Portfolio Management In An Era Of ‘Greater Fools’

Authored by Michael Lebowitz and Jack Scott via RealInvestmentAdvice.com,

U.S. Treasury bonds of all maturities have recently flirted with zero percent yields and, in the case of some Treasury Bills, have at times traded at negative yields. As a result, these bonds are closing in on the same “greater fool” status, which plagues sovereign and corporate bond investors throughout Europe and Japan.

We use the term greater fool to describe a market circumstance in which overvalued conditions are so extreme that foolish participants must rely on an even greater fool to whom they may sell their holdings to profit.

In the case of the U.S. Treasury market, the fool is the buyer of bonds at meager yields. The greater fool is an “investor” that he or she thinks will buy it at an even lower yield in the future.

Since the yield is minimal and the risk extensive, the fools either believe that yields will fall further, which in this case implies negative yields or that the future rate of deflation will be even lower than the bond yield.

Fixed-income assets play a vital role in every well-thought-out, prudent wealth management strategy. Investors use treasuries, corporates, mortgages, other bond classes, and related securities for a wide range of purposes, including, but not limited to cash flow administration, risk management, diversification, and safety.

The world of traditional money management, as we know it, has been turned on its head with zero interest rates and financial repression. Willingly or naively blind to the objectives of central bankers, most investors did not consider the consequences of those measures employed following the 2008 financial crisis and being perpetrated once again today. Ironically, the current fragility of the economy is due in part to past policies and crisis management operations, which, over the longer run, detract from economic growth by discouraging prudent capital allocation and savings.

Fixed Allocation Strategies

Many institutional and retail investment advisors employ strategies that allocate a fixed percentage between stocks and bonds. A 60/40 plan, for example, is when an investor allocates 60% of a portfolio to equities and the remaining 40% to bonds and cash. Generically it is referred to as a “Balanced Portfolio.” Over the past few decades, investors and funds using this type of strategy have been rewarded for their allocation to bonds. There are several reasons for this. First, yields have steadily declined, which has resulted in price gains for those who chose to be opportunistic and take profits. Second, although declining as yields fell, coupon income has also supported returns and helped meet cash flow needs. Lastly, and very important at times, such as today, bonds have historically done well when equities are in a bear market, thus serving as a ballast in the portfolio and hedging equity risk.

With interest rates approaching zero and the stock market now in a bear market, common sense argues that bonds can no longer offer the same risk-reward profile as in the past. To clarify this point, consider the equity hedging benefits of holding bonds during the prior two recessions.

Going back to what we described above as a balanced portfolio, investors benefited greatly during bear markets from the allocation to bonds in a simple 60/40 strategy (S&P/UST). For purposes of simplicity, we assume the full 40% allocation of bonds was in 10-year U.S. Treasuries. In most cases, investors would use other high quality fixed income categories such as mortgages and investment-grade corporates as well as a range of various maturities such as 2-year, 5-year, and 10-years.

The following analysis shows how allocations to bonds helped limit downside in the last two equity bear markets.

-

From September 2007 through March 2009, a simple 60/40 (S&P 500/7-10 Yr. UST) portfolio returned -23.92%. An all-stock portfolio returned -45.76%. The 40% allocation to bonds reduced losses by 21.84%.

-

From January 2000 through September 2002, a simple 60/40 (S&P 500/7-10 Yr. UST) portfolio returned –16.41%. An all-stock portfolio would have returned -42.46%. The 40% allocation to bonds reduced losses by 26.05%.

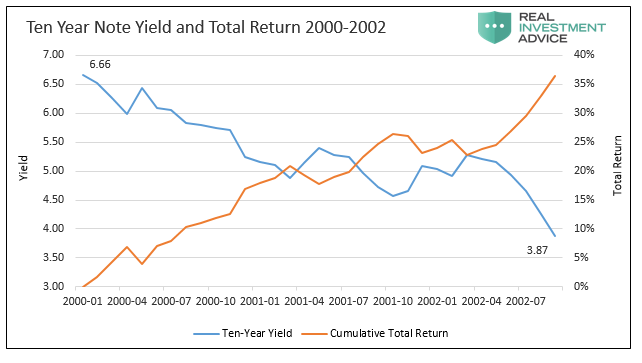

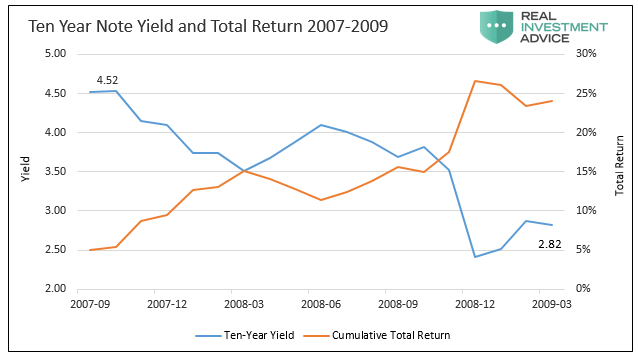

Heading into the two bear markets mentioned above, the 12-month average yield on ten-year U.S. Treasury bonds was 6.66% in 2000 and 4.52% in late 2007. At their lows, the yields fell to 3.87% and 2.43% for 2002 and 2008, respectively.

The graphs below show the decline in the yield for the 10-year Treasury note and the approximate cumulative total return (price and coupon) over the periods mentioned above.

Data Courtesy St. Louis Federal Reserve

Prior bear markets began with interest rates at much higher levels than what we see today. Therefore, well-constructed portfolios containing a healthy share of high-quality fixed-income securities provided sound protection against significant and sometimes permanent losses in a portfolio.

The equity bear market of 2020 is starting with yields well below those seen during the careers of all active portfolio managers. As described above, in the past, holding a ten-year Treasury note yielding 4% or 5% partially hedged equity losses as yield dropped and beneficial price convexity kicked in. With 10-year yields trading below 1%, there is limited room for price appreciation owing to a decline in yields unless one is convinced that yields will move significantly into negative territory.

If we assume the 10-year yield, currently at 0.55%, falls to zero over the next year as the U.S. and world are mired in a post COVID-19 recession, an investor of the 10-year note should expect to receive approximately 0.55% in coupon for the year and an approximate price gain of 5.00%.

5.55% pales in comparison to the 20%+ gains of the prior two recessions.

To hit home on this point, if bonds were to provide 25% protection, as they did in the past, ten-year Treasury yields would need to fall to approximately -2.20%. Given the experiences of Europe and Japan, we cannot rule that out. However, make no mistake; it will require a significant change in the Fed’s perspective on the damage negative yields do to the banking system. Further, we would also need to find a lot of fools willing to pay a remarkably high price.

To the distress of many, the math and probabilities also apply to pension funds, endowments, sovereign wealth funds, and a host of other large investors worldwide. As 10,000 baby boomers retire in the United States every day, all of whom seek secure fixed-income returns, the size of this problem cannot be overstated.

Portfolio Management in an Era of Fools

From an equity perspective, investors will have to be more agile with their allocations. If we are correct in that the bond market does not offer the same loss-mitigating firepower as in past cycles, then investors will be forced to do a better job of understanding valuations and risk.

As we are fond of reminding readers, wealth is best compounded by avoiding large losses. Significant losses are best avoided by not paying too much, or in other words, not being the greater fool. Smart investors and advisors will need to be much more active in choosing the right mix of stocks at the right price and shifting their overall allocations to and from stocks when prudent.

Further, they must also think about the types of companies they own. For instance, in a bear market, value-based strategies are likely to hold up much better than growth strategies. For example, as the tech bubble deflated in the months following March 2000, out-of-favor “old economy” stocks that had gotten so beaten down during the tech euphoria, rallied. Investors may also become more dependent on dividend stocks and preferred stocks to help generate needed cash flows that bonds will not be able to deliver.

The investment industry, like it or not, is about to shift away from the brain-dead investing non-processes of passive and algorithm (black box) trading back toward a thoughtful, value-oriented, common-sense approach to compounding wealth. For more on Process-Based strategies, see our article March Madness: Having a Process for a Winning Outcome.

There are other options than holding equities, which may grow in importance at times. For instance, commodities are currently the cheapest asset class available. In the post-pandemic future, people may permanently modify what they buy and how they buy it. They might also decide to buy less and save more as resources become tangibly more precious. Investors will need to apply their intellect and rigor toward exploring the cause and effect of such changes and what that means for investment opportunities.

While the virus and the possible recession are not immediately good for the economy or commodity prices, we need to be forward-looking. Might rapidly changing supply lines and production cuts lead us to a period when commodities erase long periods of underperformance versus equities like the cheap “old economy” value stocks did in 2000-2002? Given the lack of demand for commodities today, it is hard to envision such performance, but as investors we must look beyond today.

Summary

As bonds flirt with zero or negative interest rates, it will likely be increasingly difficult to find a greater fool in the bond market. Consider also that while you wait to find a fool, you may be paying someone to borrow money from you. Now is the time to think about portfolio management using sound logic and common sense as opposed to blindly chasing tiny interest rates and taking enormous risks.

Balanced strategies and passive management worked well in the past years of financial repression. Still, if rates stay at, near, or even below zero, your portfolio may begin to demonstrate some symptoms of a wealth-devouring virus.

Today is the time contemplate what tomorrow may bring.

Tyler Durden

Thu, 04/23/2020 – 11:10![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com