Shaping Eurasia: Russia – China Bilateral Trade And Cooperation

Tyler Durden

Mon, 08/03/2020 – 22:45

Submitted by SouthFront

Relations between Russia and China have gone from strength to strength over the last 10 years. This development is not exclusively due to the increasingly hostile attitude of Western countries, and the US in particularly, to Russia and China, but it has certainly been a major contributing factor. The deepening and diversification of their strategic relationship is apparent in all spheres, but is particularly notable in their economic and military relations.

There are many factors underpinning the expansion and diversification of trade relations and other forms of economic cooperation between Russia and China. The most important ones include the imposition of sanctions on Russia by Western countries in 2014, the economic stagnation that has characterized most European countries for much of the last 10 years while the Chinese economy has continued to grow, symmetry in economic characteristics of both countries (surpluses in one and corresponding shortages in the other in a variety of sectors), US pressure bringing both countries closer together geo-strategically (which has also produced a mutual interest in shifting away from the US dollar in all transactions), and the consolidation and harmonization of the Chinese ‘One Road One Belt’ initiative and the Eurasian Economic Union

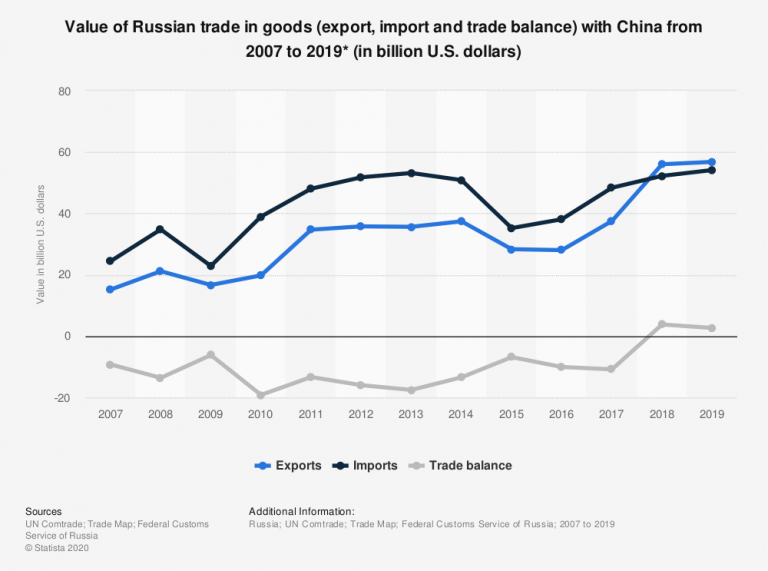

After a relatively flat period marked by what could be characterized as benign indifference and neglect, the trade relationship between Russia and China has grown rapidly since 2009 in terms of both imports and exports, although there was a sharp decline during 2014-2015 corresponding to a sharp decline in Russia’s overall GDP and trade volumes.

However, at least as importantly, the growth in trade and other forms of economic cooperation has not just been quantitative but also qualitative, as the governments of both countries have elaborated detailed industrial development strategies and plans over long periods which have channelled both public and private sector investment and production into priority areas.

This is in sharp contrast to the peculiar form of haphazard, opportunistic and hyper-militarized disaster capitalism that has reigned in the US for many years – arguably at least since the 1990s, when US companies began dismantling the US industrial capacity and offshoring production en masse to raise corporate profits, and the US Congress began to dismantle the anti-trust and financial regulatory frameworks that had been established during the Great Depression of the 1930s to limit the volatility and excesses of the financial sector. (It is also approximately the same period that the US began its post Cold War military adventurism in earnest.)

Most recently the Trump administration’s ambitious infrastructure investment fund (which appeared to be yet another corporate and political slush fund to a considerable extent, to be divided amongst political and corporate allies and withheld from opponents or intransigents) to modernize the US’ aging infrastructure never materialized, and the attempt to establish something resembling a coherent industrial policy complemented by a set of tariffs on selected imports to stimulate domestic production degenerated into an ad hoc series of punitive tariffs and charges whose main objective seemed to be to punish China for the US’ own economic and industrial failures.

The only thing the Republicans and Democrats have been able to agree on in recent times, apart from increasing the already astronomical level of military spending, was to establish another disaster capitalism multi-trillion dollar bailout fund (for the Coronavirus this time) for the financial and corporate sectors, which have increasingly fallen under the control of a very limited number of investment funds led by Vanguard and Black Rock.

In contrast, China’s long-running practice of elaborating and updating five year strategic economic development plans which are implemented by a combination of State-owned and private sector enterprises has proven to be a success. After a catastrophic period of experimentation with disaster capitalism under Boris Yeltsin, Russia has also adopted the strategy of developing a hybrid (or ‘mixed’) economy with substantial State and private sector involvement within the overall framework of strategic planning and industrial policies elaborated by the State in accordance with crucial national interests and objectives.

The underlying similarity in approaches and objectives – albeit obscured somewhat by China’s continued strong commitment to communism and Russia’s strong renunciation of the same – has provided a solid basis for both countries’ renewed interest in strengthening bilateral relations and cooperation in all spheres.

While the leadership of both countries have sought to develop and promote a wide range of bilateral trade, investment and R & D projects both by State entities as well as by the private sector, due to their vast scale the bilateral agreements and projects in the energy sector overshadow all others.

This should not however obscure the importance of cooperation in other sectors and the extent to which the different manifestations and forms of cooperation have continued to proliferate. Most Western analysts emphasize the excellent ties that have developed in terms of military cooperation, involving everything from basic R & D of new technologies and weapons systems to military training and exercises, but the bilateral cooperation goes far beyond these high profile sectors to include education, scientific and technical research, agriculture, manufacturing and services more generally.

Macroeconomic Data on the Russian Economy

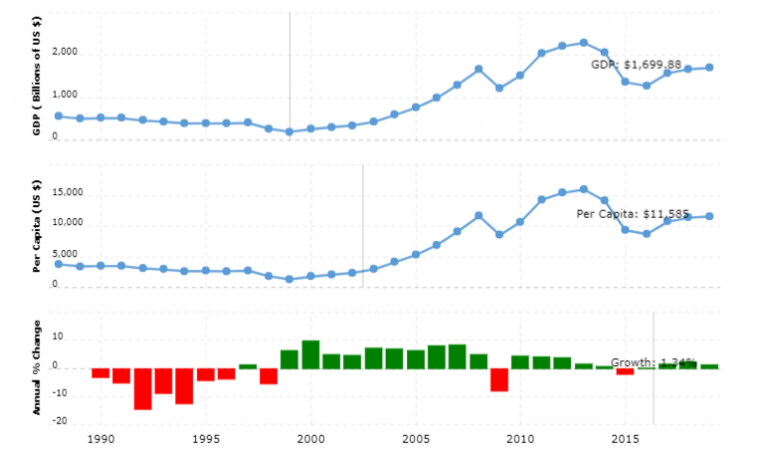

To contextualize the changes that have taken place in the bilateral economic relations between Russia and China, they are placed against the background of economic developments in Russia more generally. As noted above, Russia’s economy has generally experienced solid if not spectacular growth since the disastrous decade of the 1990s, and although it was significantly impacted by the West’s sanctions imposed in 2014 (as well as by the fall in oil prices that ocurred around the same time) the economy soon stabilized and then recovered quantitative losses on an even more solid fundamental basis given the economy’s increased diversification, self-sufficiency and resistance to external shocks.

{kind=link}

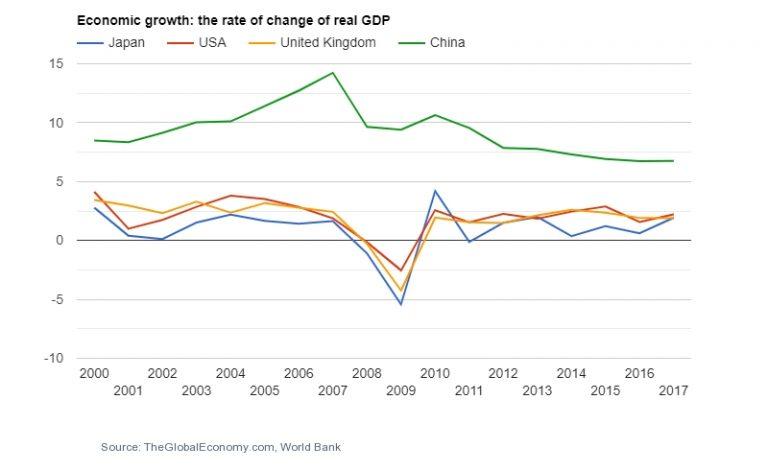

Overall Russia has performed at least as well as most Western countries since 2000, though of course China’s economic growth has far exceeded them.

China’s impressive economic growth therefore could explain the steady trend of increasing trade between the two neighbours by and of itself, however as mentioned above bilateral relations have been boosted by external factors (Western hostility and sanctions) and also nurtured and guided by internal factors (strategic economic and industrial planning based on compatible national priorities and objectives, augmented by significant levels of direct State participation in key economic sectors).

{kind=link}

Imports and Exports

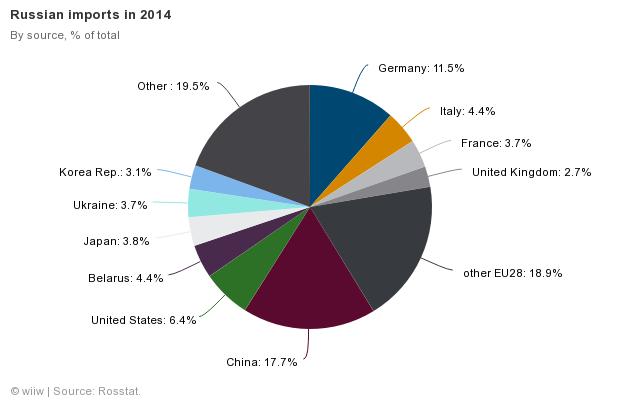

The growing economic importance of China to Russia has largely been at the expense of Europe, in part due to the imposition of sanctions against Russia but also a natural consequence of China’s continued economic growth and Europe’s economic stagnation, as well as the complementarity that exists between the Russian and Chinese economies, sectors of comparative advantage and resource endowments.

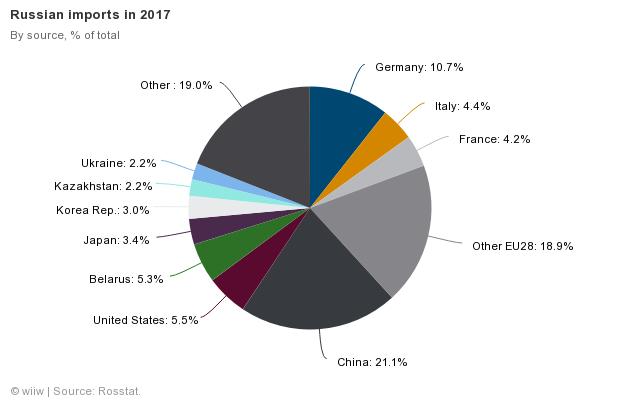

The share of the 28 European Union countries in Russian exports dropped from 52% in 2014 to 45% in 2017, and the corresponding shares in Russian imports fell from 41% to 38%. Over the same period, the share of China in Russian exports increased from 7.5% to 12%, and in imports from 11.5% to 21%. Nonetheless, as of 2017 Russian imports from China (EUR 48bn) remained about half the value of imports from the European Union (EUR 87bn). Thus although trade reorientation away from the West and towards China is steadily increasing, Europe remains an integral trade partner for Russia.

The figures for 2019 were very similar. The top 10 sources of imports were:

China 21% (54 billion US$), Germany 10.1% (25 billion US$), Belarus 5.52% (13.6 billion US$), USA 5.43% (13.4 billion US$), Italy 4.41% (10.9 billion US$), Japan 3.62% (8.96 billion US$), France 3.47% (8.59 billion US$), Korea 3.23% (8 billion US$), Kazakhstan 2.31% (5.71 billion US$), Turkey 2.01% (4.97 billion US$).

The top 10 export destinations for Russian exports in 2019 were:

China 13.4% (57 billion US$), Netherlands 10.4% (44 billion US$), Germany 6.57% (28 billion US$), Belarus 5.08% (21 billion US$), Turkey 4.95% (21 billion US$), Korea 3.83% (16.3 billion US$), Italy 3.36% (14.3 billion US$), Kazakhstan 3.34% (14.2 billion US$), United Kingdom 3.11% (13.2 billion US$), USA 3.09% (13.1 billion US$). Source

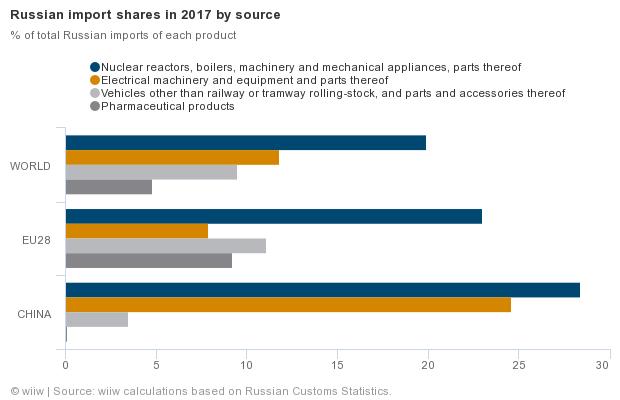

The continued importance of Europe to Russia’s economy is particularly evident when the analysis goes beyond the level of trade volumes, to a consideration of the evolution of trade structures by sector, particularly in the case of Russia’s imports. Whereas Russian exports are dominated by mineral fuels in both directions (accounting for more than 76% of exports to the EU and 64% of exports to China), there are important differences in the structure of Russian imports from the EU and China.

“This reflects the fact that, in certain areas, Russia still needs products and equipment that it can only obtain from Western sources. For example, whereas the HS84 category (nuclear reactors, boilers, machinery and mechanical equipment) represents the largest import item from both the EU and China (with shares in total Russian imports of 23% and 28% in 2017, respectively), the second and third most important categories of imports from the EU: HS87 (vehicles, 11% of Russian imports) and HS30 (pharmaceuticals, 9%) are still largely absent in imports from China…

Nevertheless, import structures are also converging: between 2014 and 2017 these structural ‘import gaps’ were substantially reduced – most spectacularly in the above mentioned three largest import items. The structure of Russian imports from China is also becoming more sophisticated: the shares of machinery and electrical equipment are already higher than the corresponding shares in imports from the EU. As the EU-China import gap closes for Russia, one can conclude that China is gradually replacing the EU as an import source, even with respect to structural developments (although there remain gaps at more detailed commodity levels).” LINK

Key Sectors and Major Projects

The negotiation and execution of structural agreements and operational projects and transactions has taken place within the framework of existing strategic planning elements so as to maximize their compatibility with existing projects and activities and contribution to the realization of national priorities and interests. Although Russia’s efforts to increase economic diversification and self-sufficiency in key sectors received a great boost from the imposition of sanctions in 2014, it had already taken substantial steps in this regard. For instance, a ‘food security doctrine’ has been official government policy since 2010, and the doctrine has been a key element of subsequent government programs for the development of the agriculture and fisheries sectors and the regulation of agri-food markets during the period 2013-2020. LINK

In the same way, ambitious infrastructure projects announced in the framework of developing bilateral relations – such as the Moscow-Kazan high speed railway, which will eventually be part of a high speed rail network linking China (and probably even southeast Asia) to Europe – are being laid out within the framework of a broader Russian strategy to overhaul and upgrade infrastructure throughout the country. In April 2019 the Moscow Times reported:

“The Russian government is pursuing a 6.3 trillion ruble ($96 billion) six-year modernization plan to revamp the country’s highways, airports, railways, ports and other transport infrastructure through 2024.

The comprehensive plan is geared toward improving the connectivity of Russian regions, as well as developing strategic routes including the Europe-Western China transport corridor and the Northern Sea Route.

The plan stems from President Vladimir Putin’s ambitious domestic goals outlined after his inauguration last May. Under a presidential decree, a 3.5 trillion ruble investment fund was set up last summer to finance around 170 construction and other projects from 2019 to 2024.”

Of course, both the general plan and specific details have been subject to scepticism by some experts:

“Bloomberg columnist Leonid Bershidsky has argued that the infrastructure plan risks neglecting underdeveloped regions the Kremlin sees as a “social liability.” Economists interviewed by The Christian Science Monitor have said the revitalization plans are geared toward boosting the export potential of big business and are ill-equipped toward future economic development.” LINK

Nonetheless, at least Russia is committed to thinking and acting strategically with the intention of improving the country’s stock of assets and capabilities, and early indications are that most of the projects have been thoroughly evaluated for current and future economic and social utility and that implementation is progressing steadily. What would the detractors of Russia’s efforts in this respect make of the non-existent efforts of the ruling classes in the US to undertake a similar national infrastructure modernization project?

Early on in the preparations for a massive expansion in bilateral ties the underlying financial infrastructure was laid.

Although still heavily reliant on the US dollar for all bilateral transactions at the time, by 2014 around 100 Russian commercial banks were already offering corresponding accounts for settlements in yuan, and in some ordinary depositors could also open an account in yuan. On November 18 Sberbank became the first Russian bank to begin financing letters of credit in Chinese yuan.

The settlement in national currencies between China and Russia in bilateral trade amounted to about 2% in 2013. However, the use of the yuan in mutual settlements between China and Russia increased ninefold in annual terms between January and September 2014, according to the Chinese Ministry of Economic Development, and has continued to rise. LINK

The financial basis for greatly expanded relations has continued to evolve in accordance with progress in other areas.

Thus, in 2015 Sberbank – Russia’s biggest lender – signed a facility agreement with China’s Development Bank to the amount of $966 million.

The goal of the agreement is to develop the “long-term cooperation between Sberbank and China Development Bank in the area of financing foreign trade operations between Russia and China.”

Russia’s state-owned VTB Bank and the Export-Import Bank of China also signed a $483.2 million loan facility agreement to finance trading operations between Russia and China.

The financial architecture has been further consolidated by broader regional frameworks and agreements for mutually beneficial cooperation.

In 2015, Russian President Vladimir Putin and Chinese leader Xi Jinping signed a decree to formalize cooperation in linking the development of the Eurasian Economic Union with the “Silk Road” economic project. The Silk Road project is aimed at connecting China with European and Middle Eastern markets.

“The integration of the Eurasian Economic Union and Silk Road projects means reaching a new level of partnership and actually implies a common economic space on the continent,” Putin said after the meeting with his Chinese counterpart.

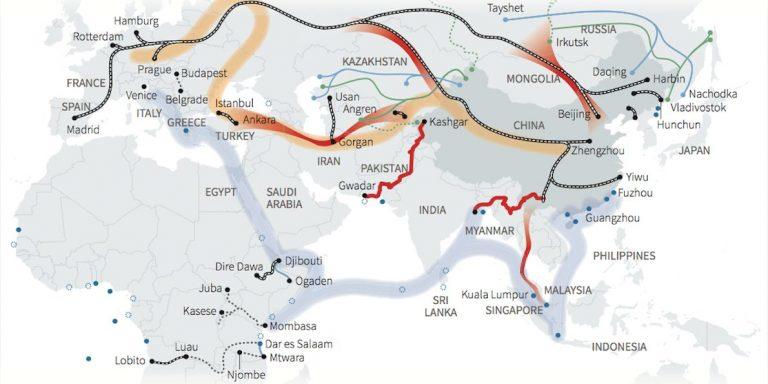

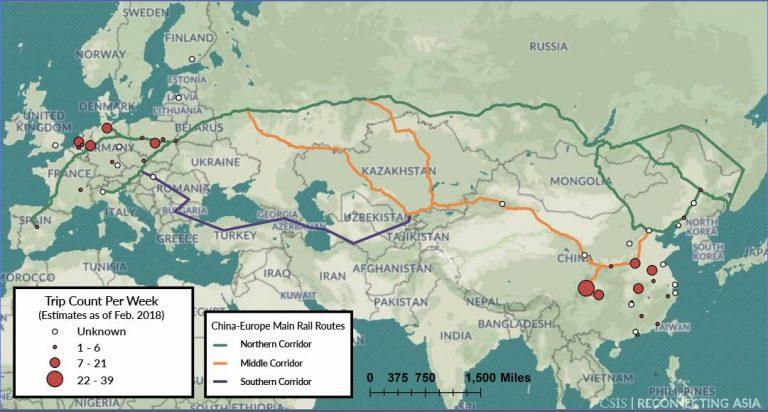

Major transport corridors of the Chinese Belt and Road Initiative

Trans-continental railways

Russia’s railway network is steadily undergoing a major program of extension and modernization

Also in 2015, China pledged to invest $5.8 billion in the construction of the Moscow-Kazan High Speed Railway. The railway will be extended to China, connecting the two countries through Kazakhstan. The total cost of the Moscow-Kazan high speed railroad project is $21.4 billion.

An agreement was signed to create a leasing company which will promote the sale of the Russian Sukhoi Superjet-100 passenger planes to the Chinese and South-East Asian markets, and the two countries agreed to develop a new heavy helicopter, called the Advanced Heavy Lift. LINK

The broadening of economic relations spearheaded by high profile State-led industrial projects is underpinned by a range of other initiatives. For example, in September 2018 Russian and Chinese businesses agreed to further develop trade and economic cooperation and increase mutual investments at the Eastern Economic Forum in Vladivostok.

According to a statement from the Russian Direct Investment Fund (RDIF), the sides are considering 73 investment projects worth more than $100 billion in total. The group overseeing the investments is the Russian-Chinese Business Advisory Committee, which includes more than 150 representatives from “leading Russian and Chinese companies.” RDIF said that seven projects worth a total of $4.6 billion have already been implemented as a result of the group’s activities.

The Russia-China Investment Fund was established in 2012 by China’s state-owned China Investment Corporation and RDIF to focus on projects that foster economic cooperation between Moscow and Beijing. LINK

Major China – Russia gas routes

The largest joint project that has been developed is the massive Power of Siberia gas project. In 2014 Gazprom and the China National Petroleum Corporation (CNPC) signed a $400 billion, 30-year framework agreement to deliver 38 billion cubic meters of Russian gas to China annually. According to Russian energy major Gazprom, 119 operational gas wells had been completed by 2017 at the Chayandinskoye field in Yakutia, and the 3,000km of pipelines from Yakutia to the Russian-Chinese border, connected to the Chinese grid via a two-thread underwater crossing of the pipeline across the Amur River, started deliveries as scheduled late in 2019. The deal on the ‘Eastern Route’ took more than a decade to negotiate.

While Western experts are trying to downplay the merits and prospects for the Power of Siberia project – and the bilateral strategic relationship more generally – the project started supplying gas on schedule and at this stage it appears that the claims of the detractors consist of logistical and operational challenges that the Russians have ample experience in confronting or are largely wishful thinking (the terrain is very inhospitable and operating costs and risks are therefore very high, the project will crowd out smaller producers, Russia is locking itself into an arrangement that eliminates other opportunities, Chinese market power means Russia will have to accept unfavourable conditions, the Asian giant will inevitably swallow up its northern neighbour, bilateral relations are founded on a ‘marriage of convenience’, etc.). LINK

As the US has continued to intensify its hostility and associated geopolitical and economic pressure on China and Russia, the two countries have continued to expand their military cooperation as well as a strong high-tech partnership spanning telecommunications, artificial intelligence and robotics, biotechnology and the digital economy based on the exploitation of existing and potential synergies.

The deepening of the bilateral relationship includes more dialogue and exchanges of information, increased academic cooperation and the development of joint industrial science and technology parks. In addition, Russian President Vladimir Putin said Russia would help the Chinese build their own missile early-warning system – a technology that only Russia and the U.S. have successfully implemented so far. LINK

Conclusion

The crucial role of strategic economic and industrial planning and direct State participation in key sectors has been emphasized throughout this report. This is not to suggest that such planning and participation has been perfect; of course, significant errors have been made in both planning and execution, unforeseeable external shocks or factors that could have been predicted but were not taken into account have disrupted progress, as in all other countries.

One area of particular concern is the adverse material impact and effect on morale caused by corruption, which continues to plague both State and private sectors suggesting that the systems of accounting and accountability applying to both require further improvement in both design and implementation. Also, it is arguable that the vision of public forms of economic ownership and participation remains somewhat limited to a strict State/ private company dichotomy and to elitist management structures and procedures within each.

One aspect of this is that more forms of State participation could be considered at the regional and local levels; another is in terms of inclusion of the workforce of each enterprise in the planning, management and accountability structures and decisions of existing State-owned enterprises.

Beyond this, there may be scope for the promotion of other forms of organization, such as producer, professional or community-based cooperatives and collectives that can provide an organizational basis for economic projects and activities in a manner that can incorporate other values and objectives beyond the profit motive.

The basic data for foreign capital flows also suggest a major structural defect which is inherent to the ‘actual existing’ international economy: a vastly disproportionate amount of capital arrives from and departs for small countries that have no clear trade significance or investment capacity of their own, meaning that such capital flows are routed via these jurisdictions either to avoid taxes and other regulations or to deliberately obscure the identity of the owners and beneficiaries of the resources involved.

According to UNCTAD, between 30% and 50% of all ‘foreign direct investment’ worldwide passes through “conduit” countries, making it hard to determine the source.

According to data from the Central Bank of Russia for 2017, Russia receives 36.8% of ‘foreign direct investment’ (or more accurately, international capital flows) from Cyprus, 5.8% from the Bahamas, 7.2% from Bermuda, 0.8% from China, 3.4% from France, 4.1% from Germany, 0.5% from Japan, 0.4% from Korea, 4.4% from Luxembourg, 9.2% from Netherlands, 3.7% from Singapore, 2.9% from Switzerland, 4.2% from the UK, 0.7% from the US and 0.8% from the Ukraine.

According to estimates compiled by UNCTAD, approximately 6.5% of Russia’s ‘FDI’ stock — about $28.7 billion worth based on 2017 data — was actually of Russian origin. The UNCTAD estimates also showed a significantly increased amount of European and US investment. According to the estimates produced, the US is actually the biggest foreign investor in the Russian economy, worth about $39.2 billion.

While such features of international capital flows can be useful to, for example, elude punitive sanctions from hostile states, they greatly restrict efforts to reduce corruption and improve planning and accountability. The Russian government is no doubt well aware of both the potential advantages as well as the drawbacks involved. For example, Bloomberg reported last year:

“For Russia, meanwhile, repatriating the capital that’s recorded as foreign but isn’t remains an important policy goal. In the 2019 World Investment Report, Unctad attributes the 2018 drop in Russia’s investment inflows to the government’s effort to get Russian business owners to redomicile their holdings to the home country.” LINK

While some aspects and consequences of this inimical structural feature of the international economy have been addressed, it remains a major challenge not just for Russia but everywhere.

Overall, however, the available macro-economic data and preliminary results of major joint projects between Russia and China suggest that their approach has been successful as the Russian economy has withstood the external shocks of sanctions imposed by major trading partners as well as large falls in oil and gas prices, and continued on the path of diversification, deepening and constant improvement of existing production capacities to ensure a core level of resilience and self-sufficiency without going to the other extreme of going xenophobic and renouncing foreign trade and cooperation.

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com