“Rapidly Becoming Untenable” – Eurozone Finances Have Deteriorated

Authored by Alasdair Macleod via GoldMoney.com,

Despite negative interest rates and money printing by the European Central Bank, which conveniently allowed all Eurozone member governments to fund themselves, having gone nowhere Eurozone nominal GDP is even lower than it was before the Lehman crisis.

Then there is the question of bad debts, which have been mostly shovelled into the TARGET2 settlement system: otherwise, we would have seen some substantial bank failures by now.

The Eurozone’s largest banks are over-leveraged, and their share prices question their survival. Furthermore, these banks will have to contract their balance sheets to comply with the new Basel 4 regulations covering risk weighted assets, due to be introduced in January 2023.

And lastly, we should consider the political and economic consequences of a collapse of the Eurosystem. It is likely to be triggered by US dollar interest rates rising, causing a global bear market in financial assets. The financial position of highly indebted Eurozone members will become rapidly untenable and the very existence of the euro, the glue that holds it all together, will be threatened.

Introduction

Understandably perhaps, mainstream international economic comment has focused on prospects for the American economy, and those looking for guidance on European economic affairs have had to dig deeper. But since the Lehman crisis, the EU has stagnated relative to the US as the chart of annual GDP in Figure 1 shows.

Clearly, like much of the commentary about it, the EU has been in the doldrums since 2008. There was a series of crises involving Greece, Cyprus, Italy, Portugal, and Spain. And the World Bank’s database has removed the UK from the wider EU’s GDP numbers before Brexit, so that has not contributed to the EU’s underperformance. Furthermore, since 1994 the gap between Eurozone and non-Eurozone member nations GDP growth has increased from 9% of the total to 15%, even adjusted for new memberships. It tells us that despite all the ECB’s money-printing, non-Eurozone members facing the same regulations and trading restrictions using their own currencies have outperformed the Eurozone.

The ECB has enforced negative interest rates since June 2014, cutting its deposit rate four times since its initial -0.1% rate to -0.5%. The monetary policy planners clearly thought negative rates would boost credit demand for investment and consumption, provide fiscal space for governments and thus increase aggregate demand. It didn’t turn out like that. The principal aspect which negative interest rates has boosted is government debt, which in the Eurozone at the end of 2020 had risen to 98% of GDP overall for Eurozone members.

Admittedly, bungled management of covid and vaccines have not not helped. Not only did they increase government spending, but tax income suffered from the economic consequences. The global logistics crisis has seriously impacted the highly productive German economy, with major manufacturers seeing their production grinding to a halt for lack of components. And in many jurisdictions covid lockdowns have continued, delaying hoped-for recoveries, and hitting tourism in the highly indebted PIGS.

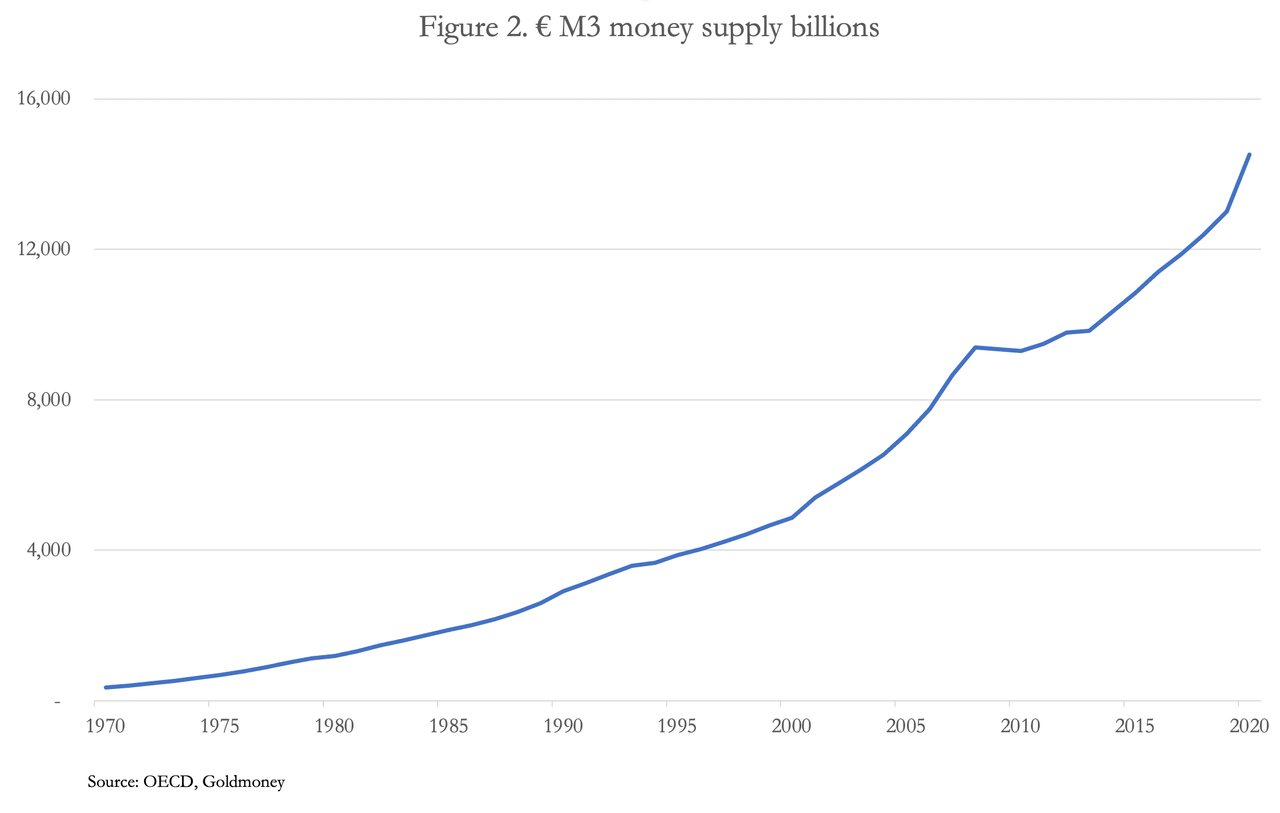

As Figure 1 demonstrates, these troubles are in addition to the economic stagnation that has been a feature of the Eurozone since the Lehman crisis. The consequences of covid do not yet appear to be adequately reflected in official GDP figures, which will have been pushed higher by an acceleration of growth in euro money supply.

Broad money increased significantly in 2020, as shown in Figure 2 below, mainly due to the expansion of central bank balances in the Eurozone.

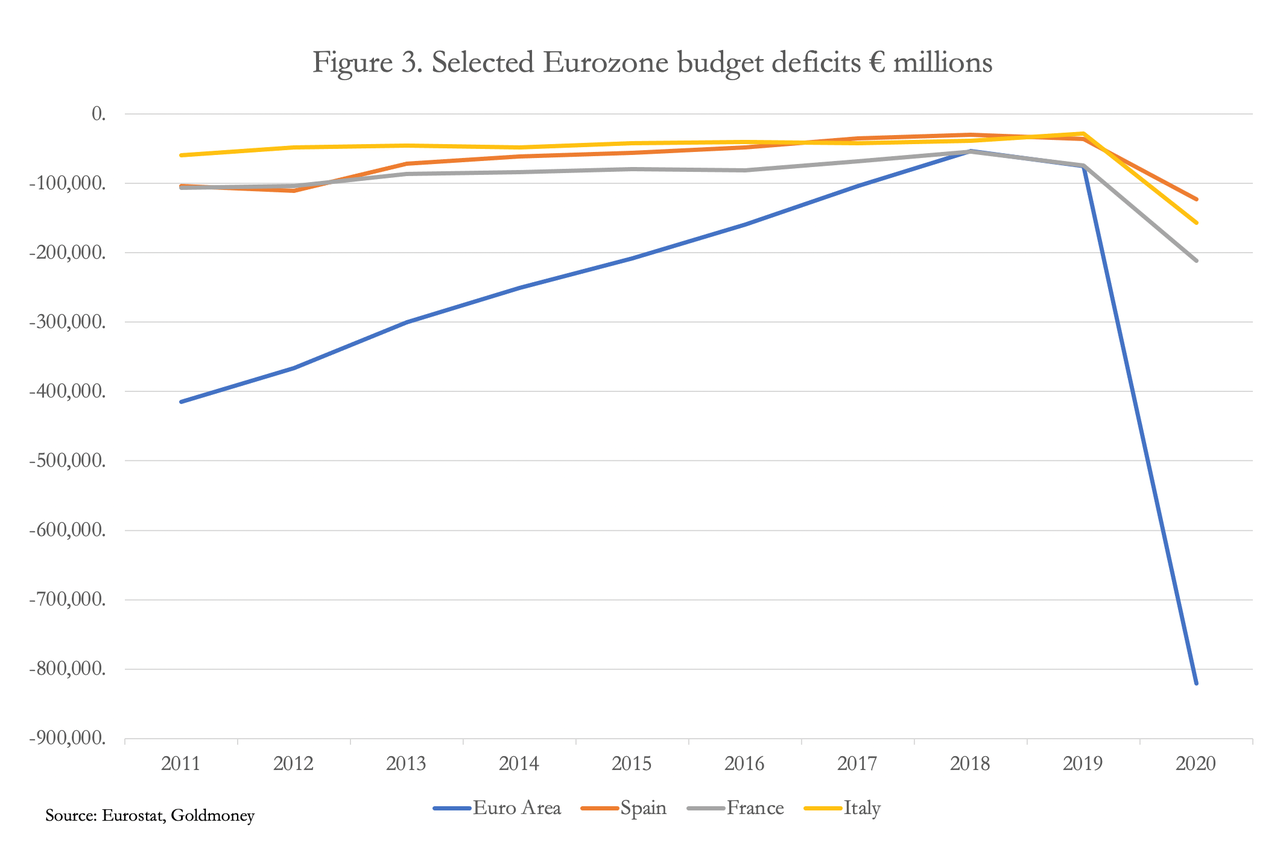

At the same time, having recovered somewhat since the series of crises following Lehman, government finances took a sharp turn for the worse, as shown in Figure 3.

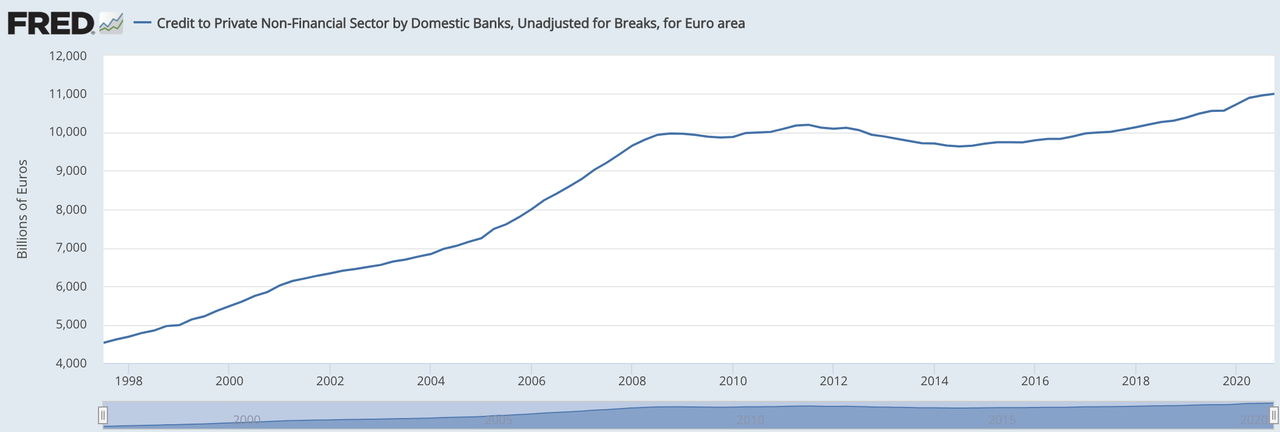

The reason for the Eurozone’s underperforming GDP relative to that of the US revealed in Figure 1 is not hard to discern. The chart below from the St Louis’ FRED shows how bank lending to the non-financial sector has broadly stalled since the Lehman crisis.

Instead, monetary growth has been in the Eurosystem, comprising the ECB and the national central banks. From €2 trillion at the end of 2008, total Eurosystem balances grew to €7 trillion at end-2020, some of this due to rising imbalances in TARGET2 which are reflected in expanded central bank balance sheets.

Government deficits in the Eurozone are persisting into the current year, expected by the ECB itself to rise to 8.7% of 2021 GDP. That’s on an estimated GDP of €13.476 trillion, giving a public sector deficit of €1.2 trillion, taking the debt to GDP figure to 103% for 2021. But this increase is mainly on the back of planned infrastructure spending and assumes a sharp recovery in tax revenues on the back of improving employment and higher consumer spending. That has already been overtaken by events, and fiscal deficits will be far higher than forecast.

In official forecasts by the ECB there is a strong dose of neo-Keynesian optimism in expectations, which we have seen time and again with the Eurozone’s economic establishment. Furthermore, under the presidency of Christine Lagarde, the ECB is meddling in non-monetary affairs, giving precedence to a green agenda over fossil fuels, and creating precedents for the politicisation of monetary affairs. It seems that the uses of the ECB’s magic money tree are one of the few aspects of economic affairs which are growing…

Of one thing we can be certain, and that is blindness at the ECB to the global credit cycle driven by America and the dollar. Officially, US prices are rising at 5.4%, while in the Eurozone they are at the goal-sought target of 2%. We know that in the US independent analysis confirms the true rate of rising prices is over 13%, so by using similar CPI methodology the Eurozone’s statisticians are misrepresenting the true effect of rapidly increasing monetary inflation. It is not going to be transient. Consequently, not only will interest rates begin to rise in the US, but they will also rise from a negative ECB deposit rate of minus 0.5%. Amongst others, the Italian government will no longer be paid to borrow.

The policy of continual monetary stimulation has run out of time, creating a crisis for ECB policy makers. Like their opposite numbers in the US and other major central banks they face the growing certainty of rising interest rates, falling financial asset values, and a slump accompanied with soaring prices. According to neo-Keynesianism the combination is an impossibility, yet that is now in prospect.

Not only is the starting point negative interest rates, but so is an average level of government debt to GDP of 103%. Averages conceal extremes, and with Greece’s debt to GDP officially at 217%, Italy at 151% and Portugal at 137% (they are likely to be higher once off-balance sheet debt for nationalised industries etc. are considered) a combination of an economic downturn and soaring prices will destroy their parlous finances.

Under “Whatever it takes” Mario Draghi, the ECB used every trick to cover over the cracks of a failing Eurozone. At the heart of the trickery was bad debt being concealed within the TARGET2 settlement system. It is only by this subterfuge that major banks have been prevented from failing.

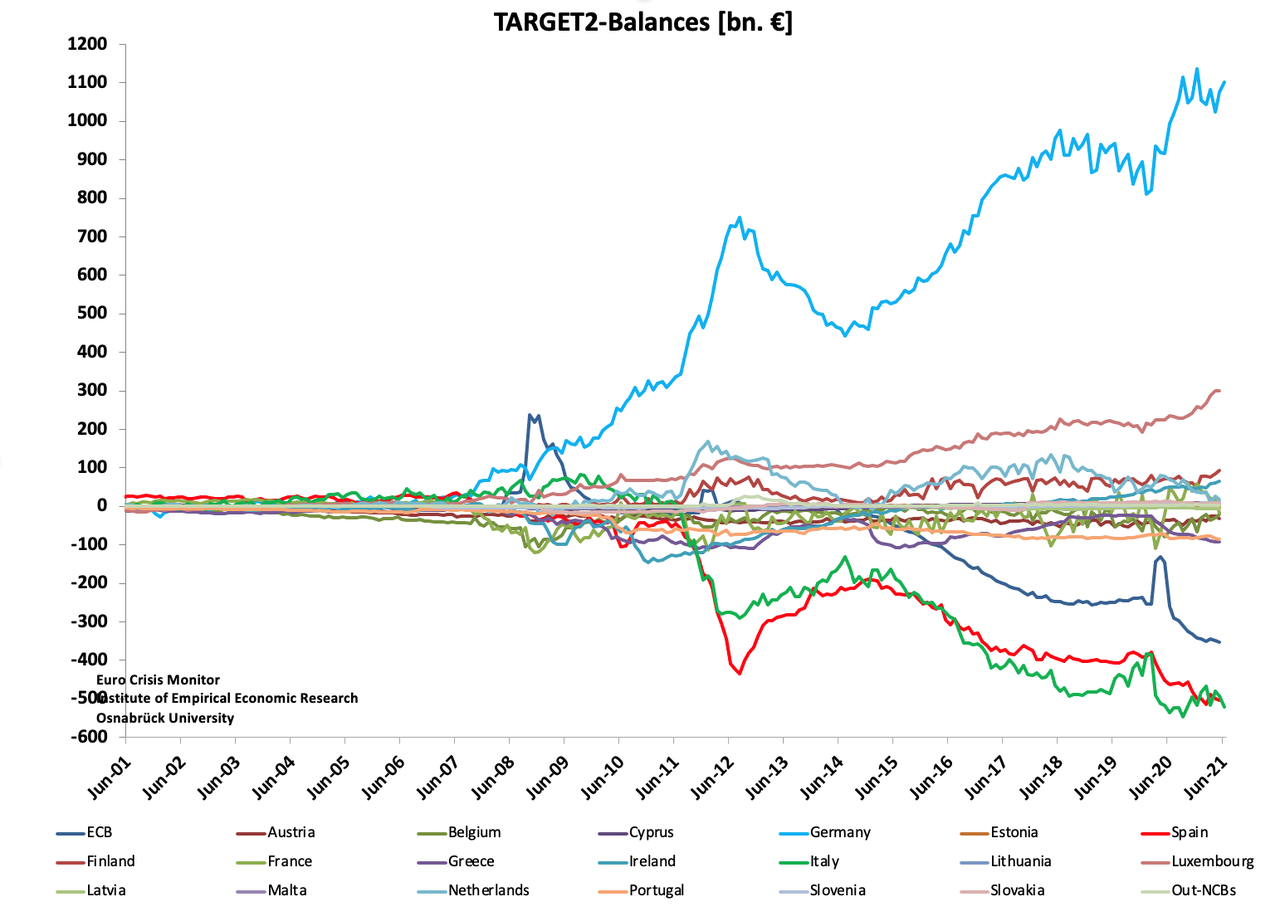

As the chart of the TARGET2 central bank balances shows, creditor balances are increasing again. To understand why, we should consider what is driving them.

The chart illustrates the imbalances in the TARGET2 settlement system between the national central banks, and between them and the ECB. It reveals three notable features. Germany and Luxembourg between them are owed a net €1.4 trillion. Italy and Spain between them owe the system €1,024bn. And the ECB owes the national central banks €353bn. The effect of the ECB deficit, which arises from bond purchases conducted on its behalf by the national central banks, is to artificially reduce the TARGET2 balances of debtors in the system to the extent the ECB has bought bonds from government and other issuers within an NCB’s jurisdiction and not yet paid for them.

Inside the workings of TARGET2

The way TARGET2 works, in theory anyway, is as follows. A German manufacturer sells goods to an Italian business. The Italian business pays by bank transfer drawn on its Italian bank via the Italian central bank through the Target2 system, crediting the German manufacturer’s German bank through Germany’s central bank.

In the past, the balance was restored by trade deficits, in Italy, for example, being offset by capital inflows as residents elsewhere in the eurozone bought Italian bonds, other investments in Italy and the tourist trade collected net cash revenues. As can be seen from the chart of TARGET2 balances, before 2008 this was generally true. Part of the subsequent problem was down to the failure of private sector investment flows to recycle trade-related payments.

Then there is the question of “capital flight”, which is not capital flight as such. The problem is not residents in Italy and Spain opening bank accounts in Germany and transferring their deposits from domestic banks. It is that those national central banks which are heavily exposed to potentially bad loans in their domestic economy know that their losses, if materialised in a general banking crisis, will end up being shared throughout the central bank system, according to their capital keys in the TARGET2 settlement system.

If one national central bank runs a Target2 deficit with the other central banks, it is almost certainly because it has loaned money on a net basis to its commercial banks to cover payment transfers, instead of progressing them through the settlement system. Those loans appear as an asset on the national central bank’s balance sheet, which is offset by a liability to the ECB’s Eurosystem through Target2. But under the rules, if something goes wrong with the TARGET2 system, the costs are shared out by the ECB on the pre-set capital key formula.

It is therefore in the interest of a national central bank to run a greater deficit in relation to its capital key by supporting the insolvent banks in its jurisdiction. The capital key relates to the national central banks’ equity ownership in the ECB, which for Germany, for example, is 26.38% of the euro-area national banks’ capital keys.[iii] If TARGET2 collapsed, the Bundesbank would lose the trillion plus euros owed to it by the other national central banks, and instead must pay up to €400bn of the net losses.

To understand how and why the problem arises, we must go back to the earlier European banking crises following Lehman, which has informed national regulatory practices. If the national banking regulator deems loans to be non-performing, the losses would become a national problem. Alternatively, if the regulator deems them to be performing, they are eligible for the national central bank’s refinancing operations. A commercial bank can then use the questionable loans as collateral, borrowing from the national central bank, which spreads the loan risk with all the other national central banks in accordance with their capital keys. Insolvent loans are thereby removed from the PIGS’ national banking systems and dumped onto the Eurosystem.

In Italy’s case, the very high level of non-performing loans peaked at 17.1% in September 2015 but by March this year had been reduced to 5.3%. The facts on the ground state that this cannot be true. Given the incentives for the Italian regulator to deflect the non-performing loan problem from the domestic economy into the Eurosystem, it would be a miracle if any of the reduction in NPLs is genuine. And with all the covid-19 lockdowns, Italian NPLs will have soared again, explaining perhaps why the Italian central bank’s TARGET2 liabilities have increased by €137bn over the course of covid lockdowns.

In the member states with negative TARGET2 balances there have been trends to liquidity problems for legacy industries, rendering them insolvent. With the banking regulator incentivised to remove the problem from the domestic economy, loans to these insolvent companies have been continually rolled over and increased. The consequence is that new businesses have been starved of bank credit because bank credit in the member nation’s banks is tied up with supporting the government and zombie businesses that should have gone to the wall long ago. The added pressure on failing Italian businesses from covid-19 is now being reflected in the Bank of Italy’s soaring TARGET2 deficit. The system could not be more calculated to cripple the Italian economy over the longer term.

Officially, there is no problem, because the ECB and all the national central bank TARGET2 positions net out to zero, and the mutual accounting between the national central banks keeps it that way. To its architects, a systemic failure of TARGET2 is inconceivable. But, because some national central banks end up using TARGET2 as a source of funding for their own balance sheets, which in turn fund their dodgy commercial banks using their non-performing loans as collateral, some national central banks have mounting potential liabilities, the making of national bank regulators.

The Eurosystem member with the greatest burden is Germany’s Bundesbank, now lending well over a trillion euros through TARGET2 to central banks exploiting the system. The risk of losses for the TARGET2 lenders is now accelerating rapidly because of Covid lockdowns, as can be seen in the chart of TARGET2 imbalances above. The Bundesbank should be very concerned.

Current imbalances in the system total over €1.6 trillion. According to the capital keys, in a systemic failure the Bundesbank’s assets of €1.102 trillion would be replaced by liabilities up to €400bn, the rest of the losses being spread around the other national banks. No one knows how it would work out because failure of the settlement system was never contemplated; but many if not all the national central banks will have to be bailed out on a TARGET2 failure, presumably by the ECB as guarantor of the system. But with only €7.66bn of subscribed capital the ECB’s balance sheet is miniscule compared with the losses involved, and its shareholders will themselves be seeking a bailout to bailout the ECB. A TARGET2 failure would appear to require the ECB to effectively expand its QE programmes to recapitalise itself and the whole eurozone central banking system.

Eurozone banks are overleveraged

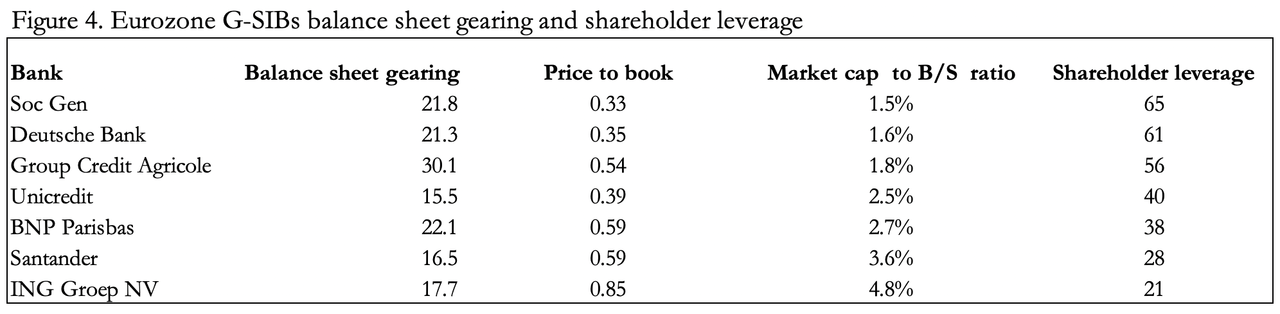

Almost certainly, the concealment of bad debts in TARGET2 has saved the Eurozone’s commercial banks from going under, because they are very highly geared to losses, as the table, of the Eurozone’s global systemically important banks (G-SIBs) in Figure 4 illustrates.

They are ranked from highest shareholder leverage (the end column), being the relationship of their market capitalisation to the size of their balance sheets. The balance sheet gearing, that is the ratio of balance sheet assets to balance sheet equity, are all exceptionally high with the French bank, Credit Agricole, being over 30 times. This compares with American G-SIBs which are geared an average of about 11 times. And while the US G-SIBs have a price to book ratio averaging about 1.3 times, none of the Eurozone G-SIBs have a price to book of over one.

Normally, value investors get excited at the prospects for an investment at a discount to book value. But that presupposes that the business is viable and whose shares are mispriced. In the case of these G-SIBs the message is different, being a serious question mark over their likely survival. It is doubly serious because an investor picking up Eurozone bank shares knows they are effectively underwritten by the ECB and the national banks, who would be certain to come to their rescue in the event of a systemic crisis. Yet with this implied guarantee, shares in Société Generale and Deutsche Bank are trading with that value embedded in their share prices.

In other words, there is option value to be had, and little else.

We see banks such as Société Generale and Deutsche having an implied leverage for shareholders of over 60 times. It makes sense to look through these numbers and conclude that so far as the markets are concerned, the Eurosystem’s ability to rescue these banks from collapse may be limited. A rescue of failing G-SIBs is a near certainty, but the terms are not. Furthermore, the threat of bail ins, which are now widely incorporated in G-20 legislation, would leave existing shareholders heavily diluted.

The effect of Basel 4

Basel 4 is the informal name given to Basel 3 regulations concerning risk-weighted assets (RWAs), already delayed and now due to be introduced in January 2023. It is difficult to see how Eurozone banks, particularly the G-SIBs, will be able to comply without reducing their balance sheets.

The aim of the new regulations is to ensure banks’ resilience to crises by prescribing how much capital and liquidity they need to hold by introducing a standardised approach. Banks will still be able to use internal models for calculating the capital required for risk weighting assets, but they are to be limited by not falling below 72.5% of the figures thrown up by the new standardised approach. The European banking Authority has calculated that the impact of these regulations will cause RWAs to increase by 28%, equivalent to a capital shortfall of €135bn for European banks.

Operationally, European banks are badly affected compared with those in other jurisdictions. Basel 4 discriminates against loans to corporates not independently rated which are uncommon in the US, but not in the EU. External ratings apply to only 20% of European corporates, throwing the emphasis onto lenders’ internal rating systems, which are to be strictly limited. Hence, the need for more capital.

In normal conditions, with bank capitalisations being greater than book value, raising qualifying capital to maintain balance sheet sizes would not be a problem. But as we have seen in our ranking of Eurozone G-SIBs in Figure 4, all their shares stand at a discount to book value.

Senior bankers will already have an eye to these regulations and are unlikely to be prepared to provide the general expansion of credit required to support seemingly optimistic growth forecasts emanating from the ECB. If anything, an Irving Fisher style slump, whereby banks accelerate falling asset values by liquidating them as they fall, has become more likely.

The euro’s fate

The public realisation of the situation within TARGET2 and the precariousness of the major banks, plus in the absence of some extremely imaginative accounting the inability of banks to come up with extra capital to satisfy Basel 4 could terminate the European project. In particular, when Germany’s Bundesbank finds that instead of being owed some €1.1 trillion by the other national central banks, she is on the hook for €400bn it will be the last straw for a people whose thrift and savings will have been wiped out. The same can be said for Finland, Luxembourg, the Netherlands, and some of the smaller states.

When one is in possession of the facts the end of the euro is easy to envisage. But early in a crisis, capital flows are likely to enhance the euro’s exchange rate, particularly against the US dollar. This is because of the accumulation of trade surpluses and portfolio flows from EU entities which has increased Eurozone entities dollar exposure. According to US Treasury TIC data, Eurozone holdings of US financial assets totalled $5,339bn and there is a further $1,158bn in dollar bank deposits and money instruments.

Meanwhile, US exposure to liquid Eurozone financial assets and bank balances is far less. Therefore, the rush to liquidity typically seen in a financial crisis is likely to initially favour the euro against the dollar.

Summary and conclusions

In defiance of the terms of the Stability Pact in the1992 Maastricht Treaty, from the admission of Greece and Italy into the Eurozone the history of the euro and the ECB has been one of persistent rule-breaking and cover-ups. Without covid, and without rising prices now almost certain to drive global interest rates higher, the ECB and Brussels might have got away with ignoring some basic rules of statist behaviour a little longer.

The crisis facing the Eurozone differs from that facing the US, which, putting aside social factors, is principally the consequence of money-printing. While similar policies have been pursued in the Eurozone, they have not been to the same extent. The problems are more structural, with a banking system that is over-leveraged and reliant on concealing bad debts in the TARGET2 settlement system.

Furthermore, much of the socialism which is relatively new to the US has been embedded in European economies since at least the Second World War, with more than half economic activity being down to unproductive government spending. The cumulative effect of central planning has been to make the economies of EU nations less efficient and through over-regulation divorced from free and efficient markets.

But a final crisis is mounting. After an initial flight out of the dollar into the euro subsides it will be virtually impossible to avoid a wholesale systemic failure, taking down not just the banks, but the central banking network and the euro itself. Some nations will be able to return to their old currencies credibly, but others, particularly Italy and Greece, probably not. And attempts to replace the euro with a new euro and central banking network will face significant hurdles.

The reality is that the euro is the glue that holds Eurozone members together, and without it the European project is effectively dead. The clamour for a return to independent nation states will be almost impossible to resist, not just for Germany, but for those that value its voice of reason. Middle-Europeans, such as Poland and Hungary are likely to stop their attempts at reforming the EU from within and just leave, and some of the smaller nations which are there for the subsidies will have no reason to stay.

An overly dramatic forecast perhaps, but one that is increasingly likely, despite Draghi’s whatever it takes.

Tyler Durden

Sat, 08/28/2021 – 07:00![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com