“No Panic”: Markets Surge As “Transitory Inflation” Narrative Reasserts Itself

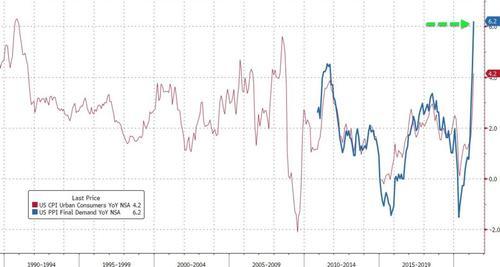

It seems that the “non-transitory” inflation panic that gripped markets yesterday, resulting in the biggest one-day drop in the S&P since February, is gradually transitioning to “transitory” again, and even though today’s y/y PPI print of 6.2%, the highest on record, reaffirmed the soaring prices narrative…

… today the “transitory” inflation mood is reasserting itself, with Emini futures surging almost 100 points from the overnight lows…

… and the battered FAAMG sector is solidly in the green as closely watched 5Y breakevens slide and nominals are down to session lows:

Wall Street traders also find comfort in the latest hot take from Morgan Stanley’s QDS desk which notes that the the trading desk noted “there was no major panic outside the systematic community as the ‘transitory inflation’ narrative appeared to be adopted” and furthermore, “the desk continues to see demand in mega cap tech from the longer term community for the third day in a row.”

Optimism was also fanned by market commentary from JPMorgan which almost verbatim echoed what we said yesterday…

Remember, Fed is focused on jobs, not inflation which is “transitory”

This does not change delayed tapering

— zerohedge (@zerohedge) May 12, 2021

… and overnight wrote that despite the blistering hot CPI and now PPI, nothing has changed “from the Fed’s view. The Fed is focused on the labor market, believing that any transitory inflation can be weathered by Consumers.” Some more from JPM:

What is the Fed looking at (BLS)? US Market Intelligence thinks it is a combination of the unemployed (9.8mm; 6.1%), long-term unemployed (4.2mm, +3.1mm from Feb 2020), labor force participation rate (61.7%; -1.6% from Feb 2020), employment-population ratio (57.9%; -3.2% from Feb 2020), number of people not in labor force who want a job (6.6mm; +1.6mm from Feb 2020), and a new category “unable to work because their employer closed or lost business due to the pandemic” (9.4mm, down 2mm MoM, but this did not exist prior to Feb 2020; and, not all of these people are counted in unemployment measure). Finally, you have people “prevented from looking for work due to the pandemic” numbering 2.8mm which is -900k MoM; none of these people are counted in the unemployment measure.

Combine these numbers and you see a US labor market that is more fragile than headline numbers suggest. This may be why we continue to see Fed speakers reiterate a data-driven approach. Conversely, this may also be why markets are now seemingly more sensitive to inflation. Commodity-based and COVIDinduced supply chain inflation may overlap with wage inflation, creating a situation where the Fed may have to act more strongly than what investors have witnessed previously.

For those asking “how to monetize this line of thinking” JPM recommends commodities and commodity-linked Equities, specifically Energy: “consider both integrates like XOM and CVX, or XLE for general exposure. Further, refiners are a strong long play through 2021Q3, potentially longer, and would view VLO and MPC as the favored ways to play. In addition to that, inflation expectations are likely to pull yields higher, which benefit Banks.”

Tyler Durden

Thu, 05/13/2021 – 10:35![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com