Inequality And The Gold Standard

Tyler Durden

Sat, 11/28/2020 – 23:00

Authored by David Howden via The Mises Institute,

[First published by Mises Canada, December 2013.]

Imagine that you earn $40,000 a year and your boss doubles you at $80,000 a year. Business was good to you both in 2013, and you received a 25% raise for your efforts. Not bad, and your boss gets to share in this good fortune too with an extra $25,000 (about 30%). You’re going to make $50,000 in 2014 and your boss will pull in $105,000.

Are you happy with this deal? Probably. But wait, income inequality just increased! Your boss originally outpaced you by 100%, but now his salary is 110% higher than yours.

To read the brouhaha going around right now, this situation is cause for alarm. Income inequality has increased and despite the fact that everyone is doing better than they once were, one group is doing relatively better.

What about if we reverse the example, starting from the original salaries? Instead of having a great year, imagine things were very bad and salary cuts are going around. You get a 25% pay cut so that you will now be earning $30,000 a year, and because he has more responsibility about the direction of the business and its lack of success, your boss gets a larger pay cut of $25,000. (This situation is the mirror image of the first example.)

You are making much less than you did last year. Are you upset about this? Probably. But wait, apparently there is a silver lining. Your boss now “only” makes about 80% more money than you, versus the 100% salary differential that existed last year. Income inequality decreased!

Apparently you can take solace in knowing that the playing field has been levelled, even if your kids are going to have a tough Christmas morning one year from now.

This is admittedly a very simple example. What I am trying to show is that the income inequality debate is not as straight forward as it is commonly framed. It is not just a question of one group getting a larger piece of the pie, but of increasing the size of the pie so that everyone can benefit.

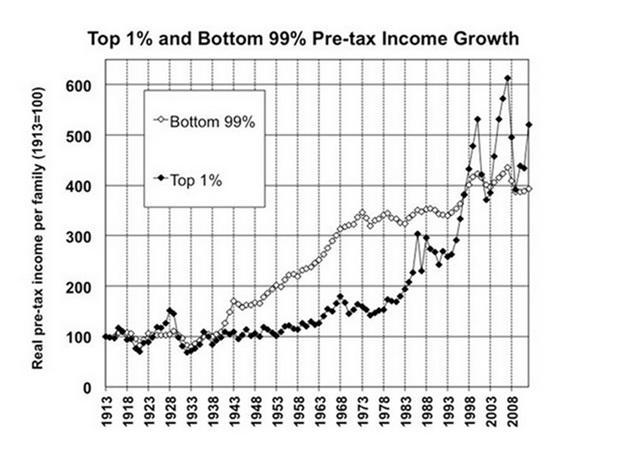

John Cassidy recently entered the melee with a very digestible look at American income inequality over time. In his “six charts” there is some of the same (the top 1% of earners have seen their share of the pie rise rapidly over the past decades) and also some surprises.

Relying on data from Berkeley economist Emmanuel Saez, Cassidy shares the following graph showing changes in real income growth over the past century.

First let’s look at the top 1%. There seem to be about three distinct periods their incomes have gone through. The first from 1913 to roughly 1973 is more or less flat. Real incomes for the top 1% were no higher in 1973 than they were around 1930. After 1973 however there is a sharp and mostly uninterrupted spike upwards which seems to stop around the year 2000. After 2000 their real incomes have ebbed and flowed, primarily in response to capital gains and losses on their stock portfolios. Even though the volatility of their income has increased, it still remains quite high relative to any time over the past 100 years.

Compare this with the bottom 99%. There seem to be about four distinct periods of real income growth. From 1913 until the end of the Great Depression, real income remained more or less constant. The 1940s, 50s and 60s saw a rapid increase in real income growth, far more rapid than what the 1% experienced. This came to a sudden end around 1973 and a stagnation until the early 1990s. Then from 1993 onwards we see the same final stage as the 1%. Increasing real incomes (though much slower than the 1%) but more volatility as well.

There are many things which are the same in these two trends, but the one year that probably pops out for people who think income inequality is a bad thing is 1973.

This year marked the end of the steady advance for the 99%’s real income gains and set in motion the rapid advance of the 1%. In other words, the marked income inequality we see today is a product of the post-1973 world.

So what happened in 1973? Many things as it turns out. Decreased unionization was getting underway in the U.S. economy around this time, as was the spike in the price of oil.

Russ Roberts over at Café Hayek has a different explanation. He thinks it has to do with changes to the family unit. Large increases in the divorce rate and a steady increase in the number of households headed by women could be to blame for the sudden jump in income inequality.

Maybe, but although this could be a reason why, I doubt it is the primary reason.

Let’s try an informal test. What was the biggest event to occur in 1973?

Americans probably will answer Roe v. Wade, the completion of the World Trade Center as the world’s tallest building or the beginnings of the Watergate hearings. Maybe the start of withdrawal of troops from Vietnam or Britain joining the European Economic Community. Or for sports fans it could be Secretariat winning the Triple Crown and getting immortalized on the cover of Time.

Actually the most important thing to happen in 1973 actually happened in 1971, August 15th to be exact.

On that date Richard Nixon closed the gold window. The U.S. dollar was convertible by foreign governments into gold under the then-existing Bretton Woods system at the great price of $35 per ounce. Continued redemption demands by some belligerent countries (primarily France) drained the U.S. of its gold reserves until the breaking point when it became questionable how much longer this could continue for. In what could have been the most important day of the 20th century, Richard Nixon decided to renege on the U.S.’s promises to foreign governments and essentially default on its currency. No longer was the U.S. dollar tied to gold and the U.S. no longer had to worry about spending beyond its means.

Well, almost no longer. While there was no convertibility into gold after 1971 there was still that old bugaboo of fixity in the exchange rate. The U.S. dollar still functioned on a fixed exchange rate standard relative to gold until 1973, even if there was no convertibility. This meant that the U.S. was still not free to expand its money supply or incur ever increasing budget deficits at will. It had to target a dollar price of gold, which was reset a little higher in 1971 to $38/oz. Even though there was no redeemability, the U.S. was legally obliged to target this gold price, something which tied its hands concerning the extent to which deficits could be run and expansionary of the money supply policies could be pursued.

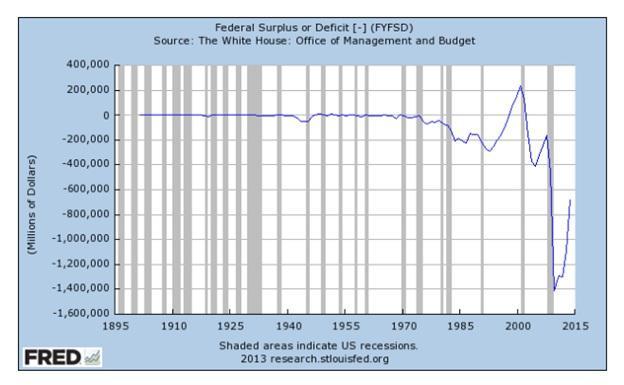

The effect on the deficit is easy to understand in light of this.

Since the late 1880s (and before) the U.S. government ran a somewhat balanced budget. Minor blips appeared during the two World Wars, but by-and-large the deficit hovered very close to the zero line. In the late 1960s we can witness the a growing deficit, partly in response to the cost of the Vietnam War but even that is relatively mild to what would come later. Likewise, 1971 also witnessed a growing deficit but the year which defines the point of no return is clearly 1973. At that point the U.S. deficit went into freefall and besides a few surplus years in the late 1990s it has never recovered.

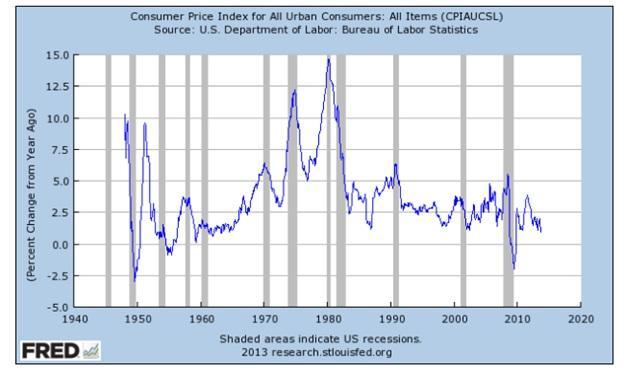

The effect was also pronounced on prices.

Prices were indeed climbing throughout the 1960s, but 1973 was also the year that set off the most inflationary episode in America´s history. Being unhinged from that relic of gold, the Federal Reserve could increase the money supply and monetize the Federal government’s budget as it wanted. This culminated with 15% annual inflation in 1980 something which took a very strong-minded Federal Reserve chairman by the name of Paul Volker to tame by putting the breaks on money supply growth.

Inflation looks tame today, though the experience following the 1973 decoupling showed what happens when you let the government spend at will without any restraint. Gold provided restraint, just as political gridlock should today. But in the period of the mid to late 1970s there was no such luck.

All this takes us back to the original question: why did income inequality increase so much after 1973? We can look to two factors both related to the loss of the gold exchange standard in 1971 and the arrival of flexible exchange rates two years later.

-

First, as the U.S. government no longer had to worry about redeeming U.S. debt held overseas in gold, it was able to spend without restraint. Of course, this created a large budget deficit quickly, something which needed a solution.

-

This brings us to the second point. By monetizing the U.S. budget deficits, the Federal Reserve set off a period of high price inflation.

The reason why there is growing income inequality since 1973 is a direct result of this monetary mayhem. All this new money needs an entry point into the economy. Someone has to get it first and spend it. When they spend this newly created money they do so at the existing set of prices, but in the course of making these expenditures prices will rise. Those who get the money first “win” in the sense that they get a free lunch – they have a greater income and can spend it before prices rise. Those who get the money last are the “losers” – they get access to this money eventually as it is spent (trickles down?) but by the time that occurs, prices have already risen. They are no better off.

The 99% that have become relatively poorer over the past 40 years are those who get access to this new money last. (Remember however that these people are still, thankfully, wealthier than they were 40 years ago.)

Who are the remaining 1%, then? Well, who gets the money first?

Government officials and contractors, to the extent that they gets the proceeds of all the newly created money are the first and primary beneficiaries. Big banks and financial institutions also win as they are the enablers who help this newly created money enter the economy. Incidentally, 99 times out of 100, when we think of someone in the 1% who is getting ahead of the rest of us, they probably either work for the higher echelons of the government or are involved in the financial industry.

Coincidence? I doubt it, and you just have to go back in time to 1973 to understand why.

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com