WTI Tumbles After OPEC+ Meeting Ends In No Agreement, Postponed To Tomorrow

Update (1400ET): Two hours ago it looked like they were close to a deal. Now, as Bloomberg reports, there is talk of delaying the full ministerial meeting until Friday, or even later. As prices have risen along with oil demand, the incentives to stick together have weakened and the rifts are widening.

the delay in the talks reveals the deep disagreements within OPEC+. Saudi Arabia, in particular, but also Russia have worked quite hard to present a unified front and reassure the market they are in control. The repeated last-minute clashes undermine the credibility of the cartel.

And that uncertainty has sent crude prices lower…

The JMMC will reconvene at 3 p.m. Vienna time tomorrow, a delegate says.

Recognition of the big increase in the UAE’s production capacity from the level used as its baseline will have to be dealt with at some point, or this dispute will continue to undermine OPEC+ unity. The UAE may now be regretting that it accepted such a low baseline in the original deal. Others may also regret that it wasn’t given a higher starting point for its cuts.

* * *

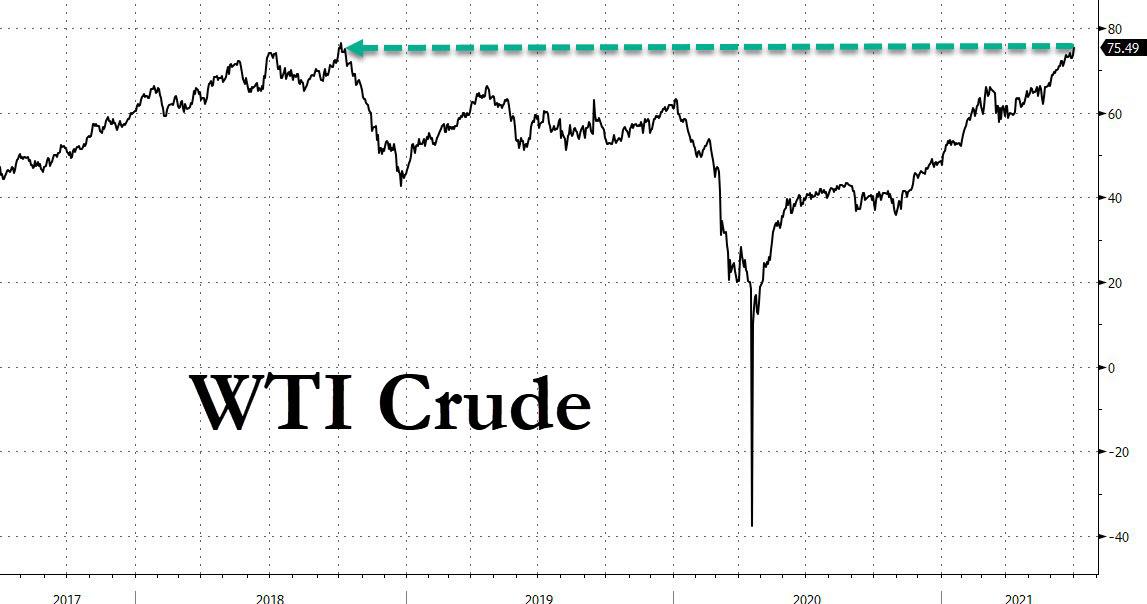

Brace for shock at the pump. WTI crude prices surged by over $2, rising more than 3% to $75.8/bbl…

… the highest since 2018…

… amid reports that ahead of the conclusion of today’s OPEC, JMMC and OPEC+ meetings, Saudi Arabia and Russia have agreed on a preliminary deal regarding raising oil output, one which will include a monthly oil output increase of less than 500k bpd to OPEC’s current holdback of 5.8 million barrels until December-2021, which is less than the market consensus of 500kbp/d. Reuters adds that OPEC+ is also likely to ease oil output cuts by 2 million bpd between August and December, which suggest that OPEC+ is weighing inflation risks in the short-term, however by year-end the market is expected to be in a deficit of over 3mmb/d, which is why most banks have projected oil to rise above $85 toward the end of the second half.

Additionally, local sources add that OPEC+ is currently debating extending the production deal to the end of 2022 (from the original April 2022), according to a delegate, which will lead to the further supply constraints and even higher prices.

While OPEC+ intentions should hardly be a surprise to the market, the fact that oil prices are only now spiking shows how far behind the curve algos and CTAs have been. Or as energy expert Art Berman puts it, “So much commentary about how OPEC doesn’t matter any more yet today so many tweets expressing frustration with OPEC for not increasing supply.”

So much commentary about how OPEC doesn’t matter any more yet today so many tweets expressing frustration with OPEC for not increasing supply.

Both narratives cannot be right. Which is it?

— Art Berman (@aeberman12) July 1, 2021

The OPEC+ meeting is happening against a backdrop of tightening supply. Crude inventories in the U.S. are falling at the fastest rate in decades, while shale producers are remaining disciplined with their spending and won’t overwhelm OPEC, ConocoPhillips Chief Executive Officer Ryan Lance said on Wednesday. In another bullish sign, TotalEnergies SE, one of Europe’s biggest refiners, bid for benchmark Forties crude at the highest premiums in 17 months.

“We absolutely think prices are going to continue to rally, especially if OPEC adds anything up to 500,000 barrels per day,” Amrita Sen, chief oil analyst at consultant Energy Aspects, said in a Bloomberg Television interview. “It’s a drop in the ocean.”

“Anything less than a 500,000-barrel-a-day supply increase in August will be enough to see the bulls push the market higher,” said Warren Patterson, head of commodities strategy at ING Group in Singapore. “While there are concerns over rising cases of the delta variant in some regions, the market is doing a good job at ignoring it for now.”

The market agrees: not only are spot prices surging, but WTI prompt backwardation surged, with the nearest timespread touching $1 a barrel intraday, rising as much as 30c, the strongest since September 2019, and trading at 86c as of 7:33am New York time, an indication the market sees supply deficits extending for a long time.

Some secondary details ahead of the completion of today’s OPEC+ meeting expects non-OPEC members Kazakhstan, Oman, Brunei to compensate 490k BPD until the end of September. So far, Russia has not offered any plans for compensation. Among the OPEC members, Iraq, Guinea and Gabon are expected to compensate a total of 960k BPD.

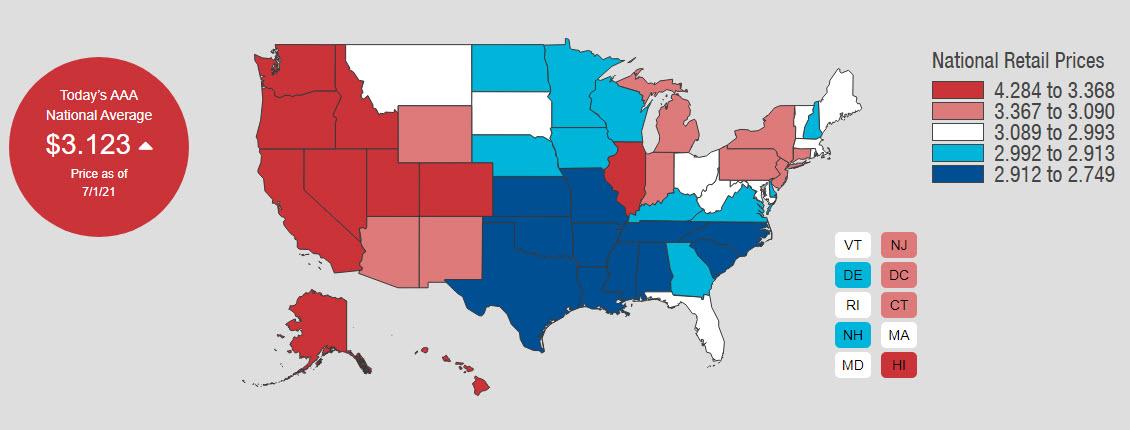

And while the surging oil prices is great news for the likes of the world’s biggest oil producer Russia, and Vladimir Putin, it may not be so great for US consumers as the average US gas price is set to rapidly approach $4.

Tyler Durden

Thu, 07/01/2021 – 14:07![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com