The World’s Best And Worst Pension Funds

With the global population aging at a rapid pace (research has determined that the percentage of the population over the retirement age will grow to 20% by 2070, up from 9% today), understanding the durability of the world’s pension funds is of growing importance.

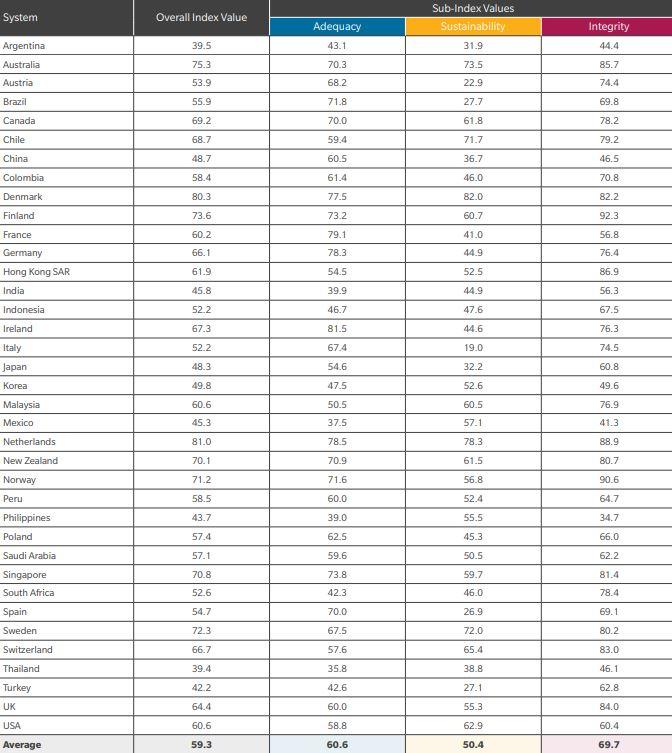

Hence, the Melbourne Mercer Global Pension Index, a study of 37 retirement income systems covering more than 63% of the world’s population, has been created to reflect the “great diversity between the systems around the world with scores ranging from 39.4 for Thailand to 81.0 for the Netherlands.”

Pension funds are not only a critical source of retirement income, they play a significant role in financial markets, mandating a growing need for accurate information about the comparisons between different countries, said Martin Pakula, Australia’s minster for jobs, innovation and trade, in a preface released with the study.

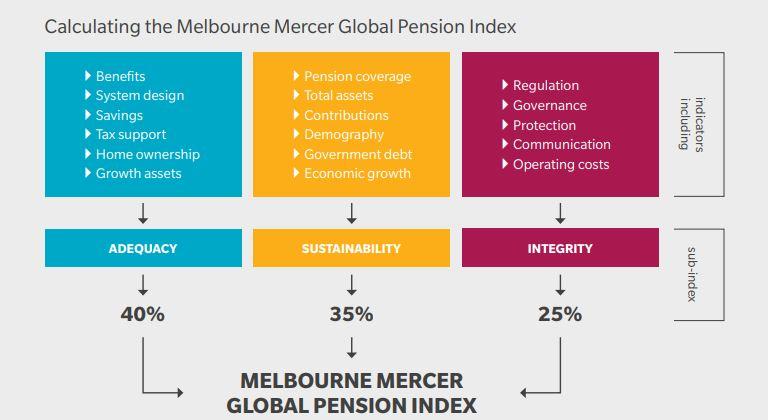

Here’s how the index works: The overall index value for each system represents the weighted average of three sub-indices. The weightings used are 40% for the adequacy sub-index, 35% for the sustainability sub-index and 25% for the integrity sub-index which have remained unchanged since the first Index was published back in 2009.

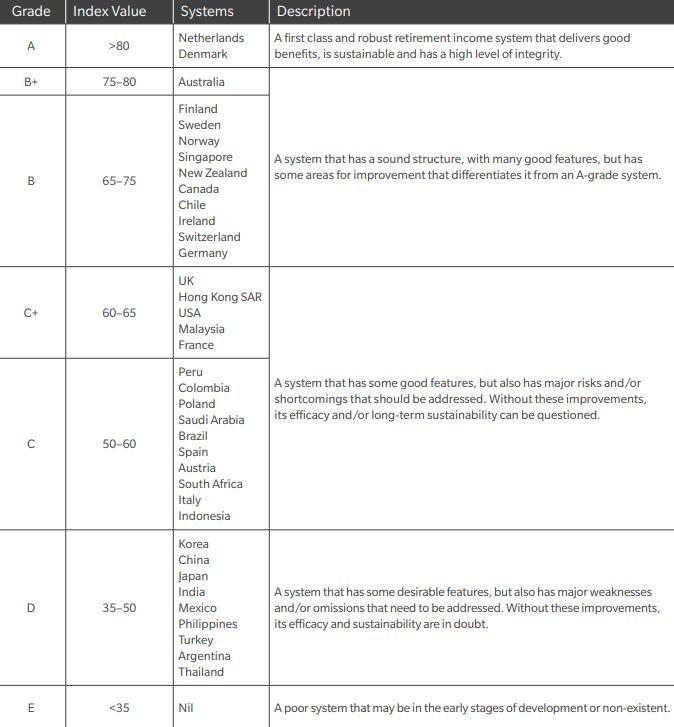

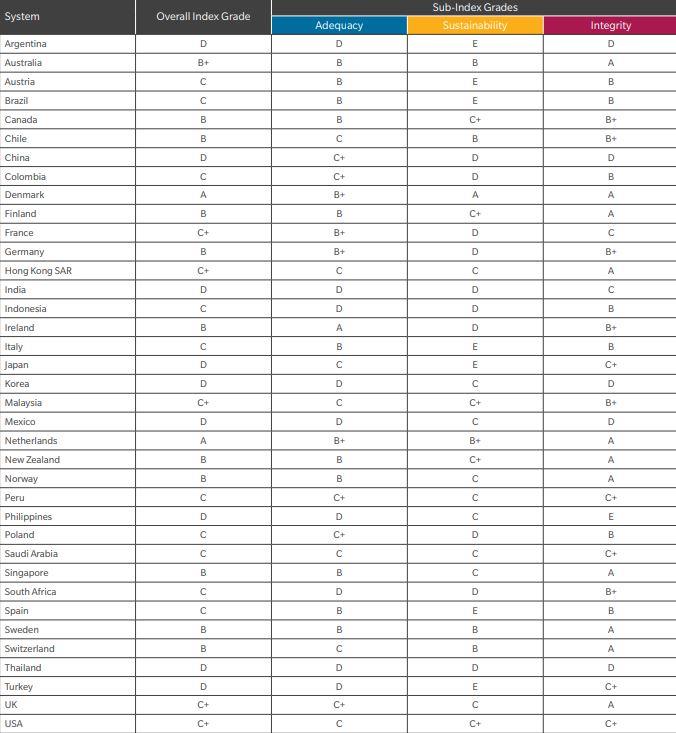

This year’s study confirmed that the Netherlands and Denmark again received A-ratings, confirming that they remain the best systems and most sustainable pension systems.

Below, is a run-down of all the country’s included in the study and their numerical ranking (in alphabetical order).

And this chart shows the letter grade received by each…

Part four of the study includes several recommendations for how low-scoring systems can improve (text courtesy of the study):

- Increase the state pension age and/or retirement age to reflect increasing life expectancy, both now and into the future, thereby reducing the costs of publicly financed pension benefits3.

- Promote higher labour force participation at older ages which will increase the savings available for retirement and limit the continuing increase in the length of retirement.

- Encourage or require higher levels of private saving, both within and beyond the pension system, to reduce the future dependence on the public pension while also adjusting the expectations of many workers.

- Increase the coverage of employees and/or the self-employed in the private pension system, recognising that many individuals will not save for the future without an element of compulsion or automatic enrolment.

- Reduce the leakage from the retirement savings system prior to retirement thereby ensuring that the funds saved, often with associated taxation support, are used for the provision of retirement income.

- Review the level of public pension indexation as the method and frequency of increases are critical to ensure that the real value of the pension is maintained, balanced by its long-term sustainability.

- Improve the governance of private pension plans and introduce greater transparency to improve the confidence of plan members.

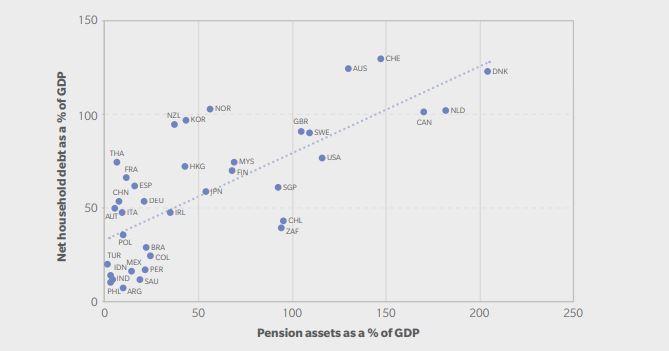

While also charting an “interesting” relationship between household debt and the relative performance of a country’s pension system, implying that household debt is higher in nations with better-performing pension systems – the so-called “wealth effect.”

Regular Zero Hedge readers are no doubt familiar with our pension coverage, especially as the largest pension funds in the US are on track to miss their targets again in 2019, just look at how much risk remains around the world, as underfunded pensions far outnumber their well-funded peers.

Tyler Durden

Fri, 10/25/2019 – 23:00

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com