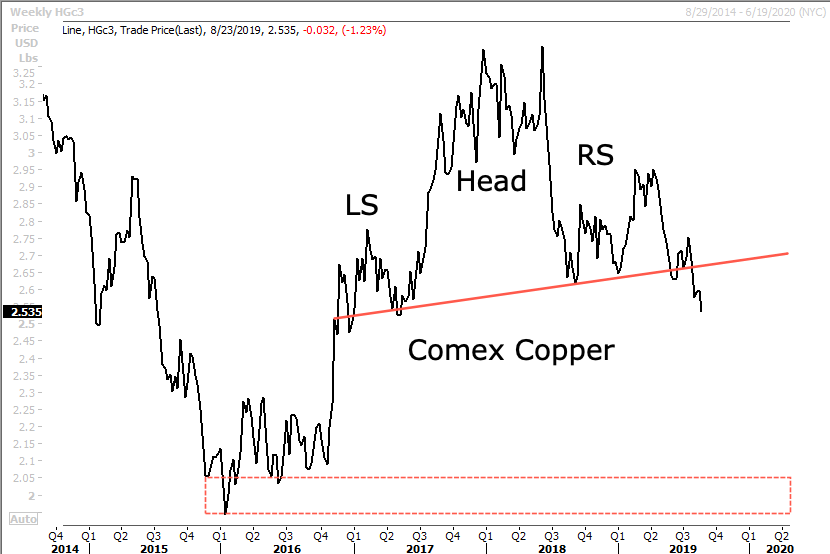

On a longer perspective, copper crashed -58% from early 2011 to January 2016. Copper prices eventually troughed at 1.94 around mid-January 2016, as global central banks pumped the world with liquidity in 2016, and then the Trump administration in 2017 and 2018 injected fiscal stimulus into the domestic economy, which helped copper prices soar 62% until June 2018. Prices then plunged into late summer and fall of 2018, by 21% as the world realized a global slowdown was developing.

The rollercoaster in prices, up and downs, created a massive head and shoulder pattern that could be completed in 2H19, or at least some time in 1H20. This would be due to another growth scare that could shock world markets. If copper was to break the head and shoulders neckline, a possible retest of 2016 levels, around 2-2.15, could be likely.

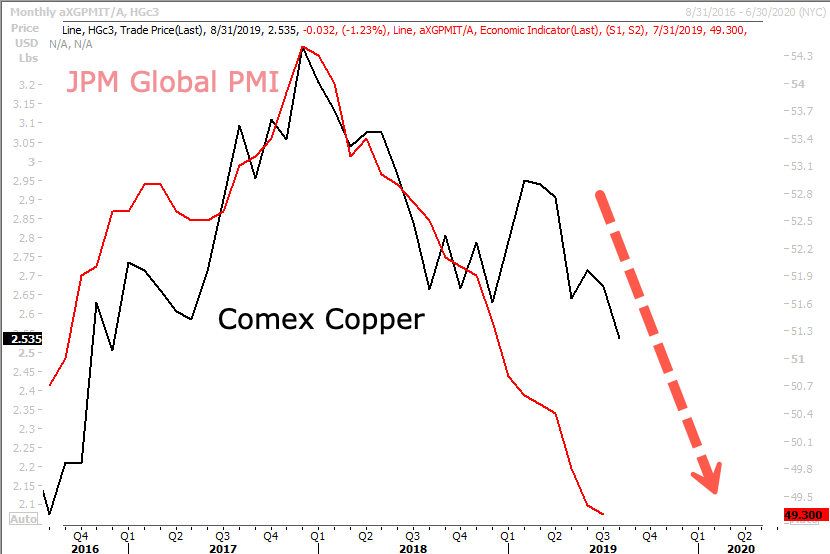

In textbook commodity market fashion, the price slump has been associated with a J.P.Morgan Global Manufacturing PMI plunging to sub 50, a harbinger that a global manufacturing recession could be imminent, or is already underway.

The Wall Street Journal said, “Net bearish bets on copper in futures markets hit their highest level in around three years earlier this month, a sign that investors have grown increasingly pessimistic on the outlook for the metal in the midst of slowing global growth and a weakening Chinese economy.”

China is the world’s largest copper user, accounting for almost 50% of global demand.

So when copper prices slump, it’s also a proxy of the health of the Chinese economy.

Earlier last week, Fathom Consulting, a global independent macro research consultancy, said its proprietary China Momentum Indicator 2.0 has slowed to 4.6% in June, the lowest reading since Aug. 2016.

There is also a growing gap between the China Momentum Indicator 2.0 at 4.6% and official GDP data at 6.2%. Might suggest China’s economy hasn’t yet bottomed, could continue to decline through 2H19 into 1H20.

And on Friday, to make matters worse for the global macro outlook, China’s Ministry of Finance said in a statement that it would levy retaliatory tariffs on another $75BN in US goods with rates anywhere between 5 and 10%, with the tariffs set to be implemented in two batches, one at midnight on Sept 1 and another at midnight on Dec 15.

Additionally, China said it would resume 25% tariffs on US autos, stating that “China’s adoption of tariff-adding measures is a forced move to deal with US unilateralism and trade protectionism.”

Then in a retaliatory move, President Trump announced starting Oct 1, the existing 25% tariffs on $250BN in Chinese goods would rise to 30%, and the 10% tariffs on $300 billion in Chinese goods set to begin on Sept 1 will be 15%.

With that being said, the global macro outlook looks set to deteriorate further into 1H20, sending copper prices tumbling much further.

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com