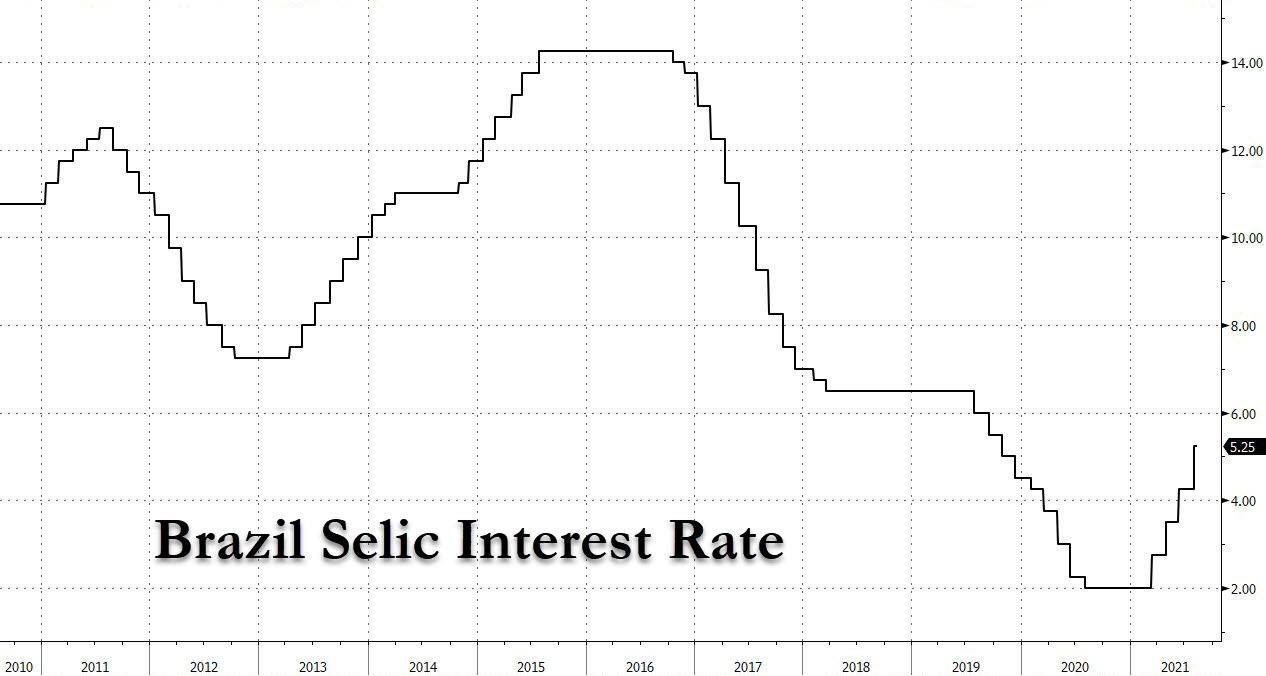

Unlike The Fed, Brazil Central Bank Vows To Do Whatever It Takes To Tame Soaring Inflation

Just days after Brazil’s central bank hiked rates last Wednesday by a whopping 100bps, to 5.25% and up 325bps since March, with market consensus for much more tightening to come, Brazilian policy markets vowed to do what the Fed won’t – or can’t – do, and will do whatever it takes to bring inflation expectations back to target despite a perceived deterioration in the country’s fiscal outlook .

Speaking at a Thursday online event organized by the national association of bars and restaurants, Campos Neto said “keeping inflation anchored is key at this moment, when we are facing consecutive inflationary shocks and it’s becoming difficult to model inflation.”

Foreign investors are perceiving a deterioration in Brazil’s fiscal accounts, Campos Neto said, as spending pressures mount ahead of next year’s presidential election. His remarks echoed similar comments made by Monetary Policy Director Bruno Serra on Wednesday, and followed the central bank’s decision to step up the pace of monetary tightening last week.

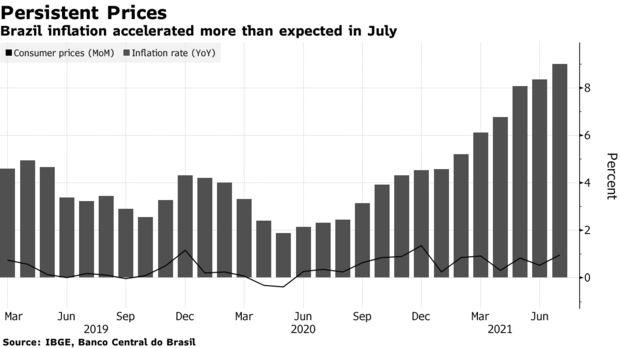

Neto’s speech comes at a time when the most severe drought in decades, along with higher commodity prices and an economic reopening are keeping inflation well above target in Brazil. Consumer prices soared 8.99% in July from the year prior, higher than economists forecast and the highest in over 5 years. Analysts polled by the central bank estimate consumer prices to rise 6.88% in 2021 and 3.84% in 2022, above the targets of 3.75% and 3.5% for each year.

The main drivers of Brazil’s runaway inflation are housing costs, which jumped 3.1% on the month due mainly to electricity bills that increased 7.88%, while transportation prices rose 1.52%, the statistics agency said.

“We will use all the tools we have, as much as needed, to anchor inflation in the medium and long term,” Campos Neto said, adding that current inflationary shocks are contaminating expectations for next year. His comments follow the central bank’s guidance from last week which signaled another 100bps Selic increase at the September meeting, and a hiking cycle that will ultimately drive the Selic to an above-neutral level; i.e., into restrictive territory as the central bank scramble to contained soaring prices.

After promising last week to raise interest rates above the so-called neutral level, the central banker said later on Thursday he still considers that point to be around 3% in real terms according to Bloomberg. Yet there’s an upward bias to that rate, which neither stimulates nor restricts the economy, when the most recent macroeconomic data is taken into account, he added.

Tyler Durden

Sat, 08/14/2021 – 22:00![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com