Evergrande Suspends Trading In All Bonds

Earlier today we pointed out that in what can (obviously) only be a remarkable coincidence, China’s largest, and most systematically important real estate developer, China Evergrande (and its $300+ billion in debt), collapsed on the 13th anniversary of Lehman’s bankruptcy filing, when Beijing told Evergrande’s creditor banks that the insolvent company, which recently hired Houlihan Lokey as bankruptcy advisor, would not pay interest on its debt next week, nor would it repay principal, in effect blessing the coming default.

And yet there was some trace of hope, because as Forte Securities trader Keith Temperton said “The Asian banks will get hit hard if there’s a default, but then there will be a 10-year recovery process. The market’s getting a hang of it. The way they’ve managed the news flow seems quite clever. They haven’t let a swathe of bad news at once” giving investors and creditors some hope that the money could still miraculously reappear.

Not any more: in an exchange filing on Thursday, Evergrande’s main unit (onshore real estate) said that trading in all of its onshore bonds would be suspended on Sept 16 to ensure fair information disclosure following a downgrade to A from AA (which in China is viewed as the lowest investment grade rating) by China Chengxin International, to wit:

In order to ensure fair information disclosure and protect the interests of investors, after the company’s application, all existing corporate bonds of Evergrande Real Estate will be suspended for one trading day from the opening of the market on September 16, 2021, and will be opened on September 17, 2021.

Since the market resumes trading, the above-mentioned bond trading methods will be adjusted from the date of resumption of trading. Among them: (1) The trading methods of “15 Evergrande 03”, “19 Evergrande 01”, and “19 Evergrande 02” have been adjusted to only adopt quotation, inquiry and agreement trading methods since the date of resumption of trading. Shanghai Branch of Registration and Settlement Co., Ltd. provides settlement by transaction; (2) “20 Evergrande 01”, “20 Evergrande 02”, “20 Evergrande 03”, “20 Evergrande 04”, “20 Evergrande 05” The trading methods of “21 Evergrande 01” and “21 Evergrande 01” have been adjusted to only adopt the negotiated block trading method since the resumption of trading, and the original net price pricing method will be maintained.

The press release ends with the hilarious “Investors are kindly requested to pay attention to investment risks.” Well… we sure can be certain they are paying attention now.

It wasn’t clear why the company would need to suspend trading in all bonds for an entire day to “ensure” that everyone was aware that the company’s bonds were no longer rated as investment grade in China (they should be rated as default but we’ll cross that bridge in time) when just a simple press release would suffice.

Instead, what the company did say is that the bonds would resume trading on Sept. 17, and the trading method for some of the securities will change to only allow block trades even as the previous pricing method will remain.

Despite the company’s promise that its bonds will resume trading, we somehow doubt it and instead we expect that in the coming months, the frozen bonds will be equitized as part of China’s largest ever debt for equity exchange. Come to think of it, the rest of the market doesn’t believe it either with Evergrande stock plunging another 7% (Zeno’s paradox means the company can keep falling at double digits every day in perpetuity) and as of Thursday Evergrande’s only traded security was at the lowest price since Oct 2011, on its way to 0.

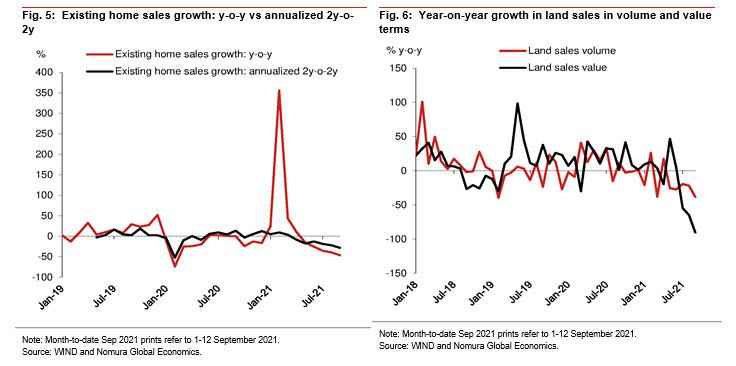

Meanwhile, as the book on Evergrande’s story closes, the company’s imminent default and the sudden collapse in China’s property market which as we noted last night saw a 90% crash in land sales values in August…

… have led to a dire outlook for the nation’s developers and their creditors. As Bloomberg’s Richard Frost writes, Country Garden, the nation’s largest developer by sales, plunged 16% in the past two days, while Gemdale slumped 12% as a gauge of property shares in Shanghai tumbled almost 5% in the period, with valuations firmly below book value. Following the news, Guangzhou R&F Properties drops 10.8% to the lowest since Dec. 2008 while Greentown China -9.1%. At this point, one can safely call it a crisis.

As contagion spread, risk is also hitting banks whose shares are suffering their fastest selloff in seven weeks. Furthermore, as discussed yesterday ahead of the coming Evergrande debt crisis, lenders in China are accepting the highest rates in four years to swap their dollars for yuan, a sign they may be preparing for what Mizuho calls a “liquidity squeeze in crisis mode.”

The pain will only get worse. China’s government is unlikely to ease up on its tough curbs toward the property market given its current priorities of promoting common prosperity and deterring excessive risk-taking, according to Macquarie. The property sector will be a “main growth headwind” for next year, although policy makers may loosen restrictions to defend 5% GDP expansion, Macquarie analysts wrote in a Wednesday note.

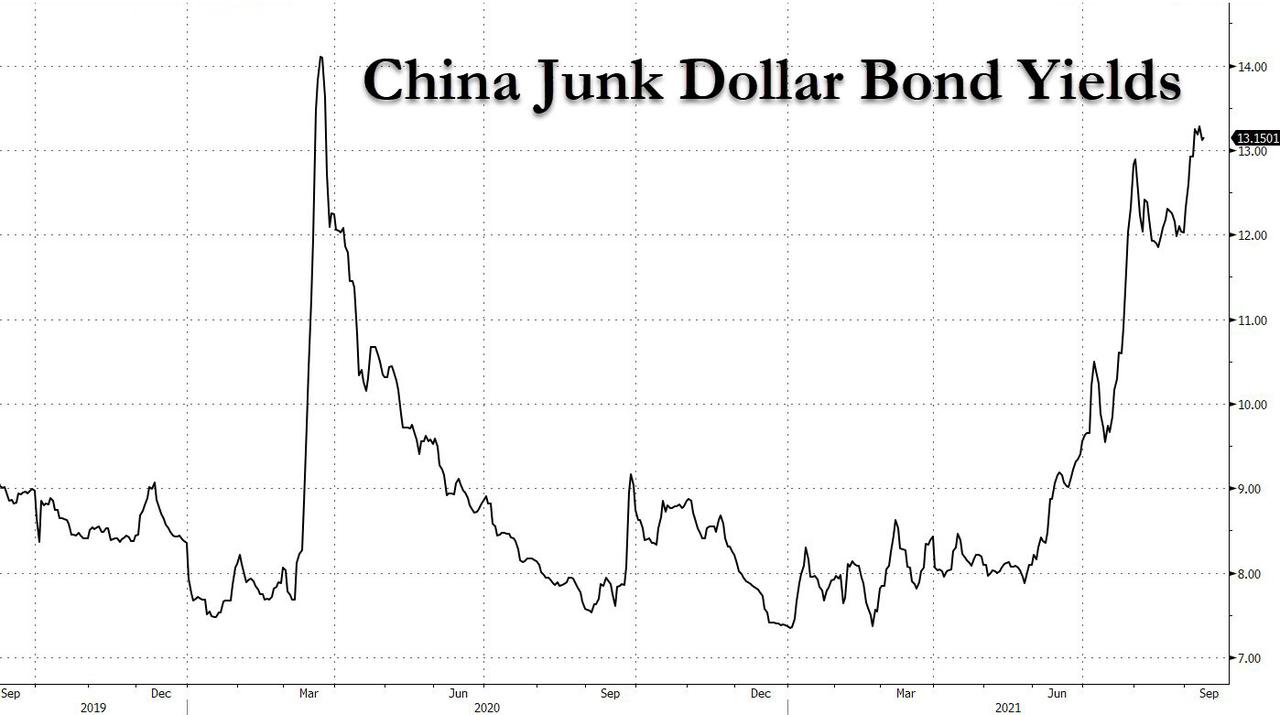

Adding to the pain, contagion concerns from Evergrande is making it more difficult for Chinese developers to refinance, despite a “critical” need to do so, according to Citigroup. Bond issuance is trickier onshore due to lower demand, and offshore due to increasing costs, they wrote in a Wednesday note. As we showed earlier this week, yields on China’s high-yield dollar have exploded rose to 13.7%, the highest since last year’s March market meltdown.

Finally, always last to the party, the rating agencies chimed in, with Fitch saying that smaller banks exposed to Evergrande or other weaker developers may face “significant” increases in non-performing loans in the event of a default, while S&P downgraded Evergrande deeper into junk, saying the developer’s liquidity and funding access “are shrinking severely.”

Tyler Durden

Wed, 09/15/2021 – 22:20![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com