Futures Flat, Traders On Edge Ahead Of Critical CPI Print, 10Y Treasury Auction

U.S. equity futures and global markets drifted without direction on Wednesday as the rally in tech shares stalled and U.S. bond yields ticked higher ahead of a critical 10Y bond auction while investors nervously awaited a reading on inflation later in the day amid fears that the economy could potentially overheat. As Reuters puts it, “it all seemed a bit subdued” after Tuesday’s roaring 20% surge in electric car doyen Tesla, 4% jump in the Nasdaq and biggest one-day gain for global heavyweights Amazon and Microsoft in well over a month.

At 6:31 a.m. ET, Dow E-minis were up 110 points, or 0.34%, S&P 500 E-minis were up 3.50 points, or 0.09% and Nasdaq 100 E-minis were down 15 points, or 0.12% as Tesla dropped about 1.5%, while Apple Inc, Amazon.com Inc, Facebook Inc and Microsoft Corp fell between 0.2% and 0.7% in early trading. General Electric rose as much as 3.7% in pre-market trading after agreeing to combine its jet-leasing business with rival AerCap Holdings NV. The Nasdaq dipped after logging its best one-day percentage jump in four months on Tuesday, helped by a near 20% jump in Tesla shares as investors picked up momentum stocks that had recently taken a beating due to higher yields.

Mikhail Zverev, head of global equities at Aviva Investors, said Tuesday’s wild moves in big U.S. tech underscored how volatile markets, which are increasingly dominated by super-sized passive funds, are likely to be this year as the world tries to reset after the COVID-19 pandemic.

“The winds are blowing harder now. The world isn’t a more dangerous place, a mild increase in interest rates is not a cataclysmic event… but there is now the big-herd mentality with a greater propensity for rotations,” he said. “They are moving more frequently, they are moving faster and they are leaving a trail of inefficiency,” making markets vulnerable to big swings.

Shares of memo stock GameStop jumped another 13%, setting the videogame retailer on track for its longest streak of daily gains in six months and extending a rally that has already doubled the company’s market value. Among other “meme” stocks, Koss Corp and AMC Entertainment climbed 5.6% and 6.7%. A chunk of the $1.9 trillion relief aid, which is on track to be signed into law later this week, is poised to end up in the stock market and could provide a boost for GameStop and other stocks popular among retail investors active in online social media forums.

While Tuesday’s pullback in Treasury yields spurred a rush into stay-at-home winners, the rotation from growth to value shares looked set to resume on Wednesday according to Bloomberg. Congress is poised to send the $1.9 trillion Covid-19 relief plan to President Joe Biden for his signature, while vaccinations are picking up amid further signs of economic recovery. Upcoming consumer prices data in the U.S. are also expected to show a faster annual increase.

The Stoxx Europe 600 Index traded up 0.2% after being little changed for much of the session amid gains in energy and real estate shares. Adidas AG shares surged after the sportswear maker said it’s doubling down on e-commerce and sustainable materials, while Just Eat Takeaway.com NV climbed after announcing it expects a further acceleration of order growth in 2021.

Earlier in the session, Asian stocks rose for a second day, with equity benchmarks in China, Thailand and Indonesia leading the advance. Following the Nasdaq’s surge, the Chinext index of Chinese small caps rose, with Tesla battery-supplier CATL contributing the most to the gains after the 20% rally in Elon Musk’s automaker overnight. After recent successive declines, Wednesday marked a rebound for Chinese stocks, with the benchmark CSI 300 Index also climbing as much as 1.7% before paring gains. While a rout that erased $1.3 trillion from equity values in just 14 sessions was halted, traders warned the worst was not yet over. Markets in Singapore and South Korea lagged. Australia’s benchmark index also fell, erasing an earlier advance of 0.5%, as iron ore miners dropped

Japanese stocks closed higher, booking their first back-to-back gain in three weeks, as technology-related shares rebounded while value and cyclical names declined. Indexes see-sawed between gains and losses throughout the day. Electronics and telecommunications were the biggest boosts to Topix after the Nasdaq 100 saw its biggest rally since November and Treasury yields pulled back from recent highs. Retailers, service providers and automakers declined as the rotation trade that boosted Japanese stocks on Tuesday reversed. “Investors remain wary of the rising U.S. rates,” said Masashi Samizo, a senior market analyst at SMBC Trust Bank Ltd. “With the ECB upcoming and the BOJ and FOMC holding their monetary policy meetings next week, investors are in a wait-and-see mode to check how these central banks will deal with the current rate levels.” Fanuc was the largest contributor to gains in the Nikkei 225 following data that showed machine-tool orders for February rose by the most in two years.

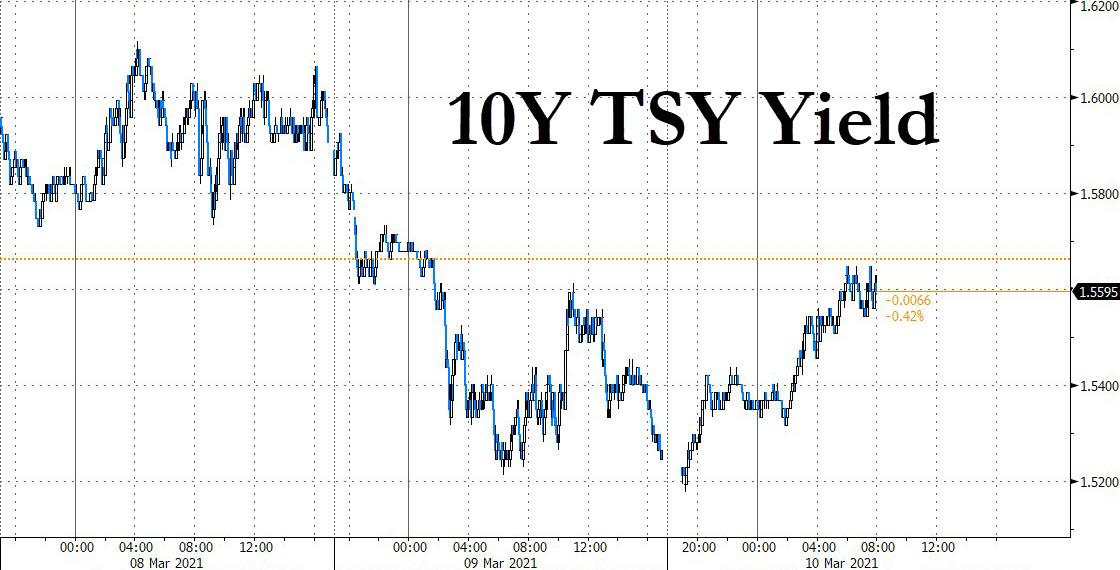

In rates, Treasury yields edged higher though remained below recent peaks as the first in a string of U.S. auctions went off without disrupting markets. Treasuries dipped after bear-steepening during London session, helped by a pair of block trades in 5-and 30-year futures at 6:20am ET. Yields were cheaper by 3bp-4bp at long-end of the curve, steepening 5s30s by more than 2.3bp, 2s10s by ~3bp; 10-year is cheaper by nearly 3bp at 1.554%, vs little-changed bunds and gilts. The selloff created a concession for Wednesday’s closely watched 10-year note auction at 1pm ET, with February CPI at 8:30am an interim risk. Treasury volumes were robust during Asian session. Ahead of $38b reopening, WI 10-year yield ~1.588% is higher than 10-year auction stops since February last year and ~43bp higher than last month’s.

“Although the bond market has steadied a bit, pressures will remain,” said Naokazu Koshimizu, senior rates strategist at Nomura Securities. “It has priced in future normalisation of the Fed’s monetary policy, the Fed’s policy becoming eventually neutral. But it has not yet priced in the chance of its policy becoming tighter.”

In FX, the Bloomberg Dollar Spot Index was little changed after erasing an Asia session advance, and the greenback advanced versus most of its Group-of-10 peers with the euro steady around $1.19. Haven currencies were among the worst G-10 performers while the Norwegian krone and the pound were among the best. The Canadian dollar was little changed before a Bank of Canada policy announcement, where it may provide clues around plans for pulling back stimulus from the nation’s surprisingly robust economy. Australia’s dollar fell to a day low in Asian trading as RBA Governor Philip Lowe said the central bank doesn’t share the market’s expectation for possible rate increases as early as late next year; the Aussie subsequently pared most of its losses in the European session. Gold steadied after posting the biggest jump in two months as the dollar ticked higher and bond yields held a decline.

Elsewhere, oil was steady as the dollar strengthened. Oil prices, which have surged 30% since the start of the year, steadied meanwhile as concerns over a supply disruption in Saudi Arabia eased. Brent crude futures recovered from an overnight wobble to sit at $67.45 per barrel, while U.S. crude futures hovered at $64.18 a barrel after a near 2 1/2-year high of $67.98 on Monday. Precious metal gold, which has suffered as bond yields have risen this year, eased 0.2% to $1,712 per ounce after rising more than 2% during Tuesday’s frantic session.

“There’s an element of corrective price action after a very spirited gold rebound,” DailyFX currency strategist Ilya Spivak said.

To the day ahead now, the calendar will be dominated by inflation released, with CPI data coming out of Denmark, Norway, Portugal and the US, with the latter also posting data on hourly earnings and the latest release of the treasury budget. France is due to report industrial production numbers. And the Bank of Canada will release its overnight rate target.

Markets Snapshot

- S&P 500 futures up 0.2% to 3,880.25

- SXXP Index up 0.2% to 421.12

- German 10Y yield little changed at -0.30%

- Euro little changed at $1.1896

- MXAP up 0.4% to 205.20

- MXAPJ up 0.4% to 685.55

- Nikkei little changed at 29,036.56

- Topix up 0.1% to 1,919.74

- Hang Seng Index up 0.5% to 28,907.52

- Shanghai Composite little changed at 3,357.74

- Sensex up 0.4% to 51,239.18

- Australia S&P/ASX 200 down 0.8% to 6,714.11

- Kospi down 0.6% to 2,958.12

- Brent futures up 0.1% to $67.56/bbl

- Gold spot down 0.1% to $1,714.31

- U.S. Dollar Index little changed at 92.03

Top Overnight News from Bloomberg

- European Central Bank officials are taking a leaf from former President Mario Draghi’s playbook as they ask if recent market moves amount to “unwarranted tightening” that requires action. That test, deployed by Christine Lagarde’s predecessor in 2014 in the run-up tonegative interest rates and quantitative easing, is relevant now as theeuro-zone economy lags behind the global recovery from the pandemic

- The rate that the Federal Reserve targets to control monetary policy is defying the skeptics by holding firmly above zero, prompting a rethink from those who thought the central bank might need to step in and tinker with the front end

- China’s producer prices rose at the fastest pace in more than two years in February, joining more expensive oil, computer chip shortages and soaring shipping costs as tailwinds for global inflation pressures

- The global economic recovery is fueling speculation that central banks will soon be shifting into tightening mode — nowhere more so than India

Here is a quick recap of global markets courtesy of Newsquawk

Asia-Pac markets traded with a slight positive bias following on from the gains on Wall Street where stocks were led higher by an aggressive resurgence in tech which lifted the Nasdaq 100 higher by over 4% for its largest gain since November and with the advances also facilitated by an easing of yields which led to a pause in the reflation trade. ASX 200 (-0.8%) and Nikkei 225 (+0.1%) both opened higher but then reversed most of the gains with the initial momentum in Australia offset by weakness in the commodity-related sectors and with financials mired as yields softened, while sentiment in Tokyo was tentative amid detrimental currency effects from the recent pullback in USD/JPY and with reports noting that Japan is to host the Olympics without overseas spectators although a decision has not yet been made and is anticipated later in the month. Hang Seng (+0.5%) and Shanghai Comp. (U/C) were kept afloat for the most part by strength in tech and with China Telecom shares surging at the open amid plans to list in Shanghai. However, the gains were briefly wiped out as participants digested inflation data which was firmer than expected but still showed CPI Y/Y in negative territory at -0.2% vs. exp. -0.4% and amid mixed US-China related headlines with US and Japan said to be considering condemning China for its ship intrusions, while other sources stated that China and the US are in talks for their top diplomats to meet in Alaska in a bid to reset their relationship. Finally, 10yr JGBs were rangebound amid the indecisive mood in Japanese stocks and lack of BoJ bond purchases in the market today, although eventually eked mild gains after support at the 151.00 level held overnight.

Top Asian News

- China’s Credit Better Than Forecast Despite February Holiday

- Japan Day Trader Arrested on Market Manipulation Charges: Report

- Taiwan Probe Spurs Fears of China Poaching Top Chip Talent

- Ant-Backed Bike-Sharing Firm Files Confidentially for U.S. IPO

Stocks in Europe are trading mostly positive (Euro Stoxx 50 +0.2%) after experiencing somewhat of a lacklustre open after the region took the wheel from a choppy/mixed APAC session. US equity futures meanwhile traded in the green before trimming the mild gains, with some outperformance in the more value-driven RTY and YM vs the tech-laden NQ, albeit the divergence is modest ahead of key risk events including US CPI and arguably the more-important US 10yr auction ahead of tomorrow’s ECB confab. Elsewhere on the fiscal front, the Senate’s USD 1.9tln COVID bill is expected to pass through the House today before landing on President Biden’s desk to be signed into law. Thus, some suggest this could translated to another bout of flows for some of the Reddit stocks in upcoming sessions. Back to Europe, UK’s FTSE 100 (Unch) resides as the laggard, albeit the index has narrowed the gap vs some of its EZ counterparts, albeit gains remain capped by Sterling dynamics. The index experienced a bout of weakness at the start amid losses across mining and oil names, albeit this has since been trimmed. Sectors in Europe are relatively mixed with no real biases, with consumer discretionary driving the gains amid earnings from Adidas (+5.8%) who resides as one of the top performers after stellar metrics and amid anticipation for revenue to increase in all market segments, with competitor Nike (+0.8%) modestly firmer pre-market. On the flip side, Tech and Materials are the laggards with the latter pressured by the slide in iron ore prices and the former taking a breather from yesterday’s firm performance, although source reports overnight also suggested that Apple (-0.2%) is planning to reduce its planned iPhone 12 mini amid weaker-than-expected demand. In terms of other moves, Spanish heavy-weight Inditex (-0.7%) is softer post earnings after missing analyst forecasts. Meanwhile, ABN AMRO (-3.0%) slid lower as it is poised to get relegated from the AEX (+0.1%) alongside Galapagos (-1.5%), and replaced with BE Semiconductor (+0.4%) and Signify (+0.5%) – with the changes effective from 22nd March.

Top European News

- U.K. Accuses EU of Harming Britons’ Health as Vaccine Row Grows

- Credit Suisse Temporarily Replaces Managers Tied to Frozen Funds

- Britain Set for Deals Boom With Firms ‘Very Cheap,’ Says L&G CEO

- Rothschild Financing Advisory Fees Rise to Mitigate M&A Dip

In FX, after Tuesday’s fall from grace, the Dollar seems to have settled down and looks content to bide time before US CPI and external events that could have an indirect impact, like the BoC policy meeting and ECB later today and Thursday respectively. Indeed, the index found underlying bids just shy of 92.000, at 91.967 vs yesterday’s 91.906 low and is now meandering either side of the new pivot level, with some external support from renewed weakness in certain major rivals that helped push the DXY up to 92.243 at one stage.

- AUD/CAD – The Aussie has pared some overnight losses, but is looking less assured above 0.7700 and 1.0750 vs its US and NZ counterparts amidst a sharp decline in iron ore prices and dovish commentary from RBA Governor Lowe who reaffirmed rate guidance and said that that the Board will decide whether to extend QE further later this year. Moreover, he categorically stated that market expectations for hikes next year and in 2023 are not in line with the Bank’s view of no tightening until at least 2024. Meanwhile, a different kind of double whammy for the Loonie as oil prices retreat further from recent heady heights (WTI not far from Usd 63/brl vs just 2 cents shy of Usd 68, and Brent Usd 66.50 compared to Usd 71.38 on Monday) and Usd/Cad pivots 1.2650 in cautious trade ahead of the aforementioned BoE confab – full preview in the Research Suite.

- CHF/JPY – No surprise to hear that SNB’s VC Zurbruegg is pleased with recent Franc depreciation, especially as the cost of curbing its strength over the last 12 months is estimated at Chf 100 bn. However, Usd/Chf reversed from circa 0.9375 through 0.9300 before basing again and Eur/Chf is straddling 1.1050 having topped 1.1100. Similarly, the Yen is maintaining recovery momentum around 108.70 falling through 109.00, but not to the extent to sustain gains beyond 108.50.

- GBP/EUR/NZD – Sterling is a marginal G10 performer, albeit unable to extend beyond 1.3900 vs Greenback far enough to test Tuesday’s best (1.3925) or the 21 DMA just above (1.3931 today), while also waning on approaches to 0.8550 against the Euro even though the single currency is finding 1.1900 tough to retrieve relative to the Buck in the run up to the ECB. Elsewhere, the Kiwi is hovering above 0.7150 vs its US peer pre-NZ FPI and post-RBNZ Governor Orr announcing that some coronavirus liquidity provisions will be withdrawn.

- SCANDI/EM – The Nok has weathered the latest pull-back in crude pretty well to keep its head above par vs the Sek and on an even keel with the Eur around 10.0800 on the back of firmer than forecast Norwegian headline inflation that offset a slightly softer than expected core. The Cnh and Cny are also gleaning some support from Chinese CPI, albeit y/y rate still sub-zero, while the Try has shrugged off a jump in Turkish unemployment amidst relief that imported oil costs have fallen quite sharply.

In commodities, WTI and Brent front month futures have nursed the pressure seen during APAC hours, which emanated from the significantly larger-than-expected and Texas-distorted build in Private Inventories (+12.8mln vs exp. +0.8mln), coupled with some questions as to whether the OPEC+ discipline will continue beyond April. Furthermore, the EIA STEO provided the complex with some downbeat omens after it cut 2021 world oil demand growth by 60k BPD but raised 2022 world oil demand growth by 330k BPD. However, prices since the European open have been climbing despite a distinct lack of news-flow, but more-so in tandem with the broader gains across stocks and the easing Buck. WTI now trades on either side of USD 64/bbl (vs low 63.13/bbl) whilst its Brent counterpart sees itself on either side of USD 67.50/bbl (vs low USD 66.50/bbl). Looking ahead, desks will be on the lookout for the US CPI metrics for some inflation/sentiment driven action, followed by the weekly EIA Inventories (Crude exp +0.816mln bbls), with further risk surrounding the US 10yr auction which could tap into traders’ future inflation expectations. Elsewhere, spot gold and silver are relatively uneventful within tight ranges around USD 1,715/oz and on either side of USD 26/oz awaiting direction from the aforementioned risk events. Over to base metals, LME copper advanced amid the more constructive risk tone coupled with a softer Buck. That being said, a Shanghai copper brokerage that accumulated bullish bets valued at over USD 1bln has reportedly cut its position by almost 25%. Finally, Dalian iron ore futures overnight sunk in a continuation of the downside seen after pollution-controlling measures were imposed on China’s largest steel-making city Tanghsan.

US Event Calendar

- 8:30am: Feb. CPI YoY, est. 1.7%, prior 1.4%; CPI Ex Food and Energy YoY, est. 1.4%, prior 1.4%;

- 8:30am: Feb. CPI MoM, est. 0.4%, prior 0.3%; CPI Ex Food and Energy MoM, est. 0.2%, prior 0%

- 8:30am: Feb. Real Avg Weekly Earnings YoY, prior 6.1%, revised 5.7%; Real Avg Hourly Earning YoY, prior 4.0%, revised 3.9%

- 2pm: Feb. Monthly Budget Statement, est. -$305b, prior – $235.3b

DB’s Jim Reid concludes the overnight wrap

You will be thinking I’m making this up but sadly I’m not. On Monday afternoon I popped downstairs to greet a very happy 5yr old after her first day back at school in 3 months. 3 hours later at dinner one of the twins (Jamie) had a temperature. By midnight my wife was on the phone to the hospital as his temperature was 40.5C and he had been sluggish all evening. They nearly came round as they were worried but after he rallied with Ibuprofen everyone agreed that he’d have a covid test yesterday which he duly took. Meanwhile the household has had to self isolate again and poor Maisie got only one day back at school. This is our sixth or seventh period of isolation or quarantine. I appreciate there are worse off people but this has been a bit of a dagger blow. Anyway, why didn’t I bring this news to you yesterday? Well I’m embarrassed to say I slept through it all and my wife had to deal with it and very kindly didn’t wake me up in the early hours of Tuesday morning. She was a zombie for most of yesterday. Fingers crossed we get a negative test result very soon and we can resume the slow crawl towards normality and Maisie can go back to see her friends. I believe the third Harry Potter film was devoured yesterday afternoon.

Even Dumbledore wouldn’t have been powerful enough to prevent the stunning tech comeback yesterday in yet another wild swing of a day. The Nasdaq (+3.69%) led the way after moving into correction territory the day before (was -10.5% from the peak by Monday close). Indeed, the NYSE FANG+ index of mega-cap tech companies rose even further (+6.42%) with Tesla (+19.64%) seeing its best day since February 3rd 2020. These two tech heavy indices saw their best days since November 4th (the day after the US elections) and April 6th 2020 respectively. It was a particularly great day for the stay-at-home trade that had been recently tossed aside with Zoom (+10.0%), DocuSign (+10.6%) and Peloton (+14.5%) all surging. The S&P 500 added +1.42% even if small-cap stocks outperformed, with the Russell 2000 up +1.91%. So a good day for both big and small and not such a good day for quite big. Indeed there was clearly a break from the recent rotation trade as Energy (-1.91%) and Bank (-1.70) stocks fell back in favour of tech industries such as Semiconductors (+6.14%) and Tech Hardware (+3.32%).

In Europe, the Stoxx 600 jumped (+0.76%) to its highest levels since mid-February last year, and now nearly erasing all of the pandemic-related slump. The European index saw nearly two-thirds of its constituents rise yesterday with similar sector leaders as seen in the US. Technology (+2.52%) and Retail (+2.34%) were the main drivers of the rally, while Travel and Leisure rose (+1.96%) on the back of news that the EU will propose “passports” for those who have taken EU-approved vaccines in order to instill more confidence in regional travel.

Even as risk assets surged many market observers kept their eyes firmly on global bond yields, which fell back as the first tranche of this week’s $120 billion of US supply was sold yesterday. A $58 billion auction of 3y notes went fairly smoothly. There more attention on the auction of $38bn of 10yr bonds taking place today, and the $24bn of 30y bonds coming tomorrow. US Treasuries led the global bond rally yesterday with 10yr yields finishing -6.4bps lower at 1.526%. This was the first drop in yields in 5 sessions and the second biggest one day drop in 10yr yields since late-January. The move was driven by a pullback in real rates (-7.2bps) rather than a change of inflation expectations (+0.8bps). Across the Atlantic, European core rates mirrored their US counterparts with UK gilts (-2.7bps) and German bunds (-2.4bps) both seeing moderately lower yields.

Inflation expectations in general have a been a partial driver of the 10yr recently and later we will get the February CPI data showing how consumer prices have evolved of late. Our US economists expect a repeat of the January release with energy prices propping up the headline figure but with a relatively soft core print. One risk to the release could be the inclement weather last month, which has the potential to induce some volatility into the print, particularly with respect to energy. The market continues to expect a +0.4% (+0.3% last month) rise in month-over-month prices.

To be honest the more important inflation prints are still some months away, once fuller reopening activity and stimulus cheques have passed through the system. On the government support, President Biden’s coronavirus relief package is expected to be approved today following a final vote by the House of Representatives, and then the bill known as the American Rescue Plan will make its way to Biden’s desk to be signed into law as early as tonight. Some Congressional Democrats are already looking past the bill to the upcoming infrastructure negotiations, though a White House advisor has said he expects it to be more bipartisan.

Overnight in Asia, markets are mostly trading lower outside of China and Hong Kong where the CSI (+0.95%), Shanghai Comp (+0.26%), Shenzhen Comp (+0.67%) and Hang Seng (+0.12%) are all up after yesterday’s intervention by state funds. Meanwhile, the Nikkei (-0.09%), Kospi (-0.69%) and Asx (-0.84%) are all down. Futures on the S&P 500 (-0.34%) are also down. Sentiment is being weighed down this morning by the higher than expected Chinese February PPI, which came in at +1.7% yoy (vs. 1.5% yoy expected), the highest gain in over two years while CPI came in at -0.2% yoy (vs. -0.3% yoy expected). The resurgence in Chinese PPI is leading to some concerns that it will likely add to inflationary pressures this year as Chinese factories start passing the increases to global customers. Meanwhile, yields on 10yr USTs are trading up +1bps and those on Australia (-7.0bps ) and New Zealand (-7.1bps) 10 years are down following yesterday’s decline in global yields. In Fx, the Australian dollar is down -0.44%% after we saw a pushback from the RBA governor over the market pricing of rate hikes. He said that markets may be getting ahead of themselves by pricing in an interest-rate increase within the next couple of years. The US dollar index is up +0.25%. Elsewhere, Brent crude oil prices are down -0.99%.

For those interested in the topic of ‘greenwashing’, under a suite of new EU finance rules due to be rolled out in stages and beginning on March 10, firms including fund houses, insurers and pension funds that provide financial products or services in the European Union will have to begin disclosing how sustainable they really are. The new EU legislation is called the Sustainable Finance Disclosure Regulation (SFDR) and it aims to iron out the patchy climate-related information currently provided by financial market participants, as well as give firms with genuinely sustainable products an edge. Set to roll out in stages over the next two years, SFDR contains reporting obligations at both the company and product level. But from this week, all funds must disclose in their pre-contractual information how they factor sustainability risks into their investment decisions. Additionally, those funds promoting environmental or social characteristics, or sustainability objectives, must explain both in their marketing and on their websites the objectives and how they plan to meet them.

Just on this a paper published overnight by Greenpeace and the New Economics Foundation has urged the ECB to stop lending against brown bonds, arguing that marginal changes taking into account climate risks won’t sufficiently lower the institution’s carbon footprint.

Staying on the sustainability subject, e-commerce firm Shopify said yesterday it will become the first customer to buy contract carbon removal units from Canada-based direct air capture company Carbon Engineering to slash its greenhouse gas emissions. Shopify bought 10,000 units, or one metric tonne of carbon dioxide captured and permanently removed from the atmosphere, from the firm’s future direct air capture (DAC) projects. Carbon Engineering has been running a pilot facility at the foot of British Columbia’ Coast Mountains to suck a ton of carbon dioxide a day out of the sky and convert it to fuels, in a bid to show that the planet can put emissions into reverse. It’ll be fascinating to see whether this is ever scaleable.

In terms of the latest on the pandemic, Johnson & Johnson told the European Union it is facing supply issues that may complicate plans to deliver 55m doses of its covid vaccine to the bloc in the second quarter of the year, reports indicated. J&J’s vaccine, which requires only one dose for protection, is expected to be approved on March 11 for use in the EU by the bloc’s regulator. EU officials have said deliveries could start in April. Meanwhile, China has launched a digital COVID-19 vaccination certificate for its citizens planning cross-border travels, as the pace of coronavirus global vaccinations has accelerated. There was somewhat positive news on the variant front, as the Pfizer vaccine was shown to neutralize the UK, Brazil and South African strains in lab experiments.

The OECD released their new outlook yesterday. The report forecast a better outlook for global growth on the back of President Biden’s $1.9tn US stimulus programme. The global economy will expand by 5.6% this year, an upgrade of 1.4 percentage points from November. The OECD substantially revised up its expectations for US growth this year, to 6.5% from 3.2%. It also revised upwards its forecast for the UK for both 2021 and 2022 by 0.9 and 0.6 percentage points respectively as a result of its successful vaccination programme. In Europe, however, the recovery is expected to be slower, as the positive effects of the stimulus will be partly offset by the lag in vaccination programmes, which will delay the loosening of coronavirus restrictions and generate a longer hangover from the crisis, the OECD said.

Looking at yesterday’s data, Germany’s exports rose 1.4% mom in January, higher than the prior 0.4% increase, while country’s trade balance rose to €22.2b. Italian industrial production increased 1% mom in January. Meanwhile, eurozone final 4Q GDP was revised down to -0.70% from -0.60% on a quarterly basis, but yoy the 4Q GDP number was revised upwards at -4.9% compared with the previous -5.0% mark. Eurozone exports rose 3.5% qoq in 4Q.

To the day ahead now, the calendar will be dominated by inflation released, with CPI data coming out of Denmark, Norway, Portugal and the US, with the latter also posting data on hourly earnings and the latest release of the treasury budget. France is due to report industrial production numbers. And the Bank of Canada will release its overnight rate target.

Tyler Durden

Wed, 03/10/2021 – 08:05![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com