Here’s 5 Reasons Why Gold Miners Have Massive Outperformance In The Tank

Tyler Durden

Sat, 05/16/2020 – 20:30

Authored by Bryce Coward via Knowledge Leaders Capital blog,

As I write this note on a dreary Friday afternoon from Boulder, CO, I am reminded of my town’s origin. Its first non-native settlers established the town 1858 as a base camp for gold and silver miners. Nestled literally at the foot of the Rockies, its location was ideal for supplying the Colorado mining boom at that time and by 1871 a railroad had been built to connect Denver, Golden, Boulder and the mining operations directly to the West of Boulder. One such mining operation was in what is still known as Gold Hill, which I highly recommend visiting for a live music and BBQ event the next time you are in Colorado (COVID permitting).

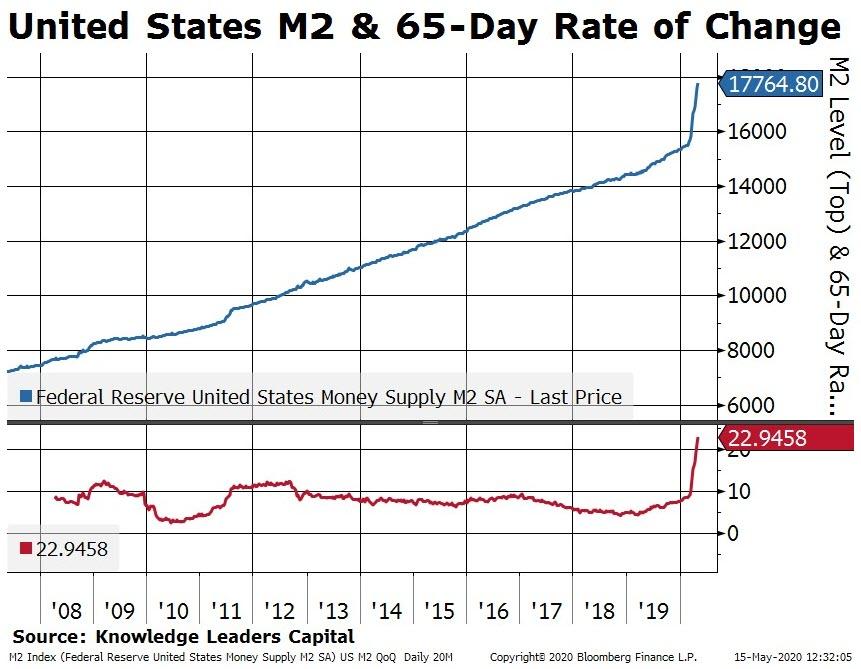

Today we may be in the early days of a different kind of gold boom. This time the boom isn’t because there are new gold reserves to be dug out of the ground. Rather, the steady supply of gold compared to the extraordinary growth of new money requires that the dollar value of the former must rise to keep parity with the latter. Indeed, the US money supply has grown by approximately 23% over the last 65 days, or about a 90% annualized rate.

No wonder the price of gold is sitting near a cycle high of $1743/oz as of this writing. But even as the price of gold has risen in recent months, the gold miners themselves may be even larger beneficiaries of the US dollar supply shock.

Below, we’ll list 5 simple reasons the gold miners could be in for a period of massive outperformance.

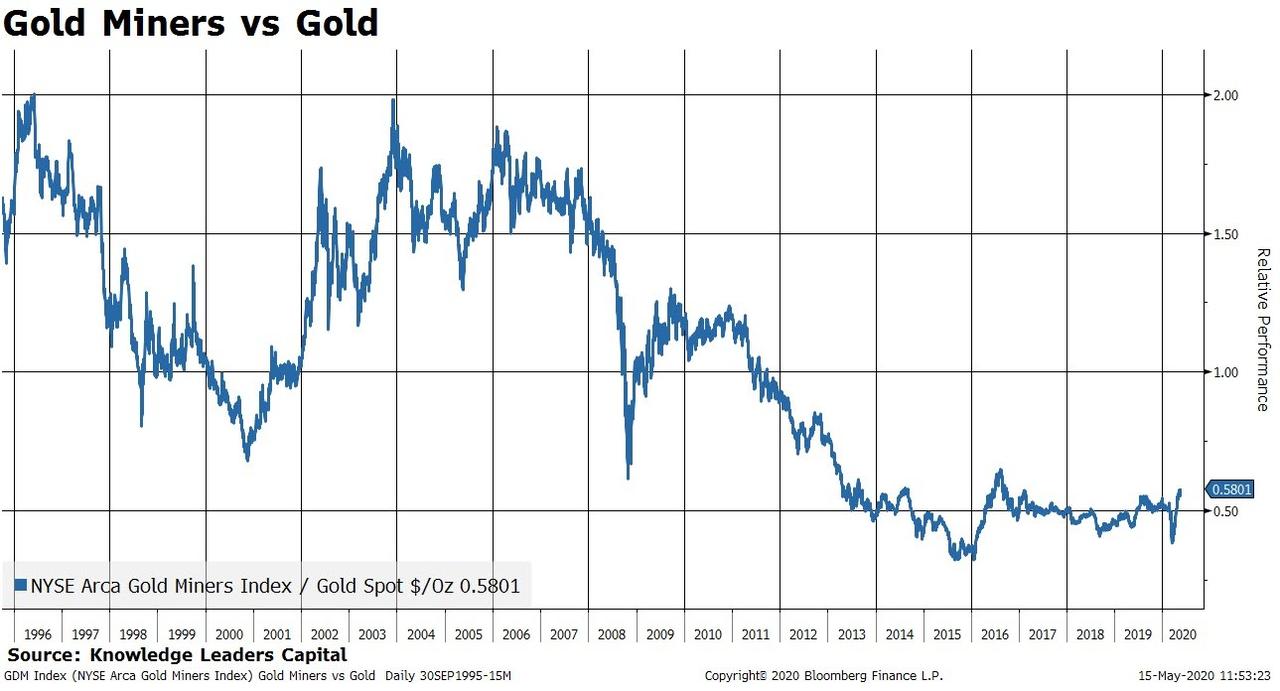

The price of gold miners relative to the price of gold is basically at a 25 year low.

This implies quite a catch up trade if the price of the commodity produced by the miners remains at elevated levels or even rises from here. The price performance of the miners would have to outperform the price of gold by 500% to reach the old 2011 highs in relative performance.

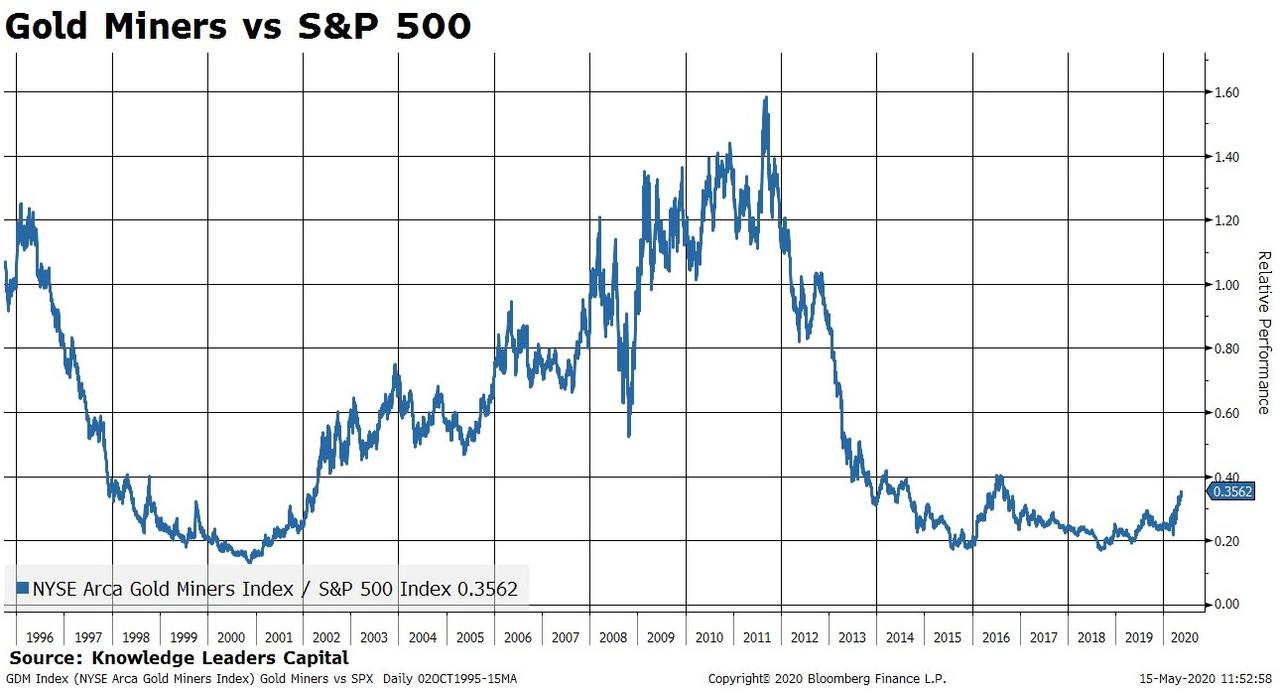

The relative performance of gold miners relative to the S&P 500 remains at near a 25 year low.

Gold miners would have to outperform the S&P 500 by 400% to get back to the 2011 highs in relative performance.

Valuation.

Based on the price to EBITDA ratio (and about all the other valuation ratios), gold miners are cheaper than the overall market. From 2005-2016 gold miners pretty much always traded at a premium to the S&P 500, but now the miners are trading at a 15% discount.

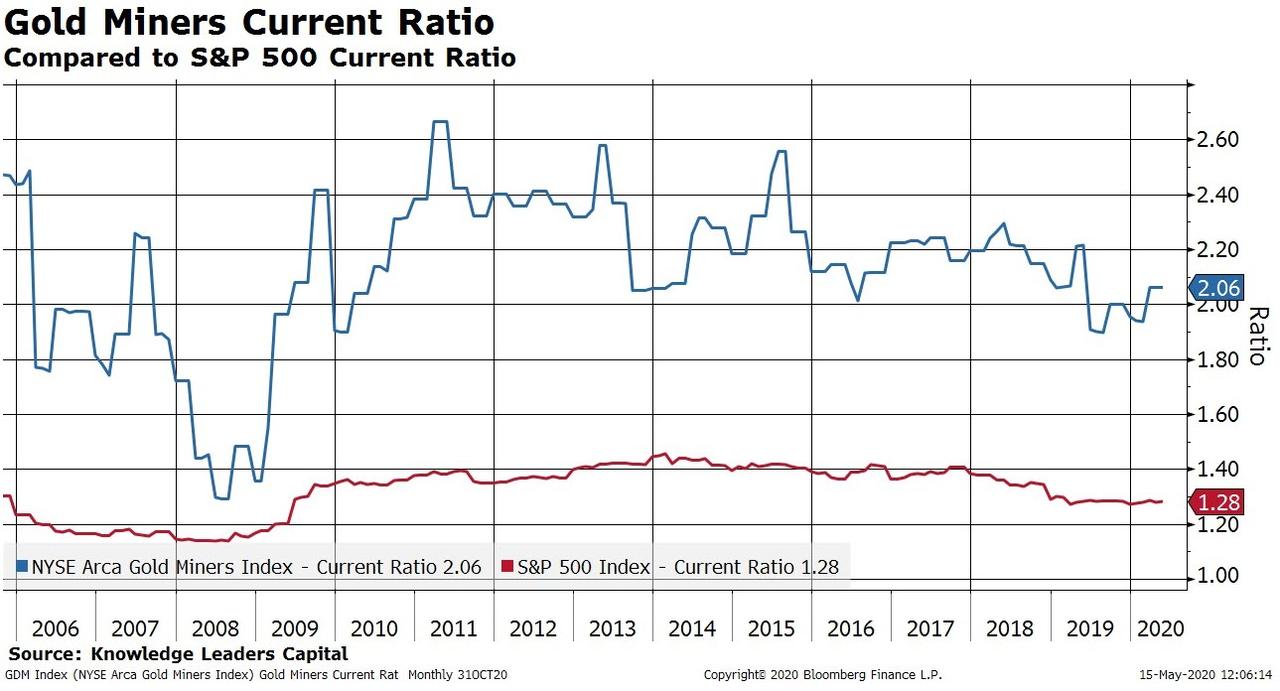

Liquidity.

In the age of COVID, stocks with the ability to service their debt obligations should arguably trade at a premium to the market. The gold miners have a current ratio (current assets/current liabilities) nearly twice that of the S&P 500 as a whioe (2.06 vs 1.28).

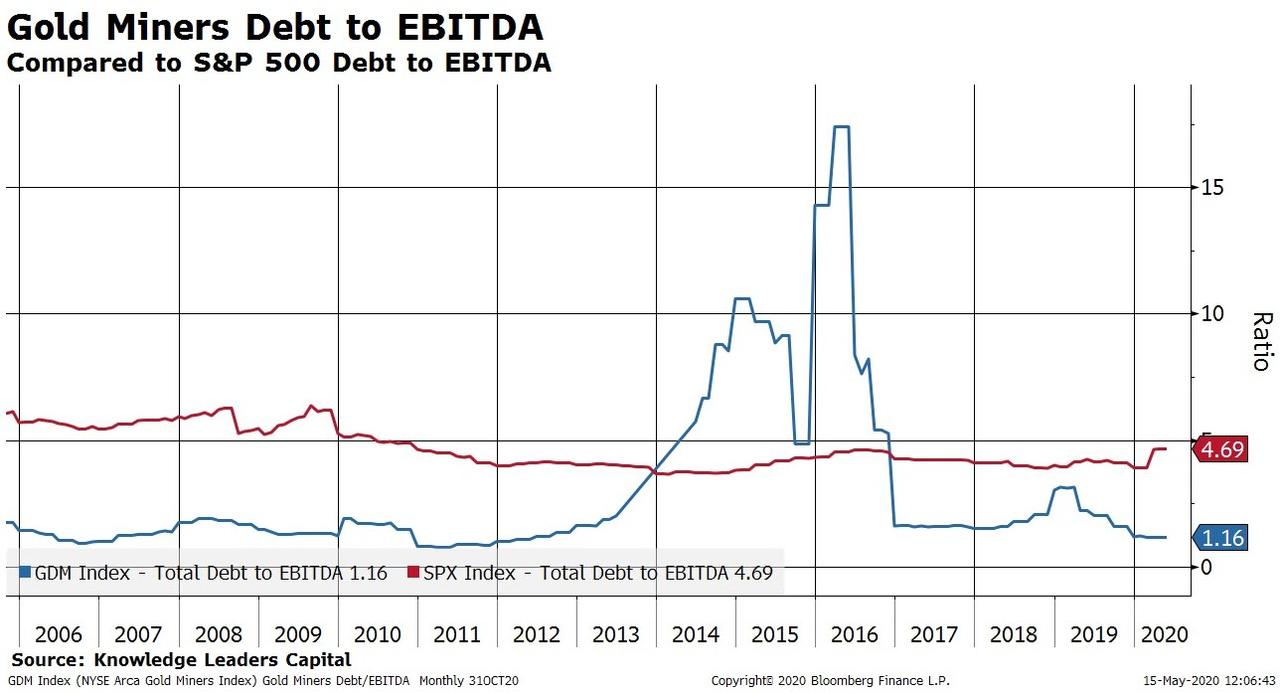

Solvency.

In the age of COVID, stocks with balance sheets in line with their income statements should arguably trade at a premium to the market. The gold miners have debt to EBITDA about 75% lower than the overall market (1.16 vs 4.69).

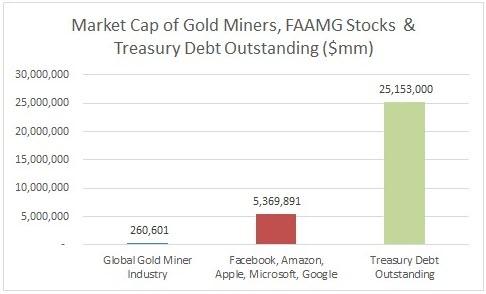

Bonus chart. The global aggregate market value of gold miners is $260bn.

This compares to the aggregate market value of the FAAMG (Facebook, Amazon, Apple, Microsoft, Google) stocks of $5.4tn and the market value of US Treasury debt outstanding of $25tn. So the gold miners, in aggregate, are worth about 5% of the value of just those 5 FAAMG stocks and 1% of the value of all the Treasury debt outstanding.

What do you think would happen to the price of the gold miners if some of that capital left the FAAMGs or Treasury bonds and flowed into the gold miners?

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com