Here Is What Goldman’s Head Of Hedge Fund Sales Thinks Will Happen Next

Tyler Durden

Mon, 06/08/2020 – 18:29

Authored by Tony Pasquariello, global head of HF Sales at Goldman Sachs

amidst a nonfarm payrolls beat for the ages — and, alongside another central bank over-delivering — the stunning rally in risk assets continued this week.

within that context, the undertone of the past few weeks is a pattern of rotation, where the dominant themes which characterized the peak crisis period have shifted, and shifted hard — witness the vicious reversions in value over growth, cyclicals over defensives, RTY over NDX.

to be clear, however, the story of the week wasn’t just one of laggards catching up to winners; it was also a story of a market where most everything rallied (note all 11 S&P sub-sectors were positive, as were 87% of S&P 500 constituents).

and, perhaps tellingly, that superb breadth came on very, very high volume (particularly in NDX, which now sits at a fresh all-time high).

these dynamics were well articulated by sales & trading colleague Pete Callahan: investor focus has shifted to more of a barbell approach as opposed to an either / or approach … secular winners at the high end … plus quality cyclicals (payments, semis and China ADRs) …plus laggards (experience / leisure, value attached to a theme). anecdotally, it feels like the middle bucket — quality cyclicals — is most topical at the moment; thoughts available.

the fundamental driver of the past few weeks traces back to a reopening which — to this point — has been better-than-expected.

in that context, this was perhaps the most interesting thing I saw this week: GS held a conference on the US travel and leisure industry, as represented by 27 different companies; for a macro observer, the overall tone of the conference was noticeably better-than-expected and the companies sounded confident on business acceleration in the re-opening period (link). in retrospect, these anecdotes fit remarkably well with the composition of the payrolls report.

so, for the bulls, the right market metaphor may now be the Swiss Army knife: at any given time, S&P has something going for it … and, recently, most all of the distinct parts were successfully deployed.

for the bears, one can argue that things are set to get tougher in the coming months: as payroll protection drops, as bankruptcies accrue, as the election noise increases, as the “free pass” zone on terrible economic data comes to an end; the bears will argue that it’s not about clearing exceptionally low bars today, it’s ultimately about the terminal direction of the economy.

for the moment, this is still a “rate of change” trading environment where the market is clearly giving the benefit of doubt to the bulls. this take from GIR sums up the short-term fundamental issues very well:

“from a narrow economic standpoint, incoming news has generally been better than expected. most importantly, we have seen little evidence of a widespread pickup in COVID infection rates as Western economies have begun reopening. in Europe, the planned Recovery Fund should go a long way towards shoring up the region’s rickety fiscal architecture. the deterioration in US-China relations remains a major source of concern but, at least over the short term, we expect that both sides will prioritize economic recovery and attempt to avoid a serious escalation. for all of these reasons, we are more confident that the early stages of the reopening process can progress relatively smoothly, and that we will see a substantial rebound in the high-profile economic statistics over the next couple of months. this should provide a further tailwind to the most growth-sensitive assets over the short term, allowing recent trends to extend.”

quick points, charts:

1. I want to circle back to positioning one more time – b/c it has played a large role in recent price action – and, I’ll hazard a guess on the month ahead:

i. the discretionary trading community is decently risked up. exposures are not where they were pre-COVID, but the fact is they have bounced sharply from the lows (link).

ii. the systematic trading community — think CTA / risk parity / vol control — have turned buyer and can certainly increase length from here. in a flat tape, the model suggests around $40bn of global equity buying from CTAs over the next month … with vol control adding a similar amount. to my eye, this is the dominant technical right now.

iii. within the retail cohort, I’d argue there’s a clear demographic divide. the Boomers are selling equity mutual funds and ETFs most every single week … that totals $73bn of YTD outflows. in stark contrast, the younger investor base is very active in single stocks … in many regards, retail traders today are as active as they’ve been at any point since ‘99/’00 (witness GSXURFAV — which, incidentally, now shares 11 names with the pandemic basket, ticker GSXUPAND … also witness exceptionally low put/call ratios).

iv. looking ahead, both the June expiry and quarter end should be on the radar screen:

- – quarterly derivatives expiry is on the 19th. while I doubt that it will bring the same fireworks that we saw on the March expiry, note that open interest to June is very large (nearly $2tr of SPX + SPY OI). as always, you have to respect the power of quarterly expiries … as they can occasionaly mark major inflection points.

- – quarter end will likely bring a slug of equities for sale (given S&P +24% in Q2) … it’s not today’s business, but it’s something to be mindful as we move along and sell side rebalance estimates begin to float around.

my point here: positioning in US equities is very mixed right now. my guess is flow-of-funds are supportive over the next few weeks — largely driven by systematic hands — then technicals will start to shift in the back end of June.

2. as pointed out by sales & trading colleague Brian Friedman, suffice it to say the Fed has largely suppressed interest rate volatility. given enormous policy on one side — but, an unwillingness to go down the negative rates path on the other side — it strikes me that there’s little impetus for front end rates to move big, in either direction. the important part here is not that rate volatility is lower than it was a few months ago — of course it is — it’s the fact that it’s so much lower than the era that preceded it. this week’s yield backup notwithstanding, perhaps in the next phase of the cycle this ups the ante for money to be made elsewhere — FX, equities, credit, EM and commodities. along the way, I suppose this framework also argues for steepeners.

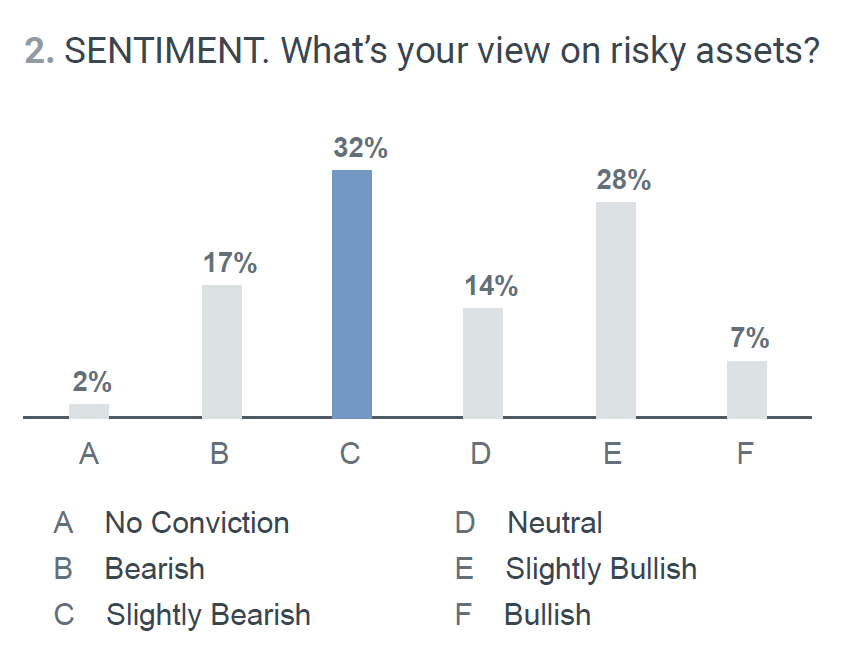

3. if I had to sum it up in a line: risk sentiment is considerably less bearish than it was just one month ago, but it’s hard to find many genuine bulls within the professional trading community. as you can see here in the latest GS Quick Poll data (link), sentiment on risk assets is better balanced today as compared to months, but it’s by no means extended (and the distribution suggests few people believe in tail outcomes, where I’m still inclined to be open-minded, particularly on the laggards; more available):

4. through all the volatility of recent months, I find it notable that investor focus on the ESG theme has remained intact, if not accelerated (link). this is evident in both the performance of the ESG factor and actual fund flow. this is worth underlining: ESG fund flows represent 31% of all global fund flows YTD (link). here’s one implementation that I like structurally: GSXURNEW is a basket of 31 US companies that stand to benefit from a transition to cleaner energy. this is the basket vs S&P:

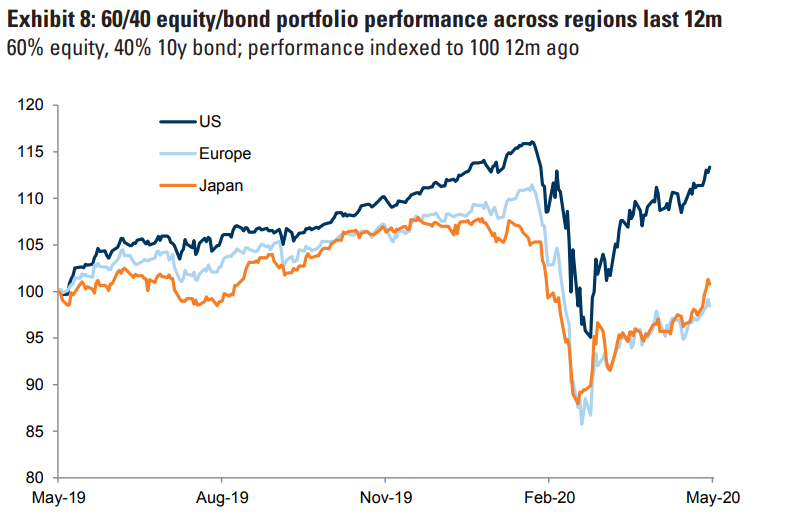

5. perhaps rightly, there’s an open question right now on the dominance of US assets on a go-forward basis. well, as the old Dreyfus ads used to say: past performance is no indication of future results … but, it is something to consider (link):

6. to the point up top on the US travel and leisure industry, this survey of 27 corporates was notably positive (link). importantly, as pointed out to me by sales & trading colleague Scott Feiler, this comes from a starting point of deep bearishness and skepticism. many assume these data points are just stimulus-driven or pent-up demand off an extremely low base; the surprise would be if these consumer trends prove to be more durable than just the initial bounce:

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com