The Fed Has ‘Absorbed’ 90% Of Treasury Issuance Since September

Authored by Lee Adler via WallStreetExaminer.com,

Let’s look at a few of Chairman Powel’s words at yesterday’s press conference. Please read them and tell me whether this sounds to you like a man who doesn’t understand what he’s doing. Or if you think he’s deliberately pulling words out of his ass, stringing them together, and spewing them from his mouth in an effort to gaslight the investing public.

I’ll take the latter. The Fed is in the propaganda business. It knows what it is doing. Double talk, lies, and utter bullshit are its stock-in-trade.

Liquidity moves markets!

Follow the money. Find the profits!

Powell’s spew was in response to a question from the confused but affable Michael Mckee of Bloomberg, who no doubt served up the question on a suggestion from his Fed handlers.

McKee: The BIS concluded in September that the repo spike was not a one off confluence of random events but reflected structural and regulatory issues that could lead to a recurrence.

This is the utter nonsense that the Fed and Primary Dealers who own Wall Street want you to believe. The fact is that the dealers and banks could no longer continue to help finance the burgeoning Federal debt. They had reached the end of their willingness, and/or their ability, to continue to use repo funding from each other to fund the growing flood of Treasury issuance.

McKee: I’d like to ask you if you agree with the BIS findings and given that we are approaching year-end for the markets will you be taking any extra steps to ensure that funding is available in the repo and FX swaps markets.

There was a report yesterday, Credit Suisse suggesting there’s a good chance that we will see disruptions and one of the reasons they December 11, 2019 put it forward is that the Fed is at this point buying only T-bills and the market wants to sell coupons, do you have any plans to sell coupons?

I believe that McKee meant to ask if the Fed has any plans to buy coupons, not sell them. But his question was almost as nonsensical as Powell’s response, so it’s hard to know what he meant.

But there’s no mistaking what Powell meant. Gaslight garbage. I’ll try to explain why as we go through this.

I put Powell’s stream of BS into paragraphs, in an attempt to make some sense of it. I have bolded statements that I felt were particularly absurd or critical. And I have interjected a few facts between Powell’s horseshit, to help you make sense of it.

Powell: So, I’m going to take a little step back and I will get to your specific questions on the year-end and on T-bills.

So I guess I want to start by stressing that these are very important operational matters, but that are not likely to have any macroeconomic implications.

The Fed is pumping $145 billion per month into the system. That’s more than under QE One. Powell has said that it’s Not QE, and now says that it won’t have macroeconomic effects. Oh please. Humor me.

Powell: We’ve decided back in January to remain in an ample reserves regime…

The obvious question here is, “Why?” And the answer is that if they hadn’t reversed course from shrinking their balance sheet, the stock and bond markets would have crashed, and short term rates would have soared.

And something very bad would have happened to the US economy. In other words, there would have been macroeconomic second order effects. True, the first order effects would have been in the money markets and the asset markets. But to say that the policy change has no macroeconomic effects is hogwash.

In fact, the money market freeze-up happened first, and the Fed started “Not QE” in September in instant response.

Powell: …and that means we’ll be setting the federal funds rate, the range for the federal funds rate, through our administered rates and not to active management of the level of reserves.

Gibberish.

Powell: We’re committed to robustly implementing that framework as you can see by our actions.

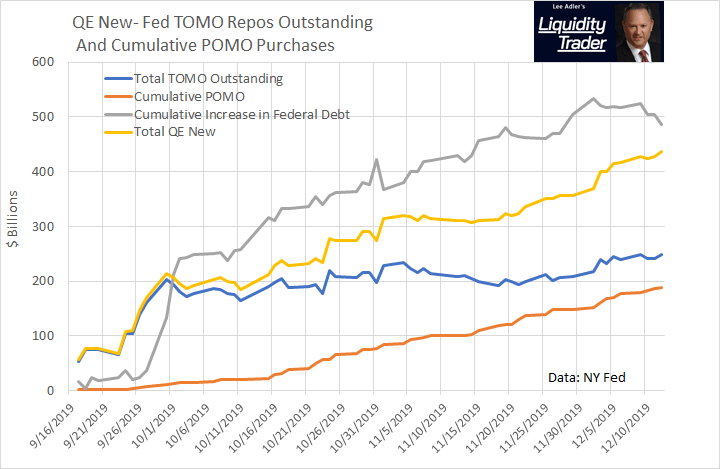

I’ll say. $435 billion in Not QE so far, since September 17.

Powell: And the purpose of all this, let’s remember, is to assure that our monetary policy decisions will be transmitted to the federal funds rate, which in turn affects other short-term rates. We have the tools to accomplish that and we will use them.

The purpose of all of this is not to eliminate all volatility particularly in the repo market.

No, the purpose is to absorb enough of US government debt issuance to keep rates down. As of right now, so far that has meant 90% of all new issuance. The Fed is effectively monetizing the US government debt!

Powell: So taking you back this as you know we had, very gradually allowed the balance sheet to shrink, we slowed that gradual paced by half in March, and then we ended it in July.

Prior to the Trump Regime and Congress lifting the debt ceiling, there was no pressure on the money markets because debt issuance was reduced while the debt ceiling was in place.

But the Fed saw the devil’s budget deal coming and knew that the Treasury would soon be crushing the market with new debt that the market would not be able to absorb. The Fed knew at that point that it would no longer be able to continue removing reserves from the system under its balance sheet bloodletting program, so it stopped.

Powell: Meanwhile we had surveyed all of the banks, and particularly the large banks who hold a lot of the reserves and said what’s your lowest comfortable level of reserves? We got those numbers, we added them up, we added a buffer and it came out sort of at a level that was well below when we were in September.

And yet we saw actually in September that reserves– the markets acted as though reserves had become scarce. So what had happened was that liquidity which actually existed didn’t flow into the repo market and that had effects on the federal funds rate.

So the question is, why did that happen? And we’ve been very carefully looking at the reasons why that might have happened there are payments issues, there have been a number of supervisory and regulatory issues raised, we’re looking carefully at those.

They know damn well why it happened. The only way the market could finance all that Treasury issuance was through repo borrowing. That, folks, is margin debt plain and simple. The dealers and the banks were buying up Treasury issuance on 90% margin. In September, they said, No mas! They’d had enough.

I have shown you this chart before. The banks had been expanding their repo borrowing at an annual rate of an astounding 40% to 60% throughout 2019, and that was on top of a 20% growth rate in 2018. Their repo borrowings rose from the $350-400 billion range in 207 to $850 billion at the peak in September.

And the Fed and Wall Street are blaming regulatory bottlenecks? Give me an effing break.

The fact is that the overleveraged dealers with their bloated inventories know that any downtick in bond prices will destroy them and destroy the system. And the Fed knows it equally well. Because, as Powell noted, they talk to each other all day, every day in the context of their debt market rigging operations.

So, what follows is utter horseshit.

Powell: We’re open to ideas for modifying supervisory and regulatory practice in ways that don’t undermine safety and soundness and the number of ideas, are under examination there.

To go through with sort of like in time, we started off really on September 17th with overnight operations, by October 11th we had created and put into effect to plan, that plan is in effect.

It’s working. I think for the last couple of months, repo markets have been functioning well, short-term rates are stable, markets are functioning.

Of course it’s working. They’ve pumped $437 billion into the banking system in less than 3 months. They have absorbed 90%, NINETY PERCENT! of all Treasury issuance over that time.

And you wonder why there are asset bubbles.

Think about how screwed the system must be, and would be, if the Fed were not monetizing the debt at this point.

But hey! There’s nothing to see here. Move along.

Powell: So you asked about year-end, temporary upward pressure is on short-term, money market rates are not unusual around year-end. And our– both our repo operations and Treasury bill purchases are intended to mitigate the risks that such pressures pose to our control of the federal funds rate.

We think that the pressures appear manageable and we stand ready to adjust the details of our operations as necessary to keep the federal funds rate in the target range.

Our strategy has been– essentially the key to our strategy is to supply reserves in the near term through both overnight and term repo.

And at the same time we’re raising the underlying level of reserves through bill purchases. I’ll take that now.

We’ve said bills– bill purchases, so we’ve also said that we were willing to adopt our strategy. We’re not at this place but if it does become appropriate for us to purchase other short-term coupon securities, then we would be prepared to do that if the need arises.

So there you have it. It may not be enough for the Fed to absorb 90% of Treasury issuance. Maybe it will take all of it. Or maybe they’ll even print a little extra cash to keep inflating stock prices.

Powell says that they stand ready to increase Not QE even beyond the $145 billion per month pace that they have established so far.

I mean, who knows how far they’ll take this insanity? And who knows what the unintended consequences will be? That, I doubt even the Fed knows.

But watch the 10 year yield, my friends. It’s not cooperating. Holders of bonds, likely including dealers, are liquidating them. If that doesn’t stop, it’s going to make big trouble. The dealers are so leveraged that they will quickly become insolvent, if they haven’t already, and the Fed will then become the permanent market maker for everything, much like the Bank of Japan.

Powell: So, but we don’t– we’re not in that place it looks– it very much looks like the bill. So those bill purchases are going well just according to expectations.

I mean, the other thing I’ll say is that we’re in, you know, very regular contact with market participants all the time.

We’ll be providing, we’ll be continuing that and we’re prepared to adjust our tactics. We’re focused on year-end as well and prepared to adjust our operations as appropriate.

Does that sound like a confident man to you?

Such is the Fed’s confidence game. It has no choice but to play it. The system is in just that bad a place.

God forbid any seriously big investors start to figure it out and decide to take their marbles out of the game and go home.

* * *

Follow this story in depth at Liquidity Trader. Know what’s coming next and what to do about it. 90 Days Risk Free If You Join Now! Get current reports and access to past reports. Read Lee Adler’s Liquidity Trader risk free for 90 days! Satisfaction guaranteed or your money back.

Tyler Durden

Fri, 12/13/2019 – 08:47

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com