“Reckless” Fed-Liquidity-Driven Momo Meltup Is Creating “Dangerous Market Conditions”

Authored by Sven Henrich via NorthmanTrader.com,

Watch This!

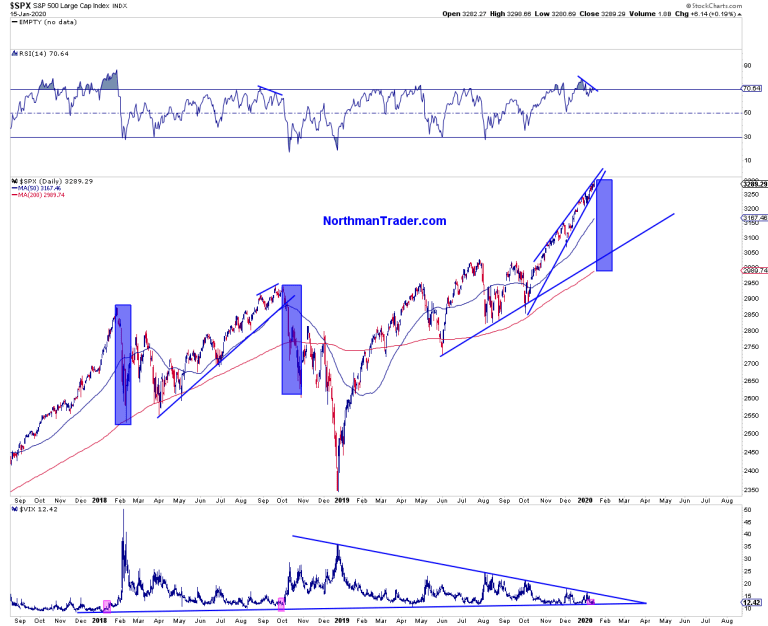

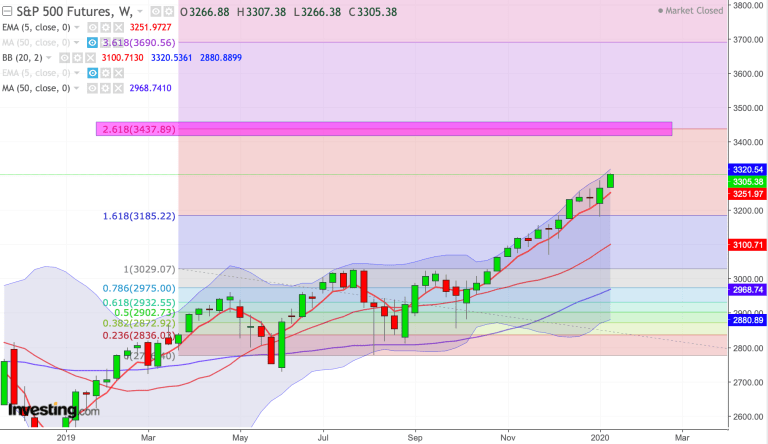

Don’t tell the complacent but the never ending rally is becoming ever more dangerous. As $ES is currently trading above 3300 it’s now not only extending over 10% above the 200MA it is also now already within a stone’s throw of what used to be considered aggressive price targets for year end of 2020. On January 16. Lol.

Recall on December 16 BAML called for an aggressive front loaded $SPX target of 3,333 by March 3. Heck, we may get there this week. More lol.

And of course at 3305 $ES is already a mere 3%-5% from the highest 3,400-3,500 year end targets outlined by several Wall Street analysts baking in good news and earnings growth:

As if earnings still matter. They didn’t last year. At the current rate of continued levitation $SPX would simply need another few weeks to get to these targets.

Of course we know why all his happening. I’ve talked about it in Ghosts of 2000, Repo Lightning and He Knows.

Yesterday Dallas Fed President doubled down on admitting it as well: The Fed’s behind it all.

“Recent Federal Reserve interest-rate moves seem to have given investors a green light to buy risky assets and this is a concern, said Dallas Fed President Robert Kaplan on Wednesday. “I’m conscious all three of those actions are contributing to elevated risk asset valuations and I think we ought to be sensitive to that at the FOMC and I certainly am,” he said.

While the Fed’s recent purchases of short-term Treasury bills is not technically quantitative easing (QE) because the Fed is not buying securities all along the yield curve, it is having similar effects, he said.

“My own view is [buying bills] is having some effect on risk assets. It is a derivative of QE in that when we buy bills and we inject more liquidity, it affects all risk assets,” Kaplan said.

“Growth in the balance sheet is not free. There is a cost to it,” he said.”

He knows, they know, we know. What we’re seeing here is all the Fed, nothing else.

And as such the liquidity program is relentlessly driving asset prices higher and stretching charts and producing massive technical disconnects.

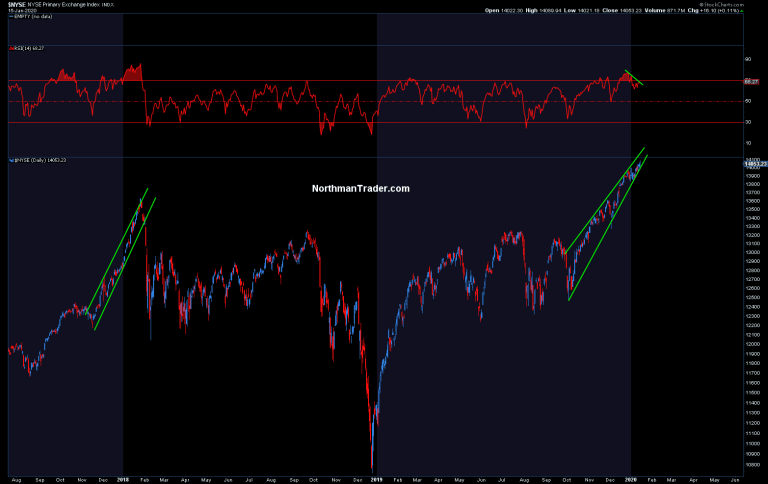

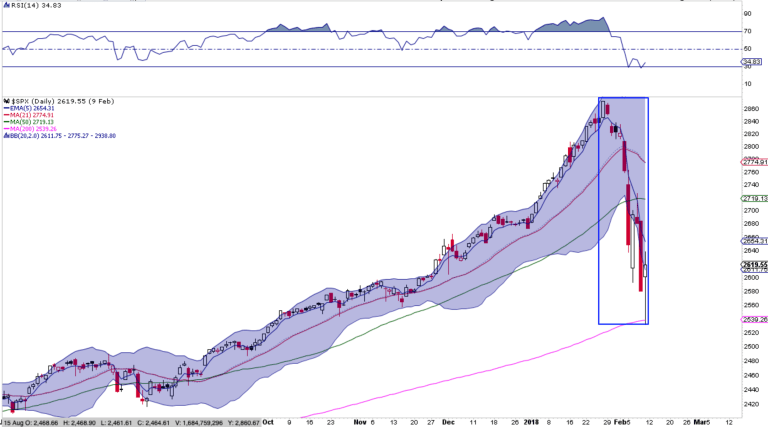

As such this liquidity event is not that different from the one we saw in the lead up to the January 2018 blow-off top:

Relentless, vertical one way action, massive overbought readings and then suddenly a risk reversion that came suddenly and within a 9 day period 3 months of relentless buying were wiped out.

Could something similar set up here? Possibly. Certainly within the realm of possibilities.

Here was the run up to January 2018:

On the way down it sliced through all the support and didn’t stop until the 200MA.

Back then $SPX extended over 13% above its 200MA. Currently $SPX is 10% extended above its 200MA with $VIX very much compressed.

Watch this:

Liquidity driven momentum rallies can keep going beyond all reason or fundamental basis, that’s what bubbles are all about.

The Fed knows what it’s doing and keeps insisting on doing it:

Repo and balance sheet expansion was forced upon the Fed.

They admit it’s causing a melt-up in asset prices.

Their actions are driving the bubble.

Yet they keep doing it.

The is Fed is reckless, irresponsible and hopelessly trapped.— Sven Henrich (@NorthmanTrader) January 16, 2020

https://platform.twitter.com/widgets.js

As the liquidity machine remains in operation one can’t exclude the possibility that this keeps going. Who’s to say it can’t? A repeat of January 2018 with a 13%+ extension above the 200MA would drive $SPX cash into the 3400 zone.

In Popping the Bubble I talked about a technical fib zone just above as a technical possibility:

Am I calling for this move from here? No. I’m merely pointing out the technical precedence following a massive liquidity event. Tax cuts back then, Fed printing now. And hence such a repeat cannot be excluded as a possibility.

At the same time patterns and valuations are so stretched that this market remains under immediate reversion risk and once that reversions triggers (markets will find an excuse) then it’ll become a matter of Fed control and technical support levels to determine where the correction then stops and runs its path. So yes, in a way I’m saying we can keep going up while at risk of reverting at any moment. I’m saying this because that’s the reality of the situation.

I maintain that volatility is setting up for an event and this Fed driven liquidity momentum rally is producing reckless behavior and dangerous market conditions, none of which will matter until a reversal kicks in. But when it does, not if, watch this. It will be fast and furious.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

Tyler Durden

Thu, 01/16/2020 – 15:05

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com