The Stage Is Set For A Bull Market In Oil

Authored by Dylan Grice via TheMarket.ch,

In late 2019, we published a report and recommended an exposure in the oil and especially the oil services sector. Down by over a third since we first did our research back in December of 2019, and down by as much as 70% during the March crash, it has been our worst performing idea by a wide margin. Hence, we felt it was high time for an update.

We’ll start by retracing our original idea. Then we’ll try to understand what was missing from it, and why it went so badly for us. We’ll end by bring the idea up-to-date and in so doing, make the case that the oil industry has an essential role to play for coming generations.

Yes, energy transition is real and, for what it’s worth, something we are completely in favour of. The question is when it happens, not if it happens, but the implications from it taking several decades rather than several years vary enormously. The cornerstone of our thesis is really that the oil industry is being written off prematurely. From that premise, everything else follows.

A shortage of capital

In very simple terms, writing in December 2019, as the first reports of a mysterious virus circulating in the Chinese city of Wuhan reached Europe, we felt that the energy slump was behind us. The excesses which had led to the shale crash were being worked out, bankruptcies had soared, and capacity had been reduced. Yet the world still needed oil, and the oil majors were beginning to sanction large projects again. There was a shortage of capital, not opportunity.

We also liked the people driving capital allocation in the energy market. In particular, we liked that experienced and successful investors like Sam Zell and John Fredriksen were moving in, self-made billionaires who’d made their fortunes partly by buying things that no one else wanted over the years. On the other side, the «sellers», were politicians, bureaucrats and other non-economically motivated players (primarily ESG-driven investors).

We were comfortable that the energy transition was real but concluded that this was a) glacially moving, and importantly, b) a widely understood shift. Oil was still needed in the meantime, and so «low-risk» oil extraction from relatively low-risk short-cycle projects which could be quickly ramped up was more than merely viable, it was essential.

Only shale-oil players and the shallow-water projects fit this bill, but we’d had terrible experiences with shale oil producers in the past – they are hopelessly drill-addicted capital misallocators. Shallow-water drillers and servicers were our sweet spot by default. Given the near-term uncertainty in the space, we felt those with strongest balance sheets were best positioned to ride out any remaining volatility. We gave Tidewater and Standard Drilling as examples.

What happened?

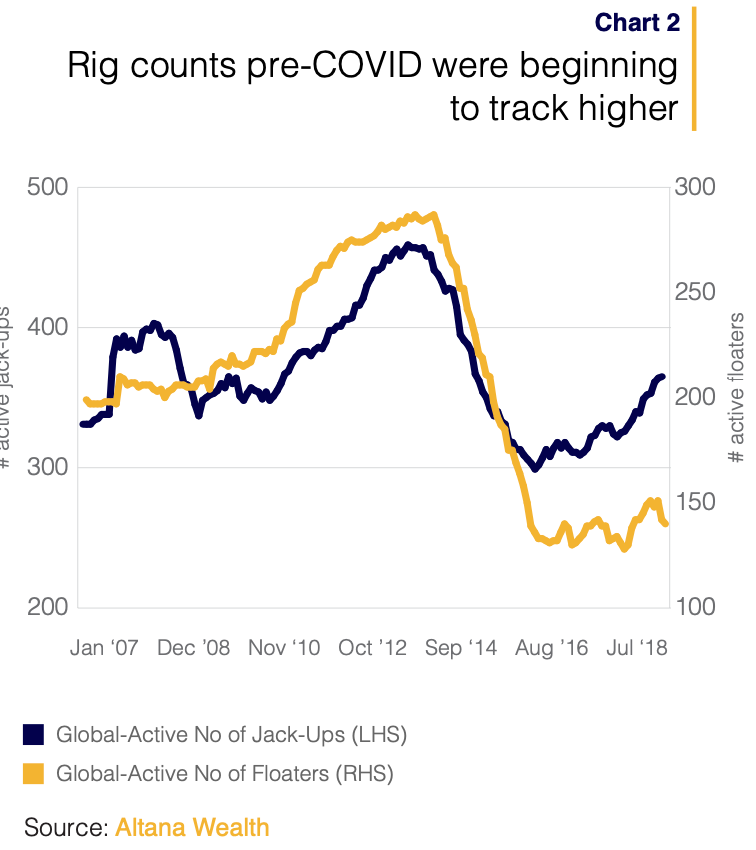

Our thesis was coming good as we started 2020. The majors were increasing their capex targets. Our belief that the lower-risk shallow water deposits would be prime production targets was panning out too, with the number of jack-ups (shallow-water drillers) which were active globally clearly trending higher, in contrast to the activity of floaters (mid-to-deep water drillers) which remained stagnant.

Saudi Aramco awarded a string of contracts to Shelf Drilling, the majority of which were for ten years (maturities not seen since the heydays of the offshore drilling boom).

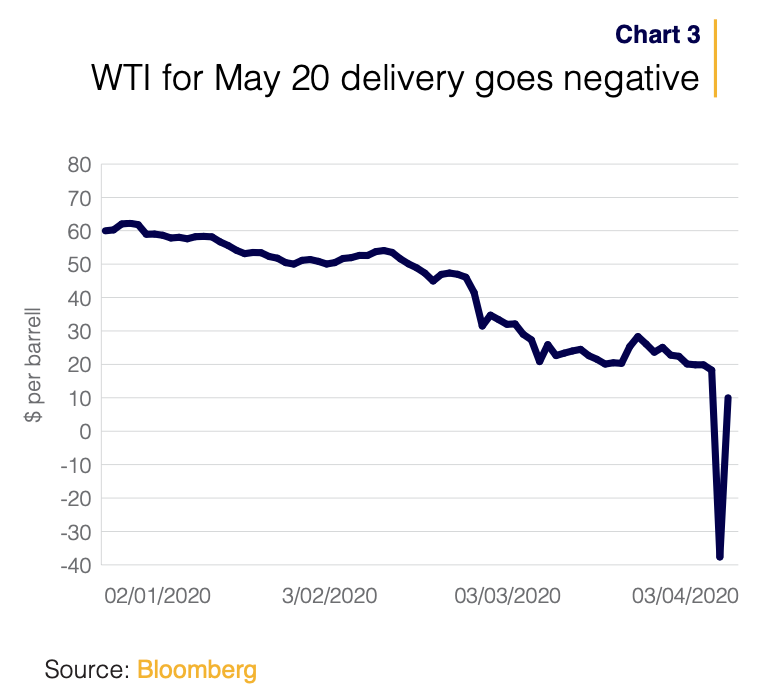

But then COVID hit, and the global lockdown led to a cessation of nearly all physical economic activity. There’s no need for us to expand upon just how ugly the macro data was during that time. Weekly US initial jobless claims rising by 244 standard deviations in the middle of March says it all. As far as the energy markets went, the collapse in world oil demand was more muted. The fall from 100 million barrels per day (mbd) to 80 mbd in the three months to April was only a 10 standard deviation event…

The world’s energy infrastructure wasn’t designed with such a sudden decline in demand in mind. The physical market was turned on its head as refineries turned away crude oil, as did storage facilities which had no capacity. Financial markets behaviour was even more chaotic with the WTI contract (which is for physical delivery) turning negative in case any of you had forgotten.

It seems as though the WTI-tracking ETFs which mechanically roll their futures at the end of each month weren’t paying attention, and as expiry approached, they were the only holders of the May contract.

It wasn’t so much panic selling by ETF funds that drove prices into negative territory (although it’s hard to imagine there wasn’t plenty of that too), it was that there were literally no buyers left in the market for that contract. It’s the most concise way we can think of for conveying how utterly chaotic those days were for everyone involved in the oil market. Despite the recovery from those lows, we can still see the effects of the trauma today.

The financial panic also reached boardroom level for the oil majors. According to Rystad Energy, 20 bn $ was cut from projected E&P capex by the majors, as the following chart shows. Activity in the jack-up and floater markets also tracked lower once more.

Crude prices expected in the medium term, as measured by the rolling sixty-month-out WTI contract, averaged 53 $ before COVID, but have averaged only 45 $ since. And if we look further out, at the rolling one-hundred-twenty-month out WTI contract (i.e. the market’s ten year expectation) prices have fallen by around 5 $ in the last few months. That’s only a few dollars higher than the March 2020 liquidity puke. The crude oil market’s verdict is clear: COVID has permanently impaired it.

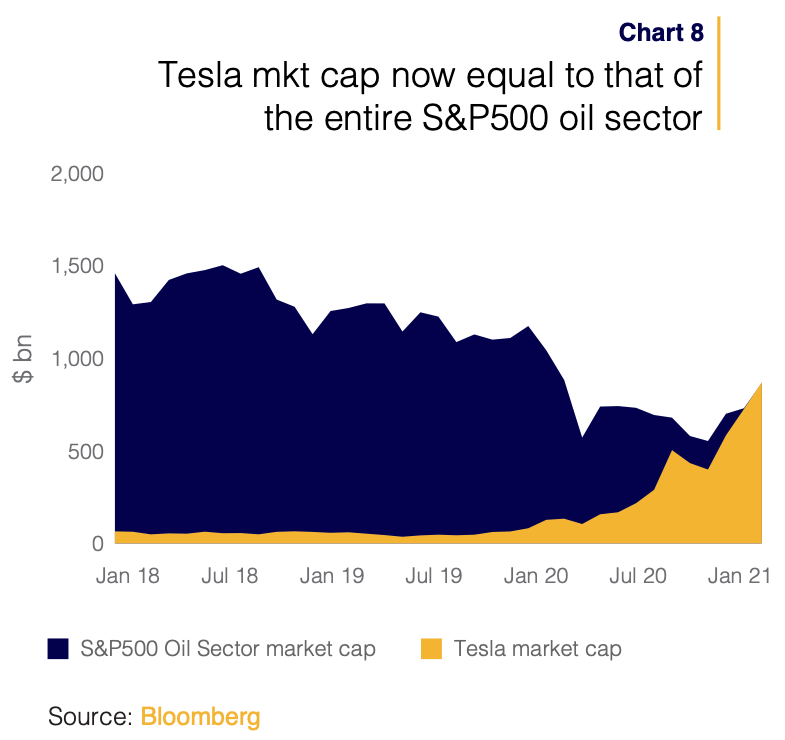

Meanwhile, the market capitalization of Tesla is today roughly the same size as that of the entire S&P 500 Oil sector, which includes the majors, the independents, the drillers, the service companies AND the refiners.

So the equity market’s view seems similarly equivocal: oil has no future, the energy transition is here.

Three reasons why the oil market has an investable future

Except that it isn’t. Or at least according to Bloomberg, which in its annual Electric Vehicle Outlook summary projects that Electric Vehicles (EVs) will only make up around 8% of the total fleet of passenger cars by 2030. Bloomberg expect the number of cars to rise from today’s 1.2 billion vehicles to 1.4 billion, but only for 110 m of them to be EVs. So the number of oil-consuming Internal Combustion Engine (ICE) vehicles on the road by then will still be around 1.3 bn, which is a forecast rise of around 0.7% per year.

Moreover, while passenger vehicles contribute around 60% of the global demand for crude oil, the rest comes from heavy duty vehicles, aviation and the petrochemicals industry for which there are as yet, few alternatives.

We’re not saying this is a good thing or that it’s something we’re especially happy about, but as investors our job is to allocate capital according to the way we think the world is, not the way we want it to be. And it’s obvious to us that the oil market will continue to play a central role in the global economy in the coming decades.

A second fact we think is important to understand is that the transition to EVs is a risk which is widely recognised and understood. BP has gone further than most in pivoting away from hydrocarbons, and very few oil executives are carrying on as normal, or are under any delusion about the reality of their industry.

The question isn’t whether or not oil demand peaks, the question is when. Project appraisals and capital allocation factor this in before sign-off. The general trend within the industry is very understandably that of moving towards a perfectly rational risk-aversion.

Lower-risk shorter-cycle projects, such as those we already mentioned, in shallow waters or in shale formations are clearly more attractive and easier to sign off on than those in deep waters, even if that’s where the largest deposits are ordinarily expected to be found.

Even the gunslingers of the shale patch seem to have gotten this memo. Scott Sheffield, CEO and co-founder of Pioneer Natural Resources, the largest owner of Spraberry acreage in the Permian, told attendees at a recent Goldman Sachs investor call that he didn’t expect much increase in Permian or wider US shale over the next several years, and that the Bakken and Eagle Ford shale regions might never see growth again. As for his own company, the message was clear: «I never anticipate growing above 5% under any conditions. Even if oil went to $100 a barrel and the world was short of supply».

The CEO of Devon echoed the sentiments, «I have a hard time seeing the need for U.S. producers over the next several years to get back to double-digit growth. For this management team, if we really think about 2021, let’s keep it flat.»

Which brings us neatly to the third point. Global production outside of shale oil has been flat since 2015. All incremental growth was driven by shale. Yet oddly enough, it’s still not quite clear how profitable that growth was. According to Deloitte, the shale industry registered net cumulative free cash flows of negative $300 billion since 2010, impaired more than 450 bn $ of invested capital, and saw more than 190 bankruptcies. Indeed, companies accounting for nearly 50% of shale output are so operationally and financially weak that Deloitte considers them «superfluous».

If Deloitte are right, and the shale patch’s newfound aversion to excessive risk sticks, global oil production may well surprise on the downside in coming years.

Arguably, the outlook is more bullish for oil today than it was pre-COVID. Regardless, the energy transition isn’t going away. Low-risk, short-cycle barrels will be in relatively higher demand, which argues not only for the higher quality shale assets, but the shallow water players. Which brings us back to where we started: shallow water services.

Shallow water drillers in the sweet spot

We don’t want to go into too much detail here. But since we discussed Tidewater in our original piece in December 2019, let’s consider it again. You may recall that having acquired Gulfmark it is now the largest listed Offshore Service Vessel (OSV) player and has been through a savage restructuring (G&A reduced by 45%, fleet reduced by 24%). It has an EV of around $500 million, of which net debt is $60 m, no maturities due until August 2022, and expects to generate free cashflow in 2020 of $42 m.

The combined EBITDA for Tidewater and Gulfmark in 2014 was $590 m, since then $60 m of cost synergies have been extracted. So call it $650 m peak EBITDA. If they can recover to just half of that, they’ll be at a normalized EBITDA of $325 m. Historically, their EV/EBITDA averaged 7x, but let’s assume that we’re wrong on the relative attractiveness of anything operating in shallow waters, and that anything oil can only expect to trade at a 50% discount compared to its former glories, given the perception that oil is now a permanently shrinking industry.

Let’s put that new EBITDA on an EV multiple of 3.5x. That implies an EV of $1.14 bn, which assuming a constant net debt of $60 m implies an equity value of just under $1.1 bn, compared to today’s $440 m. That’s around 2.4x. Of course, if we’re right about the attractiveness of shallow waters, EBITDA could surprise on the upside, and the market could reappraise its view on the sector’s longevity, which would translate into a significant rerating. It’s not difficult to see 4-8x returns here in the coming years.

And what happened to the supposed «smart money» which was buying in late 2019? Well, at the risk of stating the obvious, it shows that while skin-in-the-game might be important, it’s not a guarantee of success. Nevertheless, in an interview with CNBC in March of last year – during the teeth of the market rout – Sam Zell said he’d been adding to his energy holdings: «We think the energy space is really cheap … what helps is we were not in the energy space before.»2 John Fredriksen, who has been in the energy space before, remains fully committed, and has recently appointed Tor Andre Svelland to run his interests.

The smart money, it seems, is still invested.

* * *

Dylan Grice is co-founder of Calderwood Capital Research, an investment company specialising in portfolio construction and alternative investments.

Tyler Durden

Thu, 02/11/2021 – 21:10![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com