The Next Iteration. What Is Yield Curve Control?

Tyler Durden

Wed, 06/17/2020 – 12:12

Authored by Michael Lebowitz and Jack Scott via RealInvestmentAdvice.com,

The next iteration of monetary policy may well be “yield curve” control?

Debt and interest rates have become the predominant driving force of our economy. Unfortunately, a majority of the debt is unproductive, resulting in declining long-run economic and productivity growth rates.

In the 1950s, each dollar of debt drove nearly 70 cents of economic growth. It has fallen ever since. Recently, each dollar of debt bought less than 30 cents of growth. That number has deteriorated further in the last few months.

The Fed, as manager of monetary policy, can use policy to either encourage long term prosperity or shorter-term economic activity. They have chosen the latter and, as a result, have dug themselves into quite a hole. Each dollar of debt drives less growth than the prior dollar of debt, thus requiring even more debt.

This article explores Yield Curve Control (YCC), a policy tool at the Fed’s disposal to keep digging even deeper into the hole.

The Hole

Government and corporate debt levels are currently increasing at unprecedented rates. Total non-financial debt rose nearly 12% in the first quarter. The amount will surely be much higher when second-quarter data is released.

The federal deficit in the current fiscal year is expected to top $4 trillion. To put that in context, it took 192 years between 1789 and 1981, for America to amass its first $1 trillion of debt.

Only halfway through the year, corporations exceeded $1 trillion of issuance, putting them on par with annual totals from the prior few years.

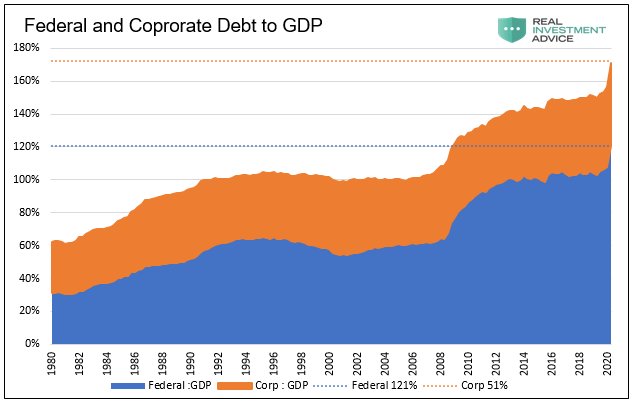

The graph below shows the ratio of non-financial corporate debt and federal debt to GDP. They both sit at record levels and will rise rapidly when second-quarter GDP is released.

As the ratio of debt to GDP increases, even more debt is needed tomorrow just to maintain current economic activity. For a Fed overly concerned about short-term economic activity, this dilemma creates a self-reinforcing problem. The situation is akin to a Ponzi scheme that needs constant feeding.

Given the Fed’s desire to avoid the slightest economic setback, surging debt levels means the Fed will have to become even more creative and active in managing interest rates. Are they prepared to impose negative interest rates on U.S. society? Although that tactic has been remarkably unproductive in Europe and Japan, the Fed has not formally ruled out negative rates.

Keep Digging

Fed Funds are at zero, and the Fed has not committed to negative interest rates. What else can the Fed do to keep debt flowing?

The Fed sets short term rates but can only indirectly influence long-term rates. Longer-term rates spanning from two-year maturities out to thirty years drive borrowing and consumption.

Quantitative Easing (QE) was introduced in 2008 when the Fed Funds rate hit zero. QE allows the Fed to purchase bonds in an effort to lower interest rates for longer-term maturities. During QE 1, 2, and 3, they bought Treasuries, mortgages, and agency bonds. Despite what one would think, on each occasion, longer-term rates rose. In the last month, they expanded their reach to include large-scale purchases of municipal bonds, corporate debt, and even junk-rated corporate bonds and ETFs.

Steering rates and setting rates are not the same. The question for the Fed is, how can they control interest rates for longer-term securities?

Yield Curve Control – A Bigger Shovel

QE 1, 2, and 3 ran systematically. The Fed set a predetermined amount and timing of QE in which to operate. It was useful in reducing the supply of Treasuries available and forcing investors into riskier assets like junk bonds and stocks. However, it did not allow the Fed to explicitly control the level of interest rates.

The Fed is now considering an enhancement to the way it manages QE. The “upgrade” is called yield curve control (YCC). YCC essentially allows the Fed to do unlimited amounts of QE with no time restraints. Embedded in YCC is the specific goal of targeting particular interest rates across the entire yield curve.

For example, assume the Fed set a 0.75% target yield on the 10-year U.S. Treasury note. They can then employ QE in any amount needed to buy 10-year notes when the rate exceeds that level. If successful, the rate would never exceed 0.75% as traders would learn not to fight the Fed.

It is essential to be clear about the definition of YCC. The Fed represents it as an option for helping them manage the economy through the difficulties the country currently faces. However, YCC is a euphemism for price controls. Price controls are government interference and regulation, establishing prices for specified goods and services.

In this instance, we are talking about the most fundamental component of any economic system, the price of money. Historically, in every case, the implications of price controls have been unfortunate.

Two examples of price controls leap out from recent history:

-

Those imposed on gasoline during the Arab oil embargo in 1973 and 1974 that created long lines of cars waiting to fill up at gas stations

-

Those set on electricity in the state of California, which contributed to rolling blackouts

Managing the Yield Curve

It is called yield curve control because the central bank effectively manages the shape of the yield curve. A steeper yield curve benefits the banks as they tend to borrow short term and lend long term. Larger profit margins increase their desire to lend and therefore stimulate debt-driven economic activity. Conversely, a flatter or inverted yield curve inhibits lending due to narrower bank profit margins, and consequently, it curtails debt issuance and economic activity.

The problem for the Fed is how they can steepen the yield curve to stimulate lending without letting longer-term rates rise too much? Under YCC, they may squirm out of one trap only to find themselves in a bigger trap.

History

The Fed would not break new ground with YCC. In fact, they would be reinitiating a previously used tactic. From 1942 to 1950, the Fed targeted rates to help manage funding costs for WWII. If you are interested in reading more on the U.S. experience with YCC, we suggest the following article from the Federal Reserve: How the Fed Managed the Treasury Yield Curve in the 1940s.

It is worth pointing out that after WWII ended, inflation spiked to double digits, yet the Fed held interest rates at artificially low levels. While bondholders may not have lost money on the bonds per se, they did lose dearly in their purchasing power, as shown below.

More recently, in 2016, Japan set a 0% yield target on its ten-year note. Currently, the bank of Australia is now targeting 0.25% for its three-year bond.

Summary

Federal Reserve Bank of New York President John Williams says that policymakers are “thinking very hard” about targeting specific yields on Treasury securities. Given what we have observed, it seems likely they will implement YCC and, in doing so, choose to keep digging and try to push problems out further into the future.

The problem with these actions is they engender anemic rates of economic growth. Equally concerning, they directly contribute to income inequality, a driving force for social unrest.

The policies the Fed staunchly defends are adverse to the healthy economic and social environment the country so desperately needs. While in crisis mode, investors will cheer them on unaware of the adverse effects it will have on the economy. As they say, there is no such thing as a free lunch.

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com