Prospects For The UK & The Pound

Tyler Durden

Sun, 12/13/2020 – 07:00

Authored by Alasdair Macleod via GoldMoney.com,

This article assesses the likelihood of the pound following the dollar into monetary hyperinflation. Between March and September, the US Government financed twice as much of its spending by bond sales — mostly through inflationary QE — compared with tax revenues. And there is much more monetary inflation to come.

A hyperinflating dollar is now the international backdrop for all currencies, including sterling.

To date, the UK’s budgetary arithmetic is less alarming than that of the US. In theory, the UK government has a workable plan, to turn the UK into a global entrepôt. However, if, as is becoming increasingly certain, the dollar falls heavily on the foreign exchanges in the coming months, dollar interest rates will rise, and so will those for sterling — catastrophic for government finances and the future of debt-laden zombies. Furthermore, with counterparty exposure to insolvent Eurozone banks and escalating covid-related insolvencies, British banks are not strong enough to withstand the general credit contraction a rise in dollar rates would trigger.

As a matter of utmost urgency, the UK Treasury should rebuild the nation’s gold reserves, secretly if necessary, so that the government can stabilise the pound by backing it with gold at the appropriate time. There is then a way out of this mess, but will the UK government take it?

Introduction

Living in the UK one is all too aware of the visible damage the virus lockdowns are doing to the economy. Hotels, pubs and restaurants have been driven towards bankruptcy, and only those whose owners have enough stored wealth to pay the bills while there is little or no income will survive. Many retailers whose margins were slim after paying rent, local authority rates and sales taxes have closed for ever. To some extent these problems have been deferred through payment holidays and furlough schemes. But the fact remains that high streets in the market towns up and down the country have had the heart ripped out of them.

Major retail chains are now going bust. If only the government could recognise it, the changes we see today were going to happen anyway. But instead of an evolutionary process it has been brought about all of a sudden by the covid crisis and its handmaiden, a likely banking crisis to follow. Schumpeter’s process of creative destruction has been bottled up for ten years before being unleashed.

If permitted, the new world that beckons the UK is high streets which combine housing, shops and all the other facilities that humans decide between them are required and desired, and not those mandated by planning laws and local government. The travel industry has taken a massive hit, with spontaneous airline travel probably going out of fashion: why not stay at home nine times out of ten and watch documentaries on the places you would otherwise have visited? British holidays taken by Brits who in the past went abroad could become a future growth industry.

One could go on, but the point is that Britain is not going to return to the old normal. And the principal obstacles to change are central government and the local authorities. Through massive waves of monetary inflation, central government is supporting the world of yesteryear, of business zombies. And because they are losing income from business rates, the local authorities are resisting the change of use from retail to housing. In fact, if they embraced this evolution in the towns and cities, much of the “housing crisis” everyone talks about would disappear without the need to concrete over much of rural England.

To be fair to the politicians, they are always elected not so much on a manifesto, but to maintain the status quo ante. No one votes for evolution. They vote for new businesses, green energy and the rest, on condition that their existing businesses and jobs continue unaffected by change. And in a Keynesian world, where monetary capital can somehow be created out of thin air, it appears to everyone to be eminently possible. And as is the situation in nearly all advanced economies, UK government policies backed by monetary inflation have resisted change, fostering crony-capitalism, regulatory protectionism and zombie businesses.

The current UK government and its cabinet ministers must be extremely frustrated by the predicament they find themselves in. As elected politicians they started out being perhaps more free market orientated than any post-war administration. All that intent is now on hold, and they are forced into retreating into the same old botched policies of perpetuating yesterday’s businesses and backing today’s failures.

This article examines the specific economic and monetary situation faced by the United Kingdom. There is an eventual way out of the covid trap, but it cannot be achieved by relying on bureaucratic intervention and ignoring monetary and economic developments elsewhere.

The government spending problem

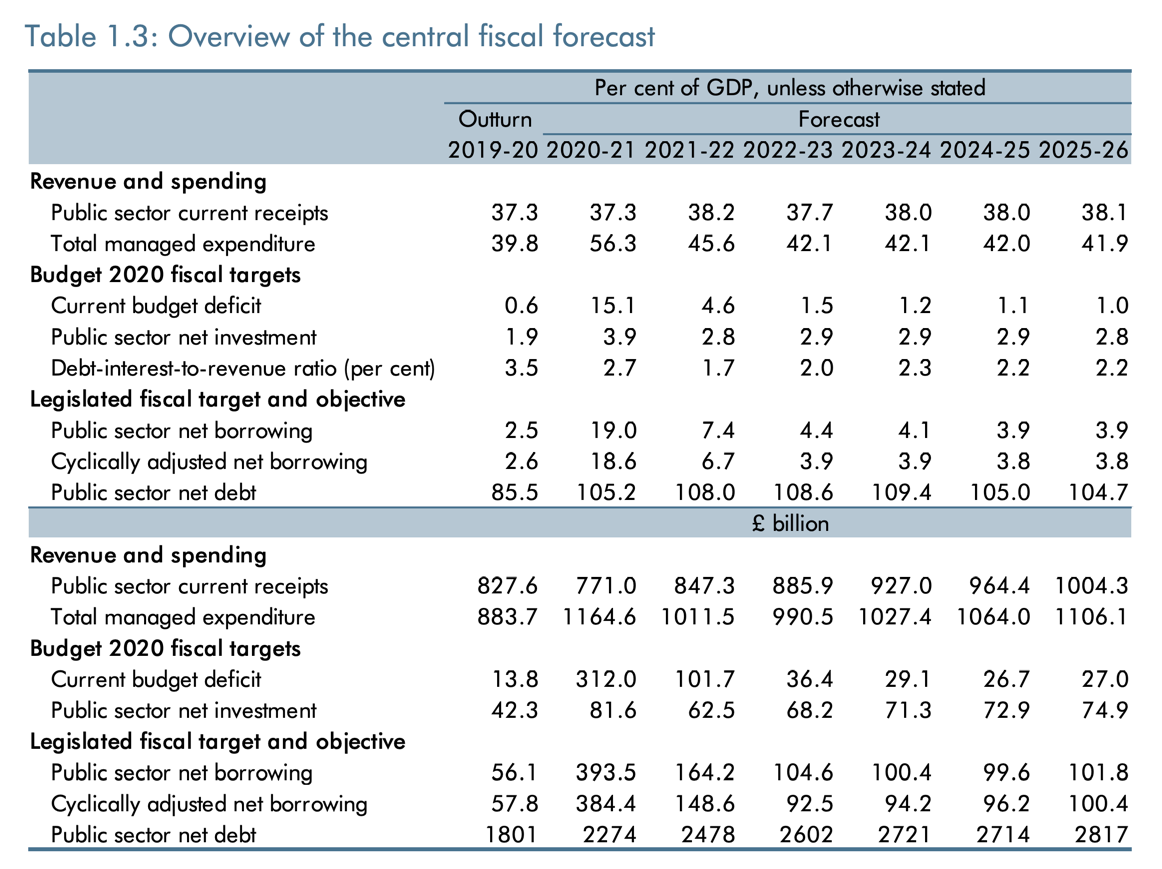

The screenshot below is taken from the UK’s Office for Budget Responsibility’s Economic and Fiscal Outlook, published in November.

It is probably true that in the few weeks since it was published this central forecast has drifted somewhat towards a worst case, particularly as it is now unlikely that covid restrictions will cease before the end of the first quarter of 2021. With nearly four months yet to run, the estimate of public sector net borrowing for the current fiscal year to 5 April 2021 is likely to be revised up from £393.5bn to well over £400bn. And the estimate that it will then fall to £164.2bn in 2021—22 appears increasingly optimistic. Elsewhere in the document, the OBR admits it is guided by the IMF’s World Economic Outlook, published in October, “[whose] projections were, however, compiled before the strength of the second wave in Europe and the US became evident”

As is usual for all government agencies, the OBR seems oblivious to what GDP actually represents. Their analysis is on the basis that GDP is economic activity, when, in fact, it merely records the monetary value of included and recorded transactions, a value that only reflects the addition of central bank money and bank credit in the period covered. The easiest way to goal-seek a nominal GDP number is to print money, which is exactly what the Bank of England has been doing ever since the Lehman failure. Quantitative easing between 2008 and 2019 produced an extra £645bn in circulating currency, during which time nominal GDP increased by £625bn, a difference of only 3.2% which could easily be attributed to other factors. Subsequently, in 2020 the extra QE to deal with the virus is £250bn, an additional 13.8% to M1 money supply, before supplementary lending schemes by the Bank through commercial banks are taken into account.

The pretence that inflationary financing is beneficial arises only from what is seen; the magic of government money being distributed for the common good. What is not seen is the dilution of everyone’s savings, assets, earnings and pensions for the benefit of the government’s finances. The transfer of wealth leaves everyone worse off, once the economy has absorbed the extra fiat money. The benefit is visible, while the cost is hidden and cannot be easily quantified. And every time the Bank deploys QE it is transferring yet more wealth from the productive economy to the government. It is a policy that ends up bankrupting the nation and destroying the currency.

In common with other central banks, the Bank of England denies that wealth is transferred, or at least if it is it is limited to the 2% inflation target, which is somehow “stimulative”. But as a consequence of the statistical imperative to reduce the cost of indexation to the government, changes in the CPI as a measure of the general price level have become both misleading and meaningless. There is no independent estimate of the UK’s rise in the general price level, but we know from the US that independent calculations place the rate of US price inflation closer to ten per cent every year for the last ten years, while the official CPI has hardly deviated from its 2% target, the same as that of the Bank of England.

The evidence is that government statistics have become so self-serving that in any proper analysis they must be ignored. The expansion of the money quantity is the relevant story to follow. Since the Lehman failure, the UK’s M4 broad money supply has increased by about 50%, diluting the monetary value of GDP accordingly, a process likely to accelerate even faster in the future as a result of covid.

Rather, therefore, than challenge the OBR’s assumptions about future GDP, we should accept it is a meaningless figure, useless for estimating economic progress and its future course. And being the basis of all economic modelling by government departments, their models should be rejected as well. Furthermore, the OBR’s forward projections look eerily similar to the guesswork of the US’s Congressional Budget Office.

Neither agency can have a clue about future economic activity. It is unknowable. As Ludwig von Mises put it, the assumption is of an evenly rotating economy, where the human action that drives economic progress is ignored. But by not understanding the difference between progress and an accounting total, it inevitably leads to an error: the support of yesterday’s businesses which are less relevant to the future, and that consume capital instead of adding value demanded by consumers. Evidence of policy support for these zombies is found in the Bank’s Term Funding Scheme (TFS) and the incentives for commercial banks to lend to smaller business, leading to £56bn in loans being made under these schemes since March.

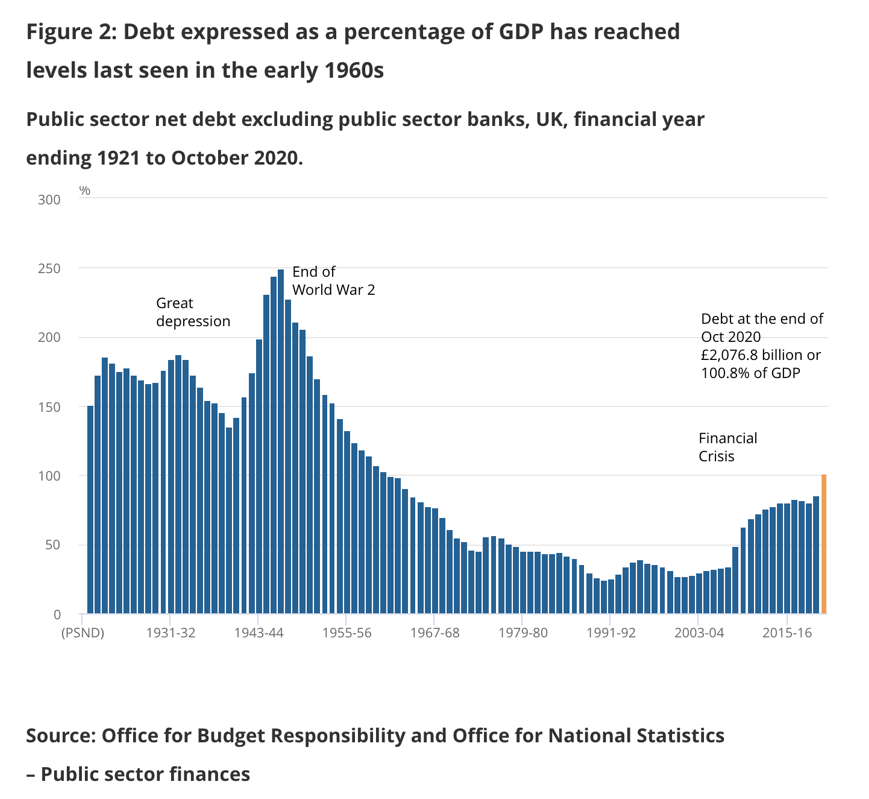

In the narrow context of public sector indebtedness, the situation is nowhere near being a disaster, as the next screenshot, of central government debt to GDP shows.

The scale of government borrowing is not where the problem currently lies. Britain has tolerated far higher levels of relative government debt in the past and managed to reduce it over time. Furthermore, by issuing undated gilt stock, it is possible to fund government spending without the principal ever having to be repaid. Arguably, the current situation could present such an opportunity.

The UK’s economic problems are analogous to the situation in the mid-1970s, when government debt to GDP was half the current level. But with a socialist government bent on destroying private sector wealth, nationalised industries dominating the economy, and trade unions emasculating businesses of all sorts, the then Chancellor of the Exchequer, Denis Healey, was forced to go to the IMF for a bailout loan in 1976.

The situation today has different content, but similarities in terms of overall effect. Income and corporate taxes are lower for the wealth creators, but instead of being hampered by rampant trade unionism, businesses have been burdened by unproductive debt since before the Lehman crisis. Coupled with increasingly onerous regulation, the UK economy has been like an overloaded aircraft struggling to get off the runway. Private sector debt at end-2019 is estimated at £3.429 trillion, about 1.6 times GDP. This has increased from £2.965 trillion at end-2008, when it was almost the same ratio to GDP. The increase in the private sector’s debt to GDP number occurred before the financial crisis, rising from 94% since 2000, while in Keynesian terms, the economy has merely stagnated ever since.

For Britain, the financial crisis of 2008 was the unwinding of excessive bank credit, and ever since then the policies of successive UK governments have been focused on preventing business failures. Consequently, the UK economy has become increasingly dependent on continuing support from inflationary monetary policies and the extension of that debt. It leaves the government and the Bank with the problem of supporting a private sector, which remains at least as vulnerable as it was in 2008, and under Denis Healey in 1976.

Indeed, the current Chancellor is doing what he can to support today’s zombies. And it is becoming clear that yet more help from him will be needed to fund the private sector through the entirety of the covid pandemic. Except at the margins, tax rises can be ruled out along with cuts in public spending, which places the entire emphasis on the magic money tree. And no one yet is talking about a post-pandemic world, merely assuming there will be a return to the normality suggested by the government’s economic models, where consumers will be fully employed, paying their taxes and spending their money on the same items as in the past.

To these uncertainties are added Brexit. At the time of writing, trade terms with the EU have not yet been agreed. But if there is no agreement, no doubt the government will announce new measures to support industry through the necessary changes, financed, of course, by further monetary inflation. But after that, Britain will have to become more of an entrepôt, and this is indeed planned with a series of free ports. But for the policy to be successful it will require the government to allow all capital resources to be mobilised towards new businesses, which can only happen if zombies are abandoned to their fate.

Sterling and post-Brexit challenges

The mistakes of monetary and government policies described above fail to anticipate three problems that seem bound to derail them. The first is rising interest rates, which I shall address later. The second is an almost certain banking crisis, which will involve Britain’s banks, which will also be addressed later. And the third, which we will now discuss, is the potential for foreign ownership of sterling to undermine the currency.

Due to continual trade deficits, Britain’s balance of payments has led to an ebb and flow of foreign ownership of UK financial investments, including government stock. The liquid element is ownership of bank deposits, reflecting commitments in wholesale money markets and correspondent banking balances. Foreign ownership of non-financial assets and listed equities is estimated at about £4 trillion, not far from twice GDP.[iv]

If the government allows the economy to evolve itself, then as an entrepôt Britain should be able to retain and make a virtue of this involvement. Furthermore, a side benefit of covid is that budget deficits, particularly those of the US, are leading to increasing trade deficits. While domestic markets may be tanking, export business to the US and other consumer-driven economies is set to boom next year, offering substantial opportunities for UK businesses, much of which is internationally owned. For this to work effectively the whole structure of the economy must evolve, with the state reducing its burden on the economy. But that can only happen following the current crisis, which I will address at the end of this article. Meanwhile, we must assess the position of the more liquid foreign investments in sterling.

Foreign investment in gilts is estimated at £560bn, but sterling is still a substantial part of foreign exchange reserves for central banks, and offshore captive insurance companies also hold their sterling liquidity in gilts. These balances are likely to be broadly retained. If there is to be pressure on sterling, it is likely to come from sterling deposits in British banks from non-residents, which according to the Bank of England’s database totalled £537bn at end-October. If, in the coming days there is no trade deal with the EU, it is reasonable to assume some of this balance will be sold, driving sterling lower from its recent highs against the US dollar. But that in itself seems unlikely to be enough to destabilise sterling beyond its normal volatility.

British banks

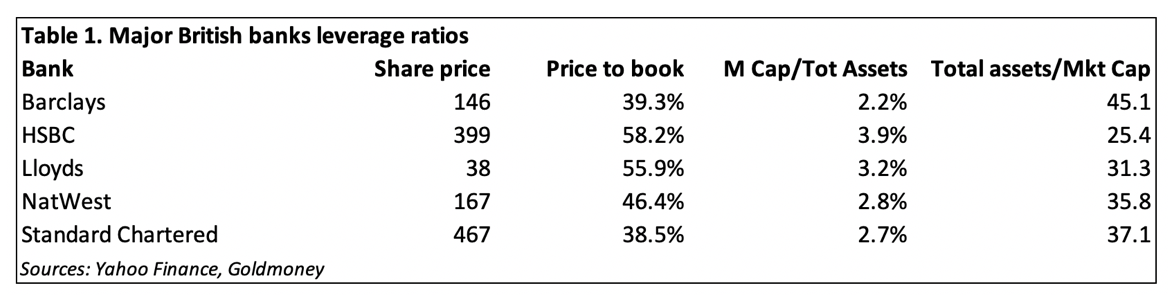

Systemic risk is eerily absent from nearly everyone’s radar, but as Table 1 below shows, the big five UK banks are highly leveraged, particularly when the market discount to book value is taken into account.

Along with share prices of banks in the EU, British banks have rallied strongly since mid-September, but in most cases their market capitalisations are still less than half their balance sheet equity. The position for many Eurozone banks, with which London has significant counterparty risks, is more troubling. Furthermore, both HSBC and Standard Chartered have substantial exposure to China and Hong Kong, which implies there are geopolitical and counterparty risks from that region as well. Clearly, the British banking system is inadequately capitalised for an economic shock, such as the accumulation of bad debts from the covid pandemic, or for that matter, a banking crisis in another jurisdiction.

We should note that the global cycle of bank credit moved from a ten-year expansion to a sharp contraction in September 2019, when the US repo market indicated the dollar-based banking system had run out of balance sheet capacity. This was about a year after it became clear that the trade tariff war between the US and China had destabilised international trade, and about ten years after the expansionary phase had started. There is enough evidence, even from the nineteenth century, that the expansionary phase of bank credit, when bankers move from caution to increasing lending confidence, usually lasts about ten years.

As we saw with the Lehman crisis, the expansion of bank credit had led to speculation, malinvestments and rising interest rates, a recipe for an impending crisis that ends with bank failures. With Eurozone banks in a far more fragile condition today than those in the US, where the liquidity crisis in September 2019 occurred, it seems highly likely that that is the weakest point in global banking. And given that TARGET2 imbalances are hiding accumulated bad debts, covid-related bankruptcies and a global credit contraction will almost certainly lead to a collapse of the Eurozone banking system — possibly in a few months or even weeks.

The UK Treasury will then be faced with either nationalising the entire UK banking system, or at least underwriting their entire balance sheets, amounting to some £5.4 trillion, over twice the UK’s GDP. At that point, the Bank of England, in common with other major central banks, will be faced with a slump in the economy, and its Keynesian response will almost certainly be to flood the system with inflated money in an attempt to stabilise it. Its other policy tool, interest rates, was always useless, which is our next topic.

The fallacy behind interest rate suppression

The Bank of England believes that interest rates are the cost of money and that by lowering them economic activity can be stimulated. That its policy planners still believe it in the face of continual failures to achieve their policy objectives is a triumph of hope over experience, and is certainly not confirmed by theory either.

In the nineteenth century, Thomas Tooke noticed that the rate of interest and the general level of prices were positively correlated, an observation repeated in 1923 by Arthur Gibson in an article for Banker’s Magazine. It was named Gibson’s paradox by Keynes in his 1930 publication, A Treatise on Money. Keynes commented that it was “one of the most completely established empirical facts in the whole field of quantitative economics.” Subsequently, he chose to ignore it.

The point is that the correlation is between rising interest rates and rising prices, and not between falling interest rates and rising prices. In other words, the rate of price inflation cannot be managed by raising interest rates.

The economic and empirical facts behind the relationship between interest rates and prices take on a new importance, because the Bank of England is clearing the way for negative interest rates. Again, the Bank flies in the face of experience, because negative interest rates in the Eurozone and Japan have failed to stimulate prices, the reason for this failure being explained by Gibson’s paradox. But misjudged experiments with interest rates can only persist so long as the purchasing power of fiat currencies does not collapse.

The risk of such a collapse is now acute. While it is not yet the case for sterling, there can be no doubt that the dollar is set for monetary hyperinflation. Between March and September (the second half of the US fiscal year) one third of US Government spending was funded by taxes, and two-thirds by sales of US Treasury bonds, mostly through QE, which amounts to monetary inflation. And it is not ending there. There will be a second round, once the presidential election is finally settled, and again, the US Government will face the need to fund its spending more through monetary inflation than by tax revenue. In short, without substantial cuts in budget spending, the purchasing power of the dollar is on its way to a collapse in its purchasing power.

The first hit to the dollar is now developing from the unwinding of excess foreign ownership. Foreign ownership of US financial assets in total amount to $28.5 trillion, or about 150% of US GDP, and $6 trillion of this in bank deposits and short-term bills. It will only be a matter of time before lenders realise there will be certain losses by not taking into account the future values of dollar loans in their interest rate calculations. Selling of dollars is bound to increase and term interest rates will then rise. Government finances will be fatally undermined, and term rates being the basis of comparative valuation for equities are likely to crash.

The process has already started, evidenced by the fall in the dollar’s trade weighted index and the rise in the yield on the ten-year Treasury bond. Rising dollar rates will lead to the ending of negative rates in other currencies along with talk of them at the Bank of England as well, and sterling interest rates will begin to rise. The walking shadow of Denis Healey will return — but this time there will be no IMF bailout available. It will be exogenous events that will do for sterling, likely emanating from a collapse of the Eurozone banking system or from a collapse in the dollar and dollar-denominated financial assets.

A strategy for the future

Let us make two assumptions: firstly, that the current government remains in power for its full term, and secondly that the Prime Minister and other senior ministers retain their belief in free markets. These being the case, it should be possible to reconstruct the UK economy on better lines, following the following eight steps.

1. Restore the Treasury’s stock of gold bullion as soon as possible, now that it is becoming clear that the dollar is hyperinflating and that sterling is at risk.

2. Let sterling slide with the dollar and other fiat currencies. The destruction of the currency is a precondition for reform, which cannot be achieved without the electorate realising welfarism and state intervention must be abandoned. And in any event, attempts to support unbacked fiat pounds will fail.

3. Before the pound disappears into complete worthlessness, make it convertible into gold at the then prevailing rate. The purpose of widely owned paper and digital money will no longer be to act as the state’s money, but to act as a mechanism for distributing monetary gold via the currency acting as a gold substitute. Gold coins as sovereigns and half sovereigns must be permitted to circulate alongside gold substitutes and be available to citizens on demand.

4. The ability of government to pay for and deliver any welfare and education services will be destroyed, as well as its ability to regulate the private sector. Government must retrench to provide only defence, policing, and the legal system. Everything else must go, and while it will be painful, a worthless currency will make it obvious to the electorate that there is no alternative to substantial cuts in government spending and a radical reduction in the scope of its activities.

5. Local communities should be encouraged to take over the running of schools, hospitals and health services on a charitable basis. The establishment of sound money will make this possible soon after the initial disruption.

6. Banking must be reformed. The banks that survive should be made by law to have unlimited liability for directors and shareholders, in order for the credit cycle to be tamed, while retaining some flexibility for seasonal financing factors.

7. As the economy rebuilds, the government must pursue hands-off, sound money policies, and allow the private sector to recover national wealth without an undue burden of the state. People must learn to look after themselves and take responsibility for their own decisions.

8. Never again should the government regard itself as being above the people.

Following the ending of the fiat pound, it should take no more than a year or two for economic stability to return, the consumer to drive competition and the trend for human progress to return.

![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com