Morgan Stanley Gets Even More Bullish Because Mass Layoffs Mean Even Higher Profits

Tyler Durden

Sun, 07/05/2020 – 15:30

Authored by Michael Wilson, chief equity strategist at Morgan Stanley

Don’t Overlook Operating Leverage

2020 has been an unusual year. It started with record-low unemployment and equity markets making new all-time highs nearly every day. In January and February, it was hard to find anyone who was negative on the economy or the stock market. All that changed in March when the novel coronavirus turned into a fully fledged global pandemic. The subsequent lockdown of the US economy led to the most sudden and severe recession in history, and the stock market crashed.

What followed was the greatest monetary and fiscal stimulus ever enacted. This means we’re likely to experience one of sharpest recoveries on record. Stock markets around the world seem to agree, with most major averages trading extremely well. This rally has many people concerned that equity markets are disconnected from the fundamentals and do not reflect the risks that still loom. But equity markets move well ahead of the economy and are often the best leading indicator. In short, we think that the V-shaped recovery in markets foreshadows a V-shaped recovery in the economy and earnings.

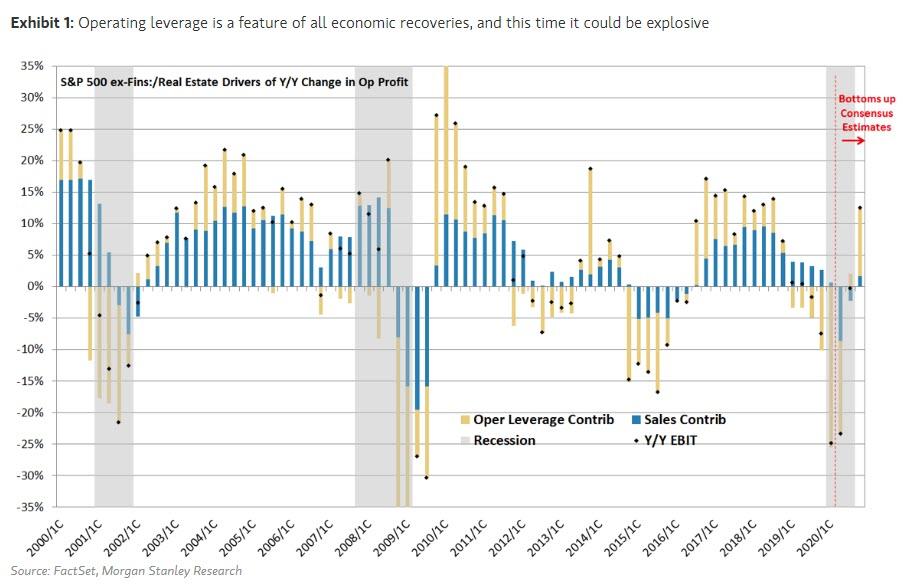

Cautious investors may be overlooking the potential for operating leverage to fuel an earnings rebound. Aggressive cost-cutting in a downturn is what creates the powerful operating leverage when the economy recovers (Exhibit 1). Labor is the number one cost for most companies, and the distinguishing feature of any recession is a sharp rise in unemployment. This time, unemployment went from a record low of 3.5% to almost 15% in just two months. Typically, it takes 1-2 years for the unemployment rate to reach its cycle peak. What’s more, this increase in unemployment was twice the normal size, which should leave cost structures leaner than usual coming out of the recession.

Operating leverage thus could be particularly explosive this time as the economy, and sales, recover. From an investment perspective, this means that earnings for many companies and the overall index will return to prior highs much faster than most analysts are forecasting. Therefore, stocks can continue to move higher even as peak valuations decline, especially the more economically sensitive cohorts and small caps. These are all features of any economic recovery and could be magnified this time by the depth of the decline and the high levels of unemployment that are likely to persist into next year. While bottom-up consensus already forecasts a significant recovery in earnings growth next year, it may still be underestimating the upside.

I would also note that operating leverage moved into negative territory starting last year. Regular readers of our research are aware of this, as negative operating leverage was key to our earnings recession call. It’s also a classic feature of late-cycle economic expansions. My point is that many companies were already exhibiting negative operating leverage pre-COVID-19. This gives me confidence that 2Q will likely be the trough for earnings growth. It also suggests that the companies with the most negative operating leverage are likely to exhibit the most upside to earnings expectations over the next year. This conclusion anchors our call to favor cyclicals and small caps.

Of course, there are risks to our positive earnings story, ranging from an uncontrollable second wave of the virus to an election outcome viewed as less market-friendly. However, the biggest and most notable risk in our view is that the fiscal stimulus package extension currently being debated in Congress falls short. There’s little doubt that the nascent recovery, while looking better than expected so far, still needs support to reach a self-sustaining trajectory. We remain optimistic that Congress will deliver in an election year, but it may take a market wobble this month to get the package over the goal line.

Finally, from our analysis of investor positioning and conversations with clients, we view institutional investor sentiment as neutral at best, while retail investors remain outright cautious [ZH: yeah… not so sure about that]. We think this mood reflects the fact that we are still in the midst of both a health crisis and a contentious election cycle. We also view this ‘disbelief’ as normal at the beginning of a new economic cycle and bull market, creating a healthy wall of worry that has yet to be scaled.

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com