The QE Endgame: A Big Problem Is Emerging For The Fed

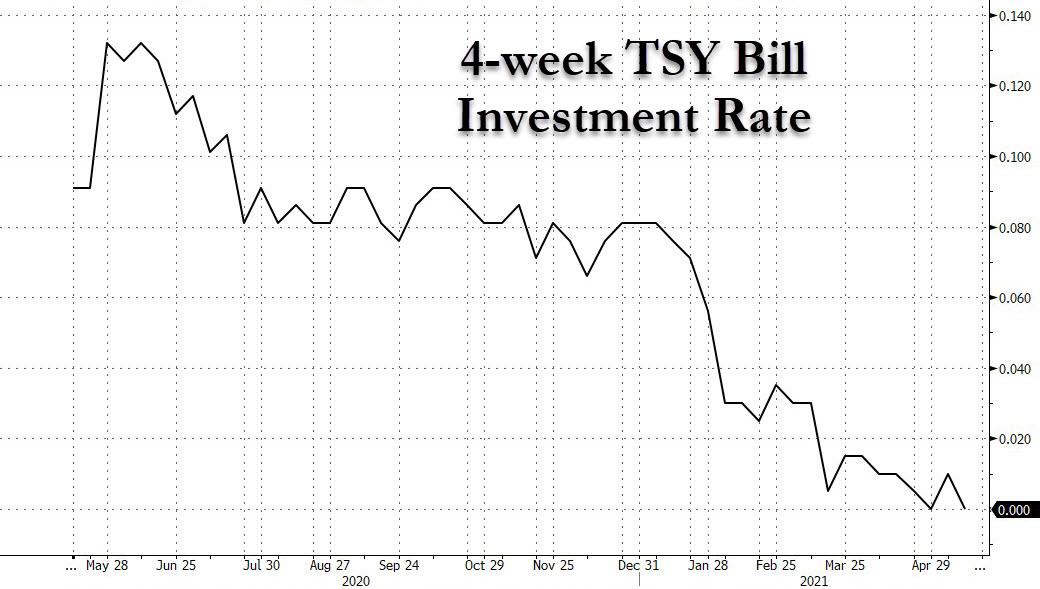

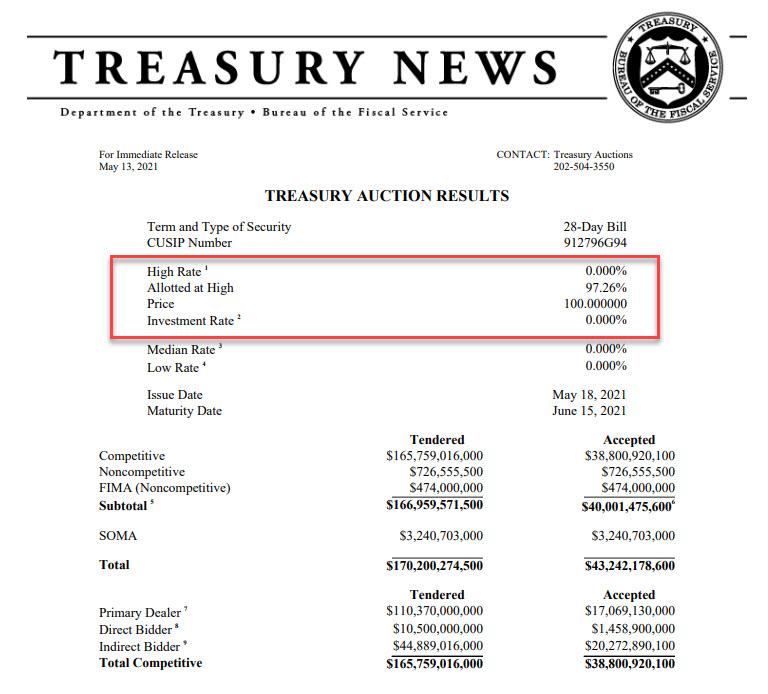

For the second time in three weeks, the US Treasury sold $40BN in 4-week bills at a price of 100.000% representing a rate of 0.00%.

To be sure, Bills had printed at 0.000% at auction previously, but that was largely during the reserve glut days of 2015.

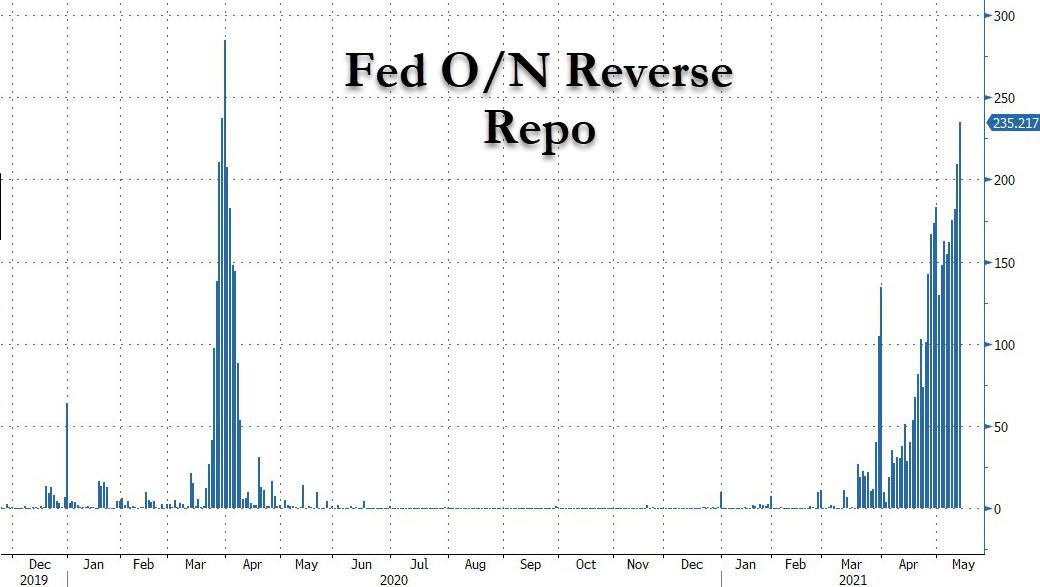

So why now? The same reason usage of the Fed’s Reverse Repo facility has soared in recent weeks from zero to over $100 billion at the end of April, hitting a whopping $235 billion today…

…as investors choose to directly transact with the Fed – where only positive rates are allowed – rather than the open market where collateral rates have frequently been negative in recent weeks as Curvature’s Scott Skyrm explained in this note from April 26:

Overnight rates are low. Too low by all normal standards. The fed funds rate is well below the mid-point of the fed funds target range and the Repo GC rate is at zero; often trading negative. Zero percent interest rates are forcing billions of dollars of cash into the Fed’s RRP facility.

While this This is a delightful case of deja vu irony – the Fed is taking Treasurys out of the market through QE purchases and putting them right back in via the RRP – it is also distorting the Repo market, and although the Fed can fix this aberration by hiking the IOER or RRP rates, it has so far refused to do so.

But the ongoing surge in reverse repo usage masks a far bigger problem in store for the Fed, and it’s why Curvature’s Skyrm writes that “now is a pretty good time to start talking about the size of the SOMA portfolio, even if some people don’t want to talk about it.”

Why is the surge in reverse repo linked to tapering? Skyrm explains, by posting a rhetorical question:

“What are the next steps for tapering purchases and what will the SOMA portfolio look like when we’re done? What will the market look like?”

The repo strategist then reminds us that even when the Fed starts tapering, the Fed balance sheet will continue to grow indefinitely, if at a slower pace, flooding the system with the same reserves that are now desperate to buy Bills at 0.000% or be parked at the Fed (for 0.000%).

Talk of tapering feels like when you’re getting ready for a dinner out. You’re ready and it’s time to go. You check on your spouse and they haven’t even started getting ready yet! As of last week, the SOMA portfolio stood at $7.185 trillion and the Fed continues purchases at $120 billion a month. If and when tapering starts, the purchases won’t go from $120 billion to zero in one announcement. The purchases will gradually slow – going from $120 billion, to maybe $100 billion, to maybe $80 billion, to $50 billion, to $20 billion.

Let’s look at some rough estimates. Assuming the Fed tapers at this schedule at each FOMC meeting beginning in June, that would mean the Fed adds about another $350 billion and ends QE in November. That’s the most aggressive tapering schedule. Let’s assume the Fed doesn’t begin tapering until the end of the year. That means, roughly, another $900 billion will be added to the SOMA portfolio.

This is a problem, and Skyrm explains why: Even today there’s barely enough collateral in the Repo market right now to cover all of the cash being invested. If volume at the RRP shot up to $235 billion today, what’s going to happen when there’s $350 billion fewer securities in the market at the end of the year?

How about if it’s $900 billion?

In short, we already have a collateral shortage the likes of which are on par with what we experienced in 2015-2016. What happens in the next 18 months when we get an additional $1 trillion in reserves sloshing around?

Tyler Durden

Thu, 05/13/2021 – 19:45![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com