“The Correlation Is Broken”: JPMorgan Tells Clients To Buy Puts In These Tech Stocks

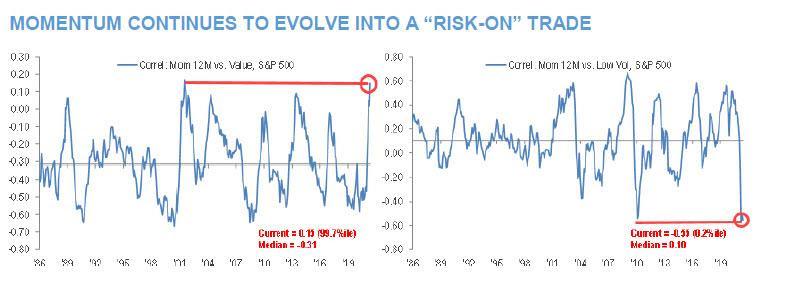

Last week, ahead of the massive Momentum ETF (MTUM) rebalance, we showed something remarkable: momentum stocks had undergone a complete Dr Jekyll to Mr Hyde transformation, and instead of correlating to growth, momentum was now purely a “risk on”, or value trade…

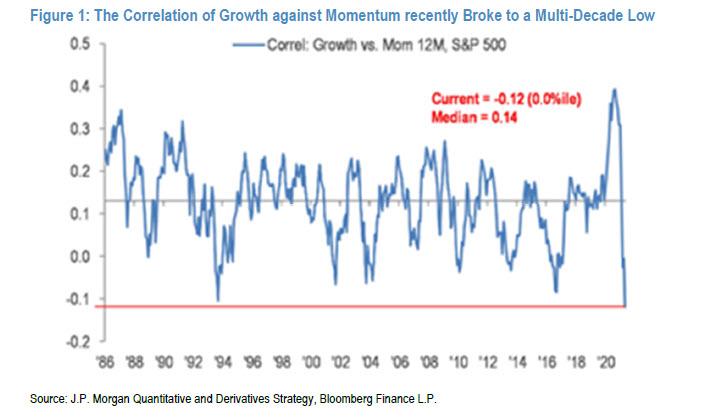

… which could be best seen in the collapse of growth-to-momentum correlation.

Needless to say, this transformation made life for analysts – who are really just glorified momentum chasers with some sophisticated-sounding narrative overlay – challenging, because after years of pitching momentum growth names, they now had to shift to value stocks as their preferred reco.

Nowhere was this more evident than in a research note from JPMorgan itself, which despite being the most bullish bank on Wall Street (certainly not to be confused with Morgan Stanley, whose chief equity strategist Mike Wilson yesterday said a 10-15% drop is coming in the next few months), is now taking a step back from its WallStreetBets-like enthhusiasm for risk, and telling clients to “Buy Puts in Tech Stocks Triggering Negative Momentum Signals“:

In the note, JPM quant strategist Shawn Quigg points to the chart of collapsing growth-to-momentum correlations shown above (and first discussed last week), and says that “the correlation of Growth and Momentum is broken, driven by a swift market re-allocation towards Value amid a view the economic reopening will drive inflation and interest rates higher, headwinds for stocks that benefit in deflationary environments such as Technology.”

To be sure, despite the recent rebound in the QQQs, JPM expects these headwinds to persist as the bank’s economists anticipate peak inflation occurring in April (last Friday’s PCE release). However, according to Quigg it will take until late June (e.g., May release), or later, to confirm the peak.

Here things get awkward within JPM itself, because while one quant strategist says to buy tech puts, the bank’s equity strategist is still overweight tech. How does Quigg resolve this apparent contradiction? Here’s how:

“While our U.S. equity strategist remains Overweight Technology, downside risks could remain for those stocks triggering negative momentum signals despite the NASDAQ 100 in a recent upswing.”

In other words, the bank argues that while tech stocks will still keep rising over the long run, they will drop in the short-term, as “momentum is broken”, and so having puts on is a way to capitalize on this drop. Why that is not sufficient to at least prompt a downgrade from Overweight to Neutral remains a very open question.

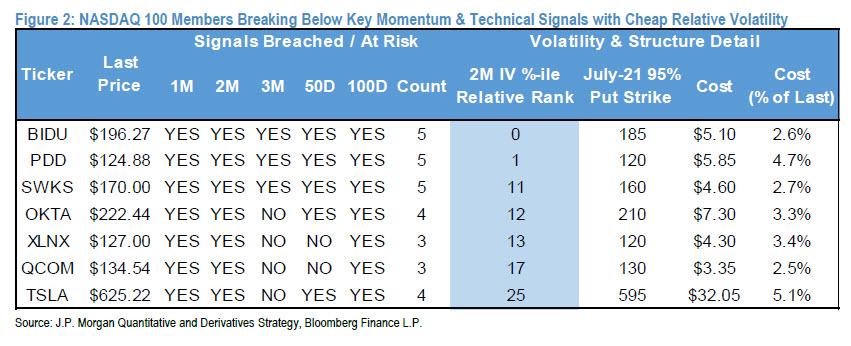

Anyway, back to Quigg who then says that he screens the NASDAQ 100 for stocks that are breaking, or are poised to break, below key momentum / technical signals that also carry cheap implied volatility for tactical trade ideas. He details the process below:

We use five short to intermediate term momentum and technical signals popular with quantitative investors (i.e., 1M, 2M, 3M momentum signals, and the 50d and 100d moving averages). We include only those option liquid (10M notional option volume over a 20d period) members of the NASDAQ 100 that are breaking, or are within +/-2.5% (beta adj.) of breaking, below three to five of these signals. We additionally screen for those stocks with cheap volatility via 2M implied volatility that ranks within the bottom quartile (i.e., 25th %-ile rank or lower) relative to the QQQ. Broadly, we find that nearly 30% of the QQQ are breaking, or are poised to break, three to five of these key technical levels. Comparatively, we are not witnessing nearly the same degree of technical breakage in the S&P 500 where only 15% are breaking below three to five of these technical levels, of which 42% of those are within the Information Technology and Communication Services sectors.

His advise: purchase July 95% strike puts on BIDU, PDD, SWKS, QCOM, OKTA, XLNX and/or TSLA, and visually:

Tyler Durden

Wed, 06/02/2021 – 14:01![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com