A few months ago US national debt exceeded $28 trillion. This number is certainly the one economists usually work with, but does this figure capture a long-term perspective?

In March 2021, the Department of the Treasury published the 2020 Financial Report of the United States Government. In the initial message, Secretary Janet L. Yellen writes: “This Financial Report discusses not only current financial results but also important, long-term trends affecting our critical social insurance programs and fiscal health.” The report not only discloses the current debt level, but also projects the cost of the government’s future obligations to its citizens. It notes that citizens will have the right to demand benefits from the state in the future.

The United States is one of the few countries whose treasury, in an act of transparency and with rigorous analysis, has warned its government of the unsustainability of the country’s public finances.

The US Department of the Treasury anticipates that unless there are substantial changes, the system will not be sustainable: “If changes in policy are not so abrupt as to slow economic growth, then the sooner policy changes are adopted, the smaller the changes to revenue and/or spending [that] will be required to return the government to a sustainable fiscal path.”

Government reports on macroeconomic matters tend to be ambivalent. Nevertheless, this one’s conclusion is decisive: the US government’s fiscal policy is unsustainable.

The Primary Deficit

The report usefully distinguishes between the primary deficit and the total deficit. Generally speaking, the primary deficit does not include the cost of servicing the debt (i.e., interest) while the total deficit does.

To conduct a rigorous analysis of public finance sustainability, it is appropriate to consider the primary deficit, because if there is a structural primary deficit, it is difficult for a country to achieve long-term sustainability no matter the interest rate. The Fed could help the government lower the total deficit with a rate decrease, but major structural changes are needed to lower the primary deficit.

The following graph, which appears in the report, compares total fiscal receipts, represented by the black line, with total structural expenditure. When the line representing total receipts (the thick black line) is below the sum of the various budget expenditure items, there is a primary deficit. During the years of the financial crisis (2009–12), the deficit-to-GDP ratio spiked, and it skyrocketed again in 2020 due to increased spending to address covid-19.

Chart 1: Comparison of Each Major Category’s Weight with Respect to Tax Revenues

Source: US Department of the Treasury, Financial Report of the United States Government, FY 2020, Mar. 25, 2021.

The Department of the Treasury assumes there will be a structural primary deficit and that total deficit (represented by the difference between the blue line and the thick black line), which includes the cost of servicing the debt, will increase with time.

The report continues with a graph that illustrates how, if the trend continues, the government’s debt could reach 300 percent of GDP in less than forty years.

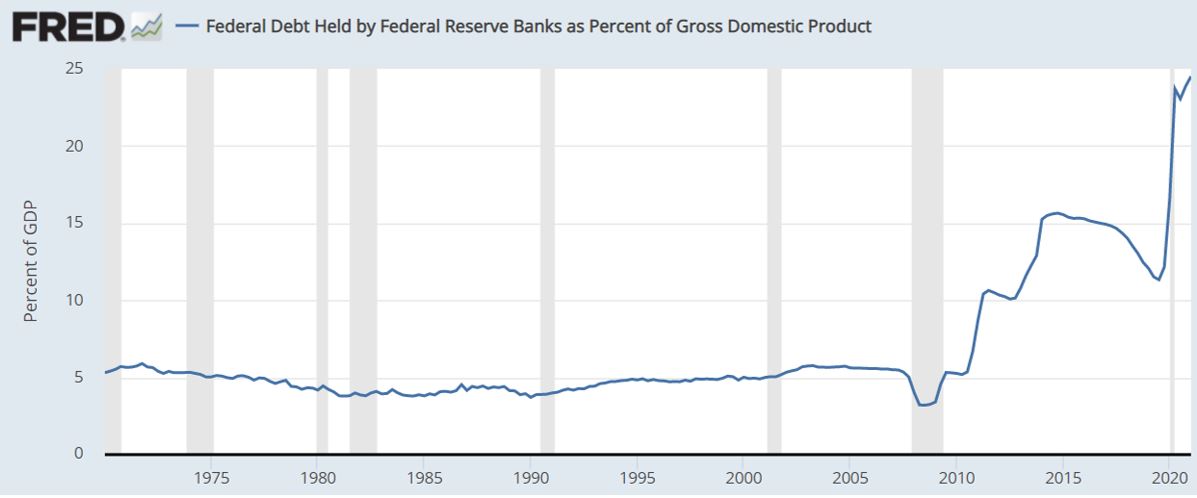

It is important to clarify that the above graph only considers “debt held by the public,” currently around 100 percent of GDP; however, if debt held by Federal Reserve Banks were included, the total debt would be 130 percent of GDP. The Fed argues that this additional $6 trillion debt should not be considered because “Federal Reserve Banks remit their profits to the Treasury, [and] any interest earned on their federal debt is rebated to the federal government.” But if the Fed continues to increase its position relative to US debt, this consideration might need to be reviewed.

In any case, the Department of the Treasury projects the future debt of the government and calculates that it could triple GDP within forty years. If the Federal Reserve Banks’ debt were consolidated, this threshold would be reached in much less time.

A country with a welfare state commits to offering its citizens future benefits (principally pensions and health services) using taxes collected in the present. While tax revenues are accounted for upon collection, government’s future obligations are not. What would happen if we accounted for the obligations in present value terms? This is exactly what the Department of the Treasury does in its analysis.

US companies that agree to provide their employees with future pensions (which the companies have to finance) have to budget annually to satisfy their future payment obligations in accordance with US Generally Accepted Accounting Principles (GAAP). But the government is not required to make provisions to cover future benefits, currently doing so only for federal employees and veterans.

What Would the Debt Figure Be If the United States Calculated the Present Value of Future Obligations?

The Department of the Treasury declares that “[t]he long-term fiscal projections indicate that the government’s debt-to-GDP ratio will rise to 623 percent over the 75-year projection period, and will continue to rise thereafter, if current policy is kept in place.” Just to give an idea of how fast the debt-to-GDP forecasts are increasing, the same report two years ago estimated that same ratio would rise to 530 percent in that period.

Let’s see why the debt is projected to become more than six times GDP.

First, considering a seventy-five-year projection period, the net present value of future tax revenues is estimated to be $295.4 trillion. From this the present value of future noninterest spending—$374.9 trillion—must be subtracted. The main projected expenditures are on social insurance—that is, healthcare and pensions.

The Statements of Long-Term Fiscal Projections (SLTFP) shows that the present value of total noninterest spending, including Social Security, Medicare, Medicaid, defense, education, etc., over the next seventy-five years under current policy is projected to exceed the present value of total receipts by $79.5 trillion. Social insurance net expenditures (Social Security and Medicare) account for $65.5 trillion of this noninterest spending.

However, these projections fix variables that the calculation of payment obligations is very sensitive to, such as the fertility rate, life expectancy, and average annual growth in health costs. Much like in the majority of developed countries, the fertility rate (defined as number of children per woman) in the United States showed a downward trend. In 2007 this ratio was 2.1 percent while in 2020 it reached 1.64 percent, a record low. Is it realistic to assume that fertility rate will return to 2.0 and remain stable for the next seventy-five years, as the Treasury’s projections assume? Using an assumed fertility rate of 1.8 percent (closer to the current one) instead of 2.0 percent increases the financing shortfall by $2.5 trillion. The same is true for average annual growth in health costs: if 4.7 percent is used instead of 3.7 percent, $14 trillion more in debt are added.

The Department of the Treasury also assumes the country will not disintegrate. Therefore, it calculates the present value of future revenues and obligations into the indefinite future (valuations by companies similarly assume they will operate indefinitely):

Experts have noted that limiting the projections to 75 years understates the magnitude of the long-range unfunded obligations because summary measures reflect the full amount of taxes paid by the next two or three generations of workers, but not the full amount of their benefits … [E]xtending the calculations beyond 2094, captures the full lifetime benefits, plus taxes and premiums of all current and future participants. The shorter horizon understates the total financial needs by capturing relatively more of the revenues from current and future workers and not capturing all the benefits that are scheduled to be paid to them.

With these adjustments, the present value of future costs less the present value of future income rises to $154 trillion, and let’s recall that this figure does not include interest expenses nor the debt held by the Fed in their books.

What Is the Situation in Other Countries?

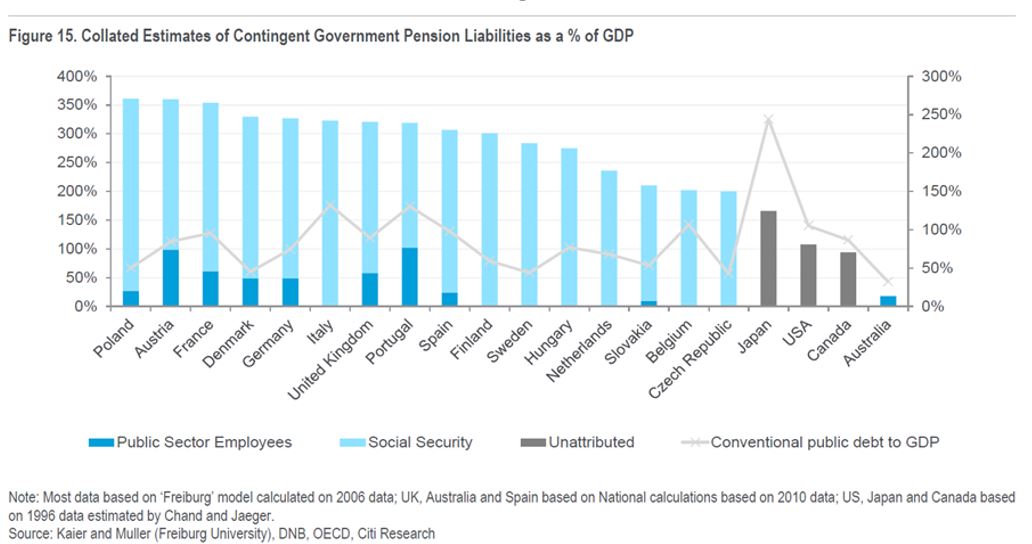

Unfortunately, the same analysis applies to other countries. In fact, some years ago Citigroup calculated what the debt would be if future government pension liabilities were accounted for in present value terms. Note that the report only includes expenditures on pensions.

As can be seen in the graph, the majority contingent government pension liabilities in most European countries reached a present value of three times their GDP.

Conclusion

Economists need to warn the public of the unsustainable nature of our governments’ public finances. Only then will our political leaders be able to debate measures that might reverse the undesirable trends.

Not much can be added to what has been exposed in the US government’s financial report, and its conclusions speak for themselves:

The continuous rise of the debt-to-GDP ratio indicates that current policy is unsustainable…. The projections in this Financial Report indicate that if policy remains unchanged, the debt-to-GDP ratio will steadily increase throughout the projection period and beyond based on this report’s assumptions, which implies current policy is not sustainable and must ultimately change. Subject to the important caveat that policy changes are not so abrupt that they slow economic growth, the sooner policies are put in place to avert these trends, the smaller are the adjustments necessary to return the nation to a sustainable fiscal path, and the lower the burden of the debt will be to future generations.

The Mises Institute exists to promote teaching and research in the Austrian school of economics, and individual freedom, honest history, and international peace, in the tradition of Ludwig von Mises and Murray N. Rothbard. These great thinkers developed praxeology, a deductive science of human action based on premises known with certainty to be true, and this is what we teach and advocate. Our scholarly work is founded in Misesian praxeology, and in self-conscious opposition to the mathematical modeling and hypothesis-testing that has created so much confusion in neoclassical economics. Visit https://mises.org