Shades Of 2007: Subprime Auto Lender Verified Income On Only 3% Of Loans In Latest Bond

The US subprime auto industry is doing everything in its power to recreate another 2008 crisis. After all, it takes a (Potemkin) village.

One of the largest subprime auto finance companies, Santander Consumer USA Holdings, verified the income on less than 3% of borrowers this year, according to Bloomberg. And in painfully vivid shares of 2008, it then took those loans and bundled them into more than $1 billion in bonds sold this year.

This laughable number which was taken straight from the Countrywide playbook (“If they can fog a mirror, we’ll give ’em a loan“) was down from 17% for loans for various asset-backed securities issued as recently as 2017. For comparison, GM Financial’s AmeriCredit, another major ABS issuer, verified income on about 68% of loans for a deal it priced in June and 66% of loans that it priced for a deal in March, according to Bloomberg.

And no, you didn’t read that wrong: according to Moody’s – which this time has no intention of getting blamed for the bursting of the biggest asset bubble in history – Santander’s ABS priced in June had 2.6% of loans verified for income and the one priced prior to that had 3.2% checked.

Another transaction being marketed by Santander will also be in the 3% range “or possibly lower”, said Moody’s analysts. Borrowers involved in the bond that Santander is currently marketing have an average FICO score of 581 and are paying an average annual interest rate of 18.9%.

What can possibly go wrong? Oh wait, everything, because as Bloomberg notes, these ridiculously lax underwriting standards is why expected losses on Santander subprime auto bonds are higher than bonds from its peers, Moody’s analyst Nicky Dang said. Moody’s expects average losses up to 17% for loans underlying the bonds from Santander’s typical subprime series of transactions, although it forecasts losses of 24% for the deal currently marketing, which is from a deeper subprime series. In comparison, expected losses for comparable peers are roughly half, and stand at about 10% for similar subprime auto ABS from GM Financial.

The decline in Santander’s income verification levels suggest the obvious that there is a higher chance of borrowers having weaker credit profiles than they have stated.”

Santander didn’t comment, but instead pointed to information on its earnings calls stating that the percentage of income verification has decline as the company is working to refine its processes of screening high risk dealers and borrowers from its securitizations. Meanwhile, we guess that just means give up on income verification altogether?

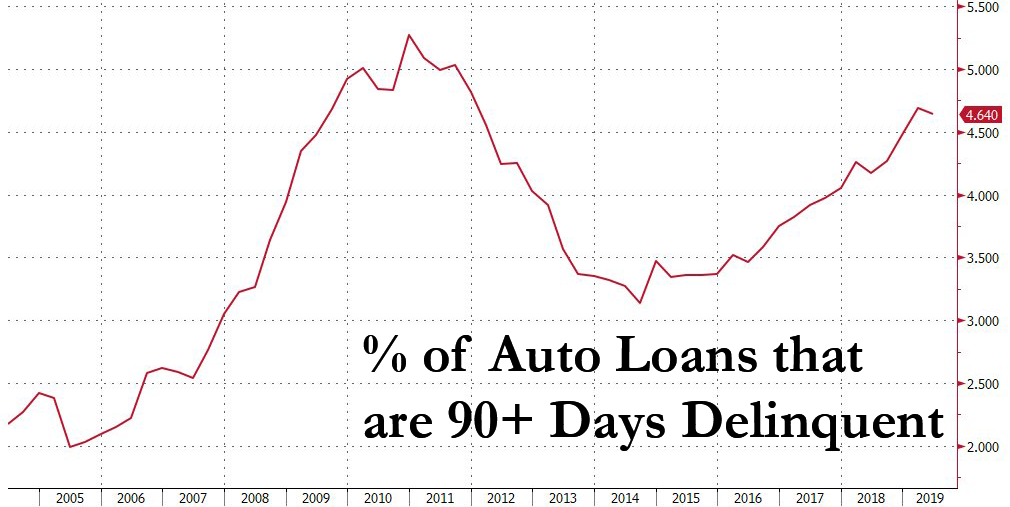

Santander also claims that the “performance of those transactions has been consistent or better than the historical deals that had a higher percentage of income-verified loans.” We’ll check back in on this statement in 12 months, although at the rapid surge in 90+ day delinquent auto loans, we doubt we will have to wait nearly that long.

Meanwhile, ratings firms have demanded higher levels of credit protection in deals over recent years to mitigate increasing delinquencies in underlying loans, although judging by Santander’s actions, they did not get them.

Moody’s Dang said: “Income verification is only one part of the entire underwriting process for the loans. It’s only one factor that is baked into the historical deal performance we’ve seen, which has generally been consistent and stable.”

Then again, considering that one of the biggest subprime auto lenders barely bothers with any income verification we won’t be holding our breath to find out just how much more thorough it has been with the remainder of underwriting process checklists. On the other hands, those who naively hold their money at Santander, may want to consider doing just that as their funds now appear to be collaterlized by billions in worthless subprime auto bonds.

Tyler Durden

Tue, 09/10/2019 – 04:15

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com