SaxoBank: Our View On The Short Squeeze In Tesla Shares

Submitted by Peter Garnry of SaxoBank

Summary: Tesla shares have exploded this year burning short sellers and the last two trading sessions have been an outright short squeeze detaching Tesla from meaningful fundamentals. It is quite likely that the stock will normalize. How it plays out and when we don’t know, but if investors want to play any normalization we go through the various options and the risks associated with them.

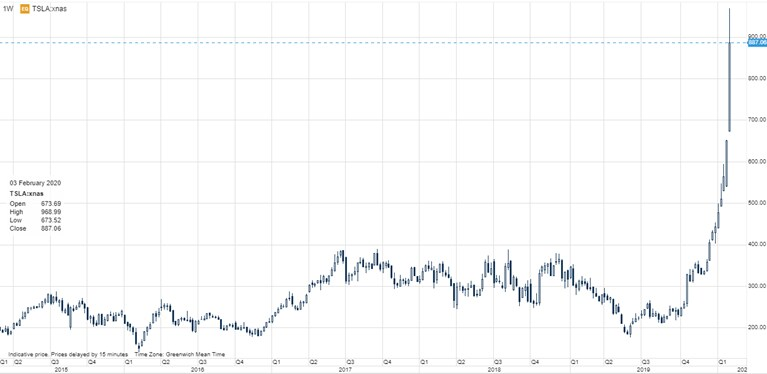

Tesla shares are up 36% in the last two trading sessions and up 111% year-to-date. We are observing a classic short squeeze where many short sellers are forced to reduce their position. The interesting math of short selling is that a short position increases in exposure (weight in the portfolio) as the position goes against you which is opposite of what is happening on long positions. So if a stock declines that you have short then you short even more to maintain the same risk exposure in the portfolio.

The price action in Tesla is compounded by other market participants smelling fatigue and weakness among the entrenched short sellers in Tesla. So they are forcing short sellers to buy back some of the shares they have borrowed. But several short sellers have openly said that they are continuing to short and new short sellers are taking the risk at current levels.

Depending on the will of the buyers trying to shake the short sellers and the short sellers’ stubbornness this short squeeze might not be over just yet. But everyone agrees that the move is not based on fundamentals and Tesla’s shares cannot support this market valuation of $160bn. That means that the market will most likely normalize Tesla’s shares at one point, but we want to stress that we don’t know when and how much the normalization will go.

But if investors believe Tesla shares will be down in the near term future how should investors do it?

If investors are shorting a delta one instrument (shares or CFDs) on Tesla then timing is everything and the potential losses are unbounded so this approach has extremely high risk. Another approach is to buy put options on Tesla. The current market price (premium) on a put option at-the-money with expiry on Friday next week is around 10% of the underlying. The put option provides the investors will pre-defined maximum loss (premium + commission paid) that cannot be exceeded. In such a volatile environment this maximum loss characteristic is attractive. But the risk with the option is naturally that the investor pays a high premium for a short period and thus could end up losing 10% of the underlying in a short period.

Tyler Durden

Wed, 02/05/2020 – 09:10

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com