In Moment Of Brutal Honesty, JPMorgan Says Economic Disaster And More Lockdowns Will Be Great For Stocks

Tyler Durden

Mon, 11/02/2020 – 07:35

After reading months of ridiculously goalseeked Wall Street commentary, where first a Trump victory was the best outcome for stocks (at a time when Trump was seen as a favorite to win), then a Biden victory becoming the best-case outcome for risk assets (this predictably emerged around the time Biden took a lead in the polls), then a Blue Wave emerging as the most bullish outcome (around the time a Democratic sweep became the most likely outcome according to polls), and then following a brief detour when Wall Street briefly freaked out about Congressional gridlock when a split Congress suddenly became an all too real possibility, we went full circle and a Trump victory once again became the most bullish outcome (according to JPMorgan), traders and analysts would simply roll their eyes and snicker whenever a new “scenario” emerged from Wall Street’s strategy desks.

There was a simple reason for that: as One River’s Eric Peters explained earlier, ever since the arrival of MMT in March, the simple reality is that for stocks it no longer matters who is president, to wit:

When stocks bottomed on March 23rd, Trump narrowly led Biden in betting markets. But pandemics have consequences and this catastrophe hit a nation that had spent decades optimizing its economy to spur asset price appreciation. America’s financial system was as overleveraged as it was unstable. A depression was inevitable in the absence of something utterly unprecedented.

On March 27th Trump signed the $2.2trln CARES Act, and this, combined with a breathtaking array of asset purchase programs marked the effective start of MMT (Modern Monetary Theory) – with the Fed and Treasury coordinating policy.

And ever since, it has mattered less who wins this election. Because you see, once the link is broken between what the government must collect and what it can spend, who leads the nation is less consequential – at least to stock markets in the near-term.

Of course, cynics will say that the presidency – which long ago devolved into a mere symbolic figurehead position – stopped mattering for markets long before March, and the data will certainly back that up. As the following chart from Ed Yardeni shows, no matter who is president or what whether Congress is united or divided, stocks go in just one direction: up. Specifically, during the previously six “Blue Wave” periods, the S&P was up 56% on average; while during three prior “red waves”, the market rose 35% on average. As for the “dreaded” divided government period – which Bloomberg hyperbolically trumpets today in “Fund Manager Nightmare Is Biden Without Blue Wave Congress” – well guess what, during the seven periods of divided government: the S&P up a whopping 60% on average!

Based on this, one can argue that gridlock is the best thing for stocks.

Why? Because the more dysfunctional the presidency, and Congress, the more the Fed has to take matters into its own hands. In fact, it is this very logic that has allowed stocks to soar to all time highs even as the economy barely grew for the past decade and then cratered into the steepest contraction on record.

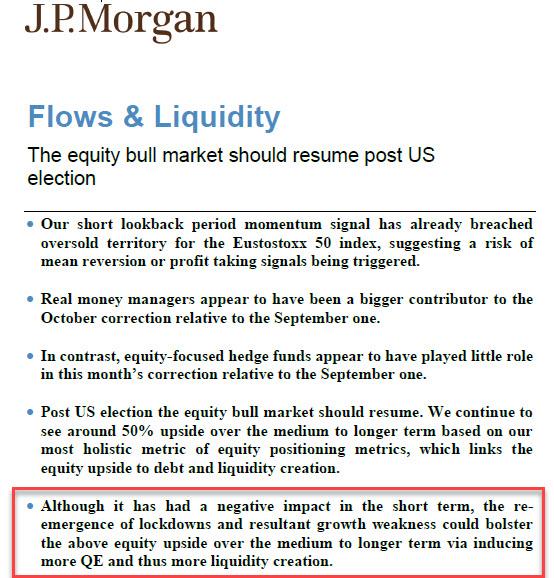

And for once, we had an honest, objective assessment from none other than JPMorgan, which in its latest Flows and Liquidity note published on Friday cuts to the chase and without any of the now ridiculous “narratives” writes that “The equity bull market should resume post US election.”

Why? For two simple reasons: i) a surge in debt which will boost stocks as it has for the past century, and ii) if it’s bad the Fed will step in.

In fact, the worse it gets the better it will be for stocks, and in a moment of brutal honesty from the largest US commercial bank, JPMorgan’s Nick Panigirtzoglou who is clearly tired of goalseeking why every single political scenario would be bullish for stocks, admits that even another economic catastrophe such as a new round of lockdowns will be great for markets, to wit:

Although it has had a negative impact in the short term, the reemergence of lockdowns and resultant growth weakness could bolster the above equity upside over the medium to longer term via inducing more QE and thus more liquidity creation.

For those who don’t believe us, here is the original:

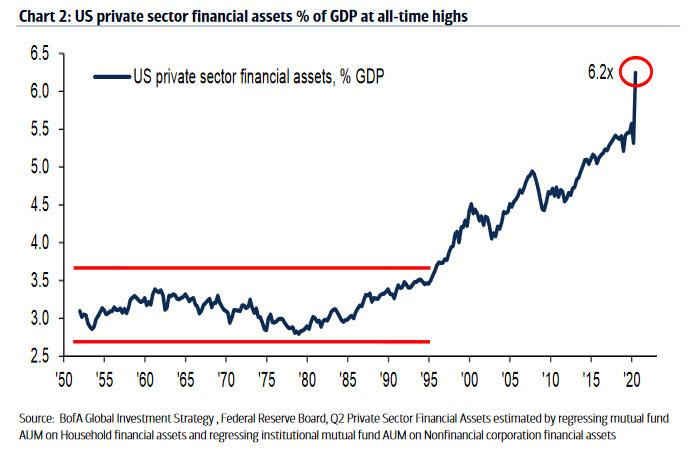

Yes – JPM did in fact state what “tinfoil blogs” had been saying for over a decade: that the worse the economy gets, the better it is for risk assets as the Fed has no choice but to step in and keep bailing out bulls as the alternative – a full-blown market crash – is simply an inconceivable scenario for a country where private sector financial assets now represent a record 6.2x the GDP…

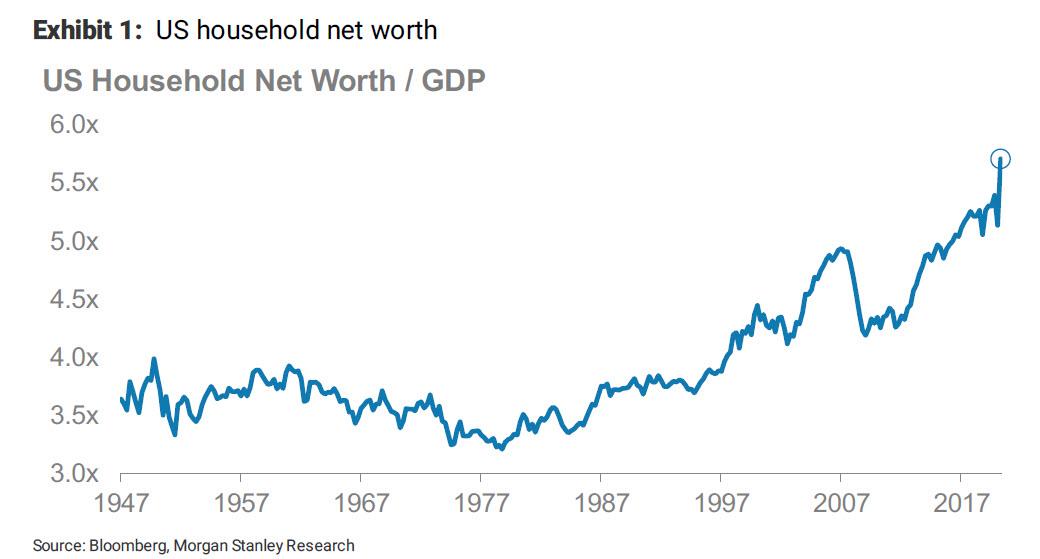

… and where household net worth which is mostly in financial assets, has never been larger.

Here is the full excerpt from JPMorgan:

We believe that, similar to September, this month’s correction offers a good entry point to equity investors over the medium to longer term once US election uncertainty subsides next week. As we explained before, our most holistic measure of equity positioning metrics based on global non-bank investors’ holdings of bonds, equities and cash (M2), points to an equity allocation (equity share) of 39.73% at the moment, still significantly below its post-Lehman period average of just over 42% and well below the cycle high of 47.6% in early 2018. The equity appreciation needed to shift the implied equity allocation of non-bank investors globally from the current 39.73% share to the post Lehman high of 47.6% (Jan 2018) is 47% for the MSCI AC World index and 54% for the S&P500 (given its higher 1.16 beta relative to the MSCI AC World index). The above calculations assume the stock of cash or money supply rises by another 7.5% from here and the stock of debt by another 5% from here. In other words, the upside for equities over the medium to longer term depends more on debt and liquidity creation and thus central bank QE than on fiscal stimulus.

This doesn’t mean that any fiscal stimulus post US election would not have implications for markets. It would, but more in terms of how steep the yield curve or how broad the equity bull market is going to be post the US election, i.e. whether it would encompass value and traditional cyclical sectors or continue to be more narrowly focused on high quality and growth oriented stocks.

It also means that the virus resurgence and the reemergence of lockdowns and growth weakness could bolster the above equity upside via inducing more QE and thus more liquidity creation.

And so, for all those wondering why the powers that be – certainly should Biden win the presidency – are rushing to enforce another full-scale lockdown of the economy, the answer is simple: they want to get even richer. Meanwhile, all those tens of millions of Americans who will certainly lose their jobs again, and all those proprietors of small and medium businesses who will see their companies snuffed out… well, for a handful of ultra rich to get even richer, others have to lose it all.

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com