Why Crude-Tanker Collapse Could Be Long And Painful

Tyler Durden

Thu, 10/22/2020 – 20:20

By Greg Miller of FreightWaves

Chinese water torture is defined as “a painful process in which cold water is slowly dripped onto the scalp, forehead or face for a prolonged period of time, allegedly making the restrained victim insane.” Crude-tanker owners and investors may face their own version of this ancient torment. Today’s agonizingly low rates could be just the beginning.

The massive floating storage volumes that built up earlier this year are unloading. But very, very slowly. In aggregate, they’re dripping out. Meanwhile, oil demand is growing, but again, very slowly. Incremental oil demand is a trickle, not a flood.

First the party, now the hangover

Crude tankers filled up with storage cargoes in April-June after Saudi Arabia opened its spigots despite COVID-weakened demand. Tanker rates hit historic highs of over $250,000 per day but did so by pulling forward demand via storage deals and borrowing from the future.

The best hope for tanker markets was that storage would unwind quickly as global consumption rebounded. This was the so-called “short hangover” or “rip off the Band-Aid” scenario. It would depress rates in the near term as storage tankers unloaded and swiftly reentered the spot-market scrum. But it would hasten a return to normalcy.

Alas, new data provided to FreightWaves by intelligence company Kpler confirms that the Band-Aid is not being ripped off. It also implies that barring a major geopolitical event to supercharge spot rates, the hangover could be long and painful.

Rates sink to multiyear lows

Cratering crude-tanker rates are now well below both breakeven levels and where they normally are at this time of year.

According to Clarksons Platou Securities, rates for very large crude carriers (VLCCs, tankers that carry 2 million barrels of crude oil) averaged $17,000 per day on Wednesday. Rates were $100,000 per day at this time last year, propelled by tankers attacks in the Middle East and U.S. sanctions against China’s COSCO. Looking beyond last year’s anomaly, current VLCC rates are less than a third of their 2015-19 average.

Clarksons estimates that average spot rates for Suezmaxes (tankers that carry 1 million barrels) are $4,000 per day. A year ago, they were $86,600 per day. Current Suezmax rates are about one-tenth of their 2015-19 average.

Clarksons puts spot rates for Aframaxes (tankers that carry 750,000 barrels) at $4,500 per day. A year ago, rates were $55,100 per day. Current rates are about one-sixth of their 2015-19 average.

Floating storage unwind stuck in neutral

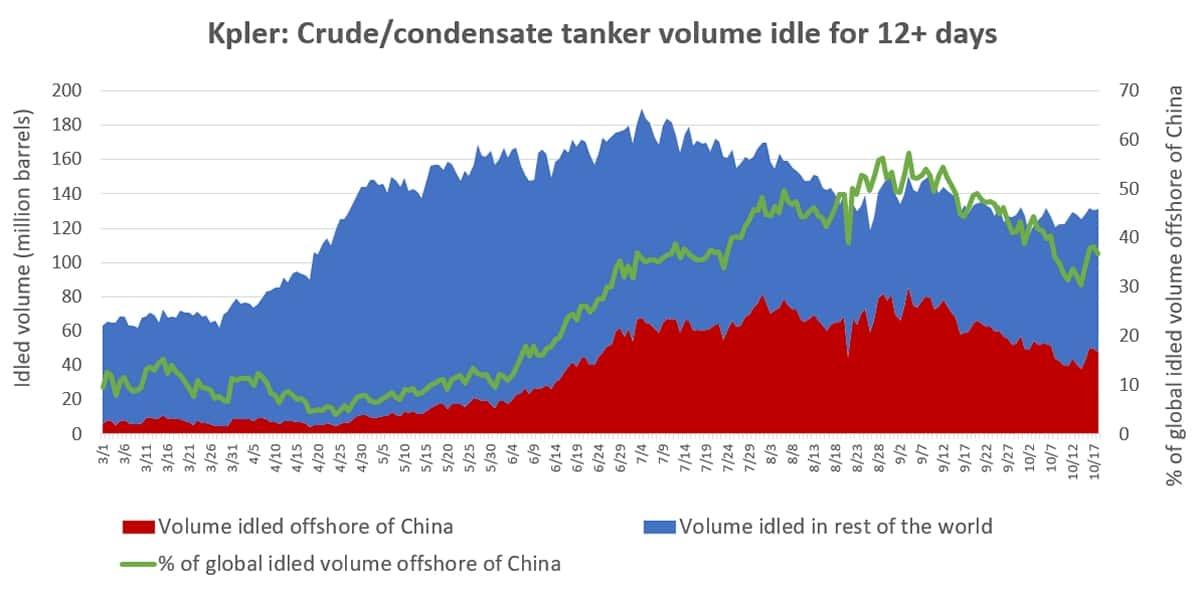

Kpler collects data on laden crude- and condensate-tanker capacity for ships stationary for 12 or more days.

This reveals how much crude is in floating storage over time, including intentionally stored cargoes and those suffering lengthy delivery delays. Kpler also breaks out how much of this laden storage is off the shores of China, where port congestion has been particularly acute in recent months.

![<!–[if IE 9]><![endif]–>](https://www.zerohedge.com/s3/files/inline-images/clarksons.jpg?itok=8L_IjmVX){kind=link}

The data shows that global crude floating storage peaked at 190 million barrels on July 1 and had fallen 31% (or 29.5 VLCC-equivalents) to 131 million barrels as of Sunday.

The negative signal for oil demand is that storage volumes have been hovering around the 130-million-barrel level since late August. Chinese storage has fallen. But non-Chinese storage has risen from around 60 million barrels in late August to 80 million barrels currently. Chinese floating storage accounted for around half of global floating storage in the beginning of September. It’s now down to around a third.

Kpler Global Energy Economist Reid l’Anson told FreightWaves that Kpler has seen the largest gains off the North Sea, on the production side, and on the destination side, off India, Japan, South Korea and in the Malacca Strait. Floating storage off the shores of destination nations is inherently bad for tanker transport demand (the oil has already been transported). And regardless of whether storage is offshore of production centers or consuming nations, it’s a bearish on current oil demand.

Crude-tanker utilization keeps falling

Kpler also provided FreightWaves with data on the percentage of unladen (empty) crude/condensate tankers versus the total fleet, based on deadweight tonnage, regardless of size category.

The numbers are ugly and confirm why rates are so low. There are too many empty ships chasing too few cargoes. And it’s getting worse.

![<!–[if IE 9]><![endif]–>](https://www.zerohedge.com/s3/files/inline-images/new-kpler2.jpg?itok=i9c_5VBj){kind=link}

The laden/unladen mix was roughly evenly split at the beginning of the year, until the Saudi production decision. That caused a surge in crude-tanker rates in March and April. That rate spike — and the ships chartered for floating storage — brought the unladen percentage down to 40%-42% in May.

But then the unladen percentage began rising. The scope of unemployed ships in the spot market increased in June even as floating storage rose. As ships have been released from floating storage starting in July, the percentage has increased further.

The higher the unladen crude-tanker percentage, the more bearish the signal for crude-oil demand (particularly in light of static floating-storage levels in late August through today). On Wednesday, the unladen share hit a year-to-date high of 52.5%.

Air-travel fears chop tanker demand

Listed companies heavily exposed to crude-tanker spot rates include Euronav, DHT, International Seaways, Frontline, Nordic American Tankers Diamond S Shipping and Teekay Tankers.

![<!–[if IE 9]><![endif]–>](https://www.zerohedge.com/s3/files/inline-images/Speakers105-burke-resized-600x400.jpg?itok=cXHbHwJo){kind=link}

As recent history has shown, tanker rates can go from bust to boom overnight as the result of major geopolitical events. But barring such an occurrence, rate prospects rely on oil demand, a topic highlighted by panelists at last week’s virtual Capital Link New York Maritime Forum.

According to International Seaways CEO Lois Zabrocky, “In the fourth quarter, we’re at 92-93 million barrels of [global oil] consumption versus 101 million barrels a year ago. COVID is still not really letting go of its grasp on a lot of the world’s population. That’s part of it. In addition, we’ve got [floating storage] destocking and OPEC is holding back [on production].

“I think there’s a structural problem in the market,” maintained Bob Burke, CEO of Ridgebury Tankers.

“I don’t think anyone on this [panel] has experienced an 8% decline in demand that seems semi-permanent. We are down about 8 million barrels a day and there’s one answer for why this is: airlines.

“The barrel-per-day [loss] seems very highly correlated to airline travel, especially long-haul travel. And because of the psychology of the consumer, there’s going to be a lot more pain in that sector,” opined Burke.

Seasonal upside vs structural downside

Higher seasonal demand in the Northern Hemisphere should bump up crude-tanker rates in the coming months. However, a combination of tepid underlying consumer demand and a languid storage unwind that slowly drips out more tankers into the spot market could create dual headwinds well into next year.

![<!–[if IE 9]><![endif]–>](https://new.libertarianhub.com/wp-content/uploads/2020/10/jon_chappell_MM18-600x336-1.jpg?itok=4sUX-D6S){kind=link}

Jon Chappell of Evercore ISI, who was just named the top shipping analyst of 2020 by Institutional Investor, told FreightWaves: “The mismatch in supply and demand is not likely to ease anytime soon.

“Although there will be traditional seasonal patterns, we expect the upside to be severely capped this year until global inventories normalize — which may take until late 2021.

“I think the VLCCs have held in better on a relative basis owing to congestion in China ports and still-elevated floating storage,” he continued. “As these issues unwind — and they are, just more slowly than many hoped — the relative performance of VLCCs and midsized asset classes should ‘normalize,’ meaning that Aframaxes and Suezmaxes will rise from above sub-OPEX [operating expense] levels, but VLCCs will likely remain under pressure.”

On the plus side, the crude-tanker orderbook is extremely low and owners should scrap older tankers if rates stay this bad. “Fortunately, we’re in a business where about 5% of the ships on average go away [via scrapping],” said Burke.

Scrapping activity has been minimal, but could increase. COVID temporarily restricted scrapping but those restrictions should ease. In addition, there has been very little scrapping of VLCCs in 2019 and 2020 because until recently, rates have been unusually strong.

As Burke put it, “If you have a pocketful of cash, you’re inclined to take another bet. So, there’s resistance to scrapping even when it would be the natural choice with rates so low.”

Scrapping and low orderbook to the rescue?

“If you look at history, it usually takes at least six months of a depressed environment to really see vessels get recycled,” added Zabrocky. “At the [rate] levels we’re at, I think we should start to see more vessels getting taken out of the market.”

Burke also pointed out that the very oldest VLCCs were inordinately placed into floating-storage duty and once those cargoes unload, these ships are prime scrapping candidates — which should temper the spot-rate headwind of the storage unwind. “A lot of the older ships that went into storage will probably go right to the scrapyard,” he said.

But can tanker rates recover in 2021 due to reductions on the vessel-supply side? Or does it ultimately hinge on reversing the cargo-demand shortfall highlighted by the new Kpler data?

Burke himself acknowledged that “if you look to the orderbook to save you on the spot market, you’re grasping for straws.”

Diamond S Shipping CEO Craig Stevenson, an industry veteran, addressed the scrapping question back in March 2009. In the midst of the financial crisis, Stevenson told Connecticut Maritime Association conferencegoers: “You’re not going to scrap your way to prosperity. Ever. You’re not going to reduce the orderbook and turn it into a good market. It won’t happen. In the history of shipping, it hasn’t worked that way.

“It’s demand,” emphasized Stephenson. “It starts with demand.”

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com