Goldman Has Three Questions For Companies During Q2 Earnings Season

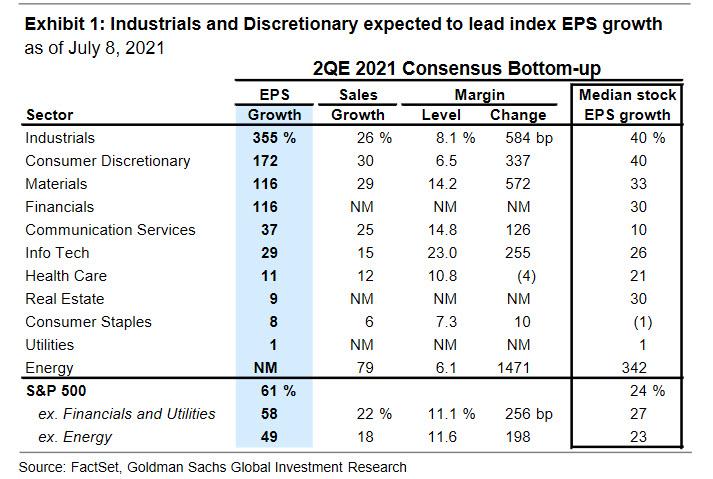

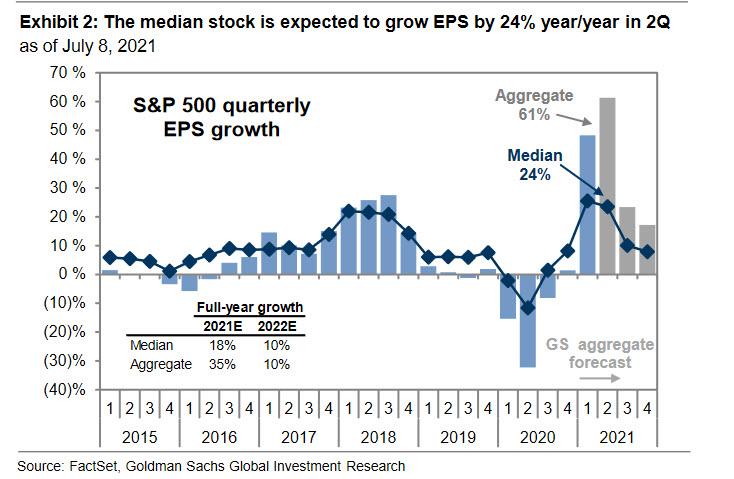

2Q earnings season kicks off next week when the big banks kick off reporting as usual, and consensus expects 2Q EPS growth of 61% year/year, driven by a combination of base effect, 22% sales growth and 256 bps of net margin expansion to 11.1% even though the median stock is forecast to grow EPS by a more modest 24%. Compare this to one year ago, when S&P 500 EPS fell by 32% as the pandemic sparked a sharp recession. Cyclical Industrials, Consumer Discretionary, and Materials sectors are forecast to lead the index in EPS growth.

In 2Q 2020, Brent crude traded at an average of $33/bbl and Energy stocks posted an aggregate net loss. Oil prices averaged $69/bblin 2Q and Energy firms are expected to return to profitability.

Like last quarter, Financials are expected to be the primary driver of S&P 500 EPS growth. In 1Q, Financials represented $3 of the total $9 EPS beat versus consensus expectations. Financials EPS are forecast to grow by 116% in 2Q and account for 25% of S&P 500 EPS growth. Most banks analysts expect results to come in largely in line with consensus after adjusting for reserve releases. Capital markets activity has normalized following the strong pace in 2020 and 1Q 2021. However, large reserve releases will boost EPS for the third quarter in a row and could drive up to 18% EPS uplift for Banks by year-end. Though investors are not likely to reward these beats outright since releases are non-recurring, analysts expect that the market will pay for the capital return that could result from the earnings tailwind and the recent CCAR results.

Another notable point: while consensus expects S&P 500 EPS to grow by 61%, the median stock is only forecast to grow earnings by 24%.

The greater rebound in aggregate earnings is largely a function of the base effect, or the sharper decline in earnings in 2020; the median S&P 500 stock saw its EPS fall by just 12% year/year in 2Q 2020 compared with the 32% decline in aggregate earnings. The five largest stocks in the index (FB, AMZN, AAPL, MSFT, GOOGL) account for 22% of market cap and 14% of S&P 500 2Q 2021 EPS. Despite last year’s acute 2Q economic contraction, these firms actually posted average EPS growth of 38% and are still expected to grow earnings by an average of 52% in 2Q 2021.

In his preview of Q2 earnings season, Goldman’s chief equity strategist David Kostin – who expects the S&P to close the year at 4,300 or -0.5% lower from Friday’s record close – focuses on three questions for managements this earnings season:

- How will firms preserve profit margins amid input cost pressures?

- How will companies prioritize their cash spending as balance sheets recover?

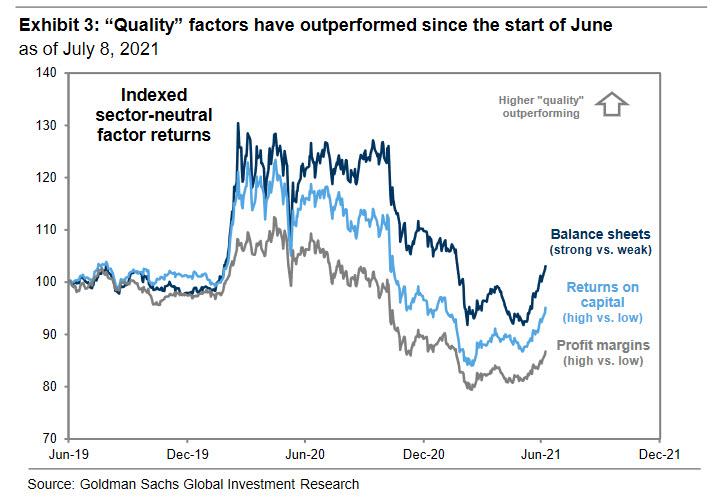

- How does ongoing policy uncertainty affect the business outlook? Rates have plunged and high “quality” themes are outperforming.

Digging a little deeper

- 1. How will companies preserve margins amid input cost pressures? S&P 500 margins notched a record high of 11.9% in 1Q 2021, though investors remain focused on the forward margin outlook given rising input costs. Global shipping woes, raw material inflation as well as acute shortages in both labor and semiconductors have combined to increase costs for companies across the by raising prices and passing higher input costs to their customers. During Q1 calls, many companies discussed price increases and this trend will likely continue during 2Q earnings. Alternatively, with SG&A as a share of sales elevated versus history, companies can also preserve margins through cost cutting. As an example, General Mills announced last week that it faces some of the highest costs in a decade and will implement a mix of both cost cuts and price increases.

- 2. Investors have started to reward companies with attractive margin profiles. According to Goldman, profit margins are the second most important driver of company valuations today, behind only equity duration. The bank’s sector-neutral factor of stocks with the highest vs. lowest profit margins has also started to outperform. Other “quality” factors such as strong vs. weak balance sheets and high vs. low returns on capital have also inflected higher since early June.

- 3. How will companies prioritize their cash spending as balance sheets recover? Both aggregate and median S&P 500 cash / assets ratios have rebounded and now stand at record levels, driven in part by record high corporate bond and follow-on equity issuance during the last 18 months. And while leverage remains elevated versus history, it has been falling as corporate profits have started to improve. Info Tech and Consumer Discretionary hold the highest cash / asset ratios of any sectors and account for 43% of total S&P 500 ex-Financials cash.

For what it’s worth, Goldman expects capex will represent the largest share of S&P 500 cash use in 2021, but forecasts the fastest year/year growth will be in cash M&A and share buybacks. After a 10% decline in cash spending in 2020, the bank forecasts that high cash balances, anemic yields as well as strong economic and earnings growth will combine to drive 19% growth in cash spending in 2021 ($2.8 trillion) and 6% in 2022 ($3 trillion). Investing for growth (capex, R&D, and cash M&A) should account for 55% of total cash spending in 2021. High cash balances, record buyback authorizations, and excess capital for Financials post-CCAR should also drive a 35% rebound in buybacks in 2021. Indeed, data from the bank’s buybacks desk show that US corporates have authorized $627 billion in buybacks YTD, the second-fastest pace on record (only behind the tax reform aided level in 2018) and 155% above 2020 levels

In terms of preferred trades, Kostin highlights a screen of stocks with above-average net margins, realized margin growth of 50+ bp in 2020, and expected margin growth of 50+ bp in each of the next two years.

The median stock has a 2021E net margin of 26% (vs. 13% for S&P 500 median) and is forecast to grow margins by 306 bp through 2022 and (vs. 156 bp for median stock).

Tyler Durden

Sun, 07/11/2021 – 13:00![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com