Futures Rebound As Energy Prices Soar

US equity futures and European markets rebounded from a tech rout on Monday that was triggered by fears of soaring energy costs, stagflation, tech overvaluation and escalating Chinese property distress even as Asian shares tracked Monday’s broad Wall Street sell-off to weaken for a third straight session. The dollar rose and yields rebounded back ato 1.50% as the rise in oil continued, pushing Brent above $82/bbl. At of 7:15am ET, S&P futures were up 16.25 points, or 0.38%, to 4,307; Dow futs were up 116 points and Nasdaq futures rose 47.25 points as technology shares bounced in Europe. Bitcoin jumped above $50,000 for the first time since Sept 7.

The “market correction, initially sparked by tapering expectations and China’s property sector worries, is now being driven by record energy prices as well as lingering political uncertainties in the U.S. about the crucial question of the debt ceiling,” said Pierre Veyret, a technical analyst at ActivTrades. “Markets are likely to stay volatile this week and with no clear direction until there is significant progress on the existing concerns.”

Additionally, the recent calm in global markets which hit an all time high as recently as a few weeks ago, has been shattered by a growing wall of worry spanning a debt crisis in China, elevated inflation on the back of commodity supply shocks, fading economic recovery and U.S. political bickering. Meanwhile, investors brace for a tapering of stimulus by the Federal Reserve.

Nerves eased on Tuesday, however, led by a tech rebound following Monday’s Facebook-led rout, and big bank stocks were higher in premarket trading as 10-year Treasury yields climbed to about 1.5% led again by breakevens as oil not only held onto recent impressive gains – along with most other commodities after a gauge of commodities soared to an all-time record – but Brent rose above $82 .

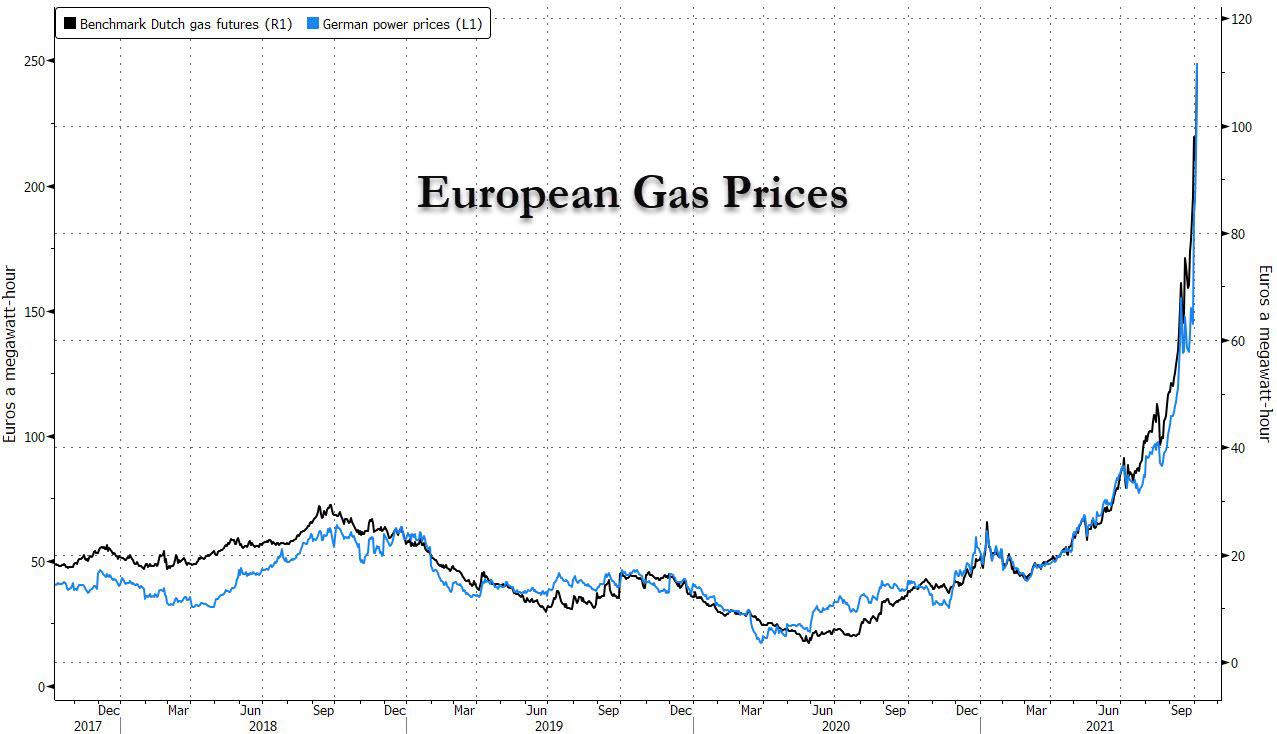

As to the insanity in Europe’s gas sector, European natural gas contracts soared on Tuesday to an unprecedented 111.70 euros per megawatt-hour, compared with 15.49 euros in February. The continent is bracing for a winter crunch in energy supply, with German front-month power contracts also jumping to record levels.

Global shortages of gas and coal are pushing energy prices higher, disrupting markets from the U.K. to China, as economies emerge from the pandemic. Surging costs are threatening to raise inflation and starting to weigh onindustrial production, with some companies in Europe forced to cut output. “The fiercely nervous sentiment on the market continues due to fears of reduced supply during the winter,” trader Energi Danmark wrote in a note Tuesday. “Everything looks set for another week of price climbs.”

In U.S. premarket trading, Facebook found dip buyers in premarket trading after a 4.9% plunge on Monday amid an hours-long service disruption. The stock added 1.6% in the early New York session. Lordstown Motors shares declined as much as 4.6% after the electric vehicle automaker was downgraded to underweight by Morgan Stanley, while the PT was also cut to $2 from $8. Uphealth fell after pricing its share offering at a discount. And Facebook was up 1.5% following Monday’s slump after it blamed a global service outage that kept its social media apps offline for much of yesterday on a problem with its network configuration. Here are some other notable premarket movers:

- Amplify Energy (AMPY US) rises 10% in U.S. premarket trading, paring some of Monday’s 44% plunge tied to an oil spill from a California offshore pipeline operated by the company

- Comtech Telecom (CMTL US) slid more than 7% Monday postmarket after it reported adjusted earnings below average analyst estimates

It is “the period of a multiplicity of shocks percolating through the financial markets leaving them in the fog, with many watching from the sidelines for clarity,” Sebastien Galy, a senior macro strategist at Nordea Invetsment, wrote in a note.

The technology subgroup in Europe’s benchmark Stoxx 600 advanced for the first time in eight days. European natural-gas contracts jumped as much as 16% and West Texas Intermediate crude headed for a seven-year high.

Earlier in the session, MSCI’s broadest index of Asia-Pacific shares outside Japan dropped as much as 1.3%, declining for a third consecutive session. Japan stocks were down 2.5%, South Korea gave up 2% and Australia shed 0.4%. The drop in markets took MSCI’s main benchmark to 619.77, the lowest since November 2020 but it pared losses to be down 0.6% in late Asia trade. The index has shed more than 5% this year, with Hong Kong and Japanese markets among the big losers.

“Investors are clearly worried about inflation due to supply chain disruptions and the rally in energy prices,” said Vasu Menon, executive director of investment strategy at OCBC Bank. “We have seen tech stocks outperform value stocks, so if inflation remains a worry, then tech stocks tend to get hit,” Menon said.

In rates, Treasuries were under pressure with yields near session highs, cheaper by up to 2.5bp across belly of the curve. Yields rose not only on the continued surge in commodities, but about the total chaos over the debt ceiling D-Date which will be hit in two weeks. Gilts lag amid bond auctions, adding to upside pressure on yields, while S&P 500 futures pare about a third of Monday’s 1.3% slide. The RBA kept monetary policy unchanged as expected.

In FX, the dollar rose against most Group-of-10 currencies near a one-year high versus major peers ahead of key U.S. payrolls data due at the end of the week; the pound bucked the trend, advancing for a fourth session. The euro fell 0.25% to $1.1592, while the yen rose 0.29% to $111.18. Leveraged funds sold the kiwi aggressively after a New Zealand business survey showed weak third-quarter economic sentiment. Sentiment on the euro over the next year reached its most bearish since June 2020 on Friday amid a widening policy divergence between the Federal Reserve and the European Central Bank.

In commodities, oil prices reached a three-year high on Monday (and continued higher on Tuesday) after OPEC+ confirmed it would stick to its current output policy as demand for petroleum products rebounds, despite pressure from some countries for a bigger boost to production. Underscoring the rise in commodity prices, the Refinitiv/CoreCommodity CRB index rose to 233.08 on Monday, the highest in more than six years. U.S. oil rose 1.15% to $78.51 a barrel, a day after hitting its highest since 2014. Brent crude stood at $82.2 after rising to a three-year top. Gold prices eased to $1,757 per ounce, after rising on Monday to the highest since Sept. 23.

“OPEC+ may inadvertently cause oil prices to surge even higher, adding to an energy crisis that primarily reflects very tight gas and coal markets,” said Commonwealth Bank of Australia’s commodities analyst Vivek Dhar. “That potentially threatens the global economic recovery, just as global oil demand growth is picking up as economies re‑open on the back of rising vaccination rates,” Dhar said in a note.

Traders are now turning their attention to Friday’s nonfarm-payrolls data to gauge the timing of the Fed’s taper. In the latest Fed comments, St. Louis President James Bullard said elevated price pressures may be changing the mentality of businesses and consumers by making them more accustomed to higher inflation. Australia’s central bank kept its monetary settings unchanged.

Looking at the day ahead now, the main data highlight will be the services and composite PMIs for September from around the world. We’ll also get the Euro Area PPI reading for August, and from the US there’s the August trade balance and the September ISM Services index. Otherwise, central bank speakers include ECB President Lagarde, the ECB’s Holzmann, and the Fed’s Quarles.

Market Snapshot

- S&P 500 futures up 0.2% to 4,301.00

- STOXX Europe 600 up 0.4% to 452.37

- MXAP down 0.7% to 192.58

- MXAPJ down 0.3% to 626.41

- Nikkei down 2.2% to 27,822.12

- Topix down 1.3% to 1,947.75

- Hang Seng Index up 0.3% to 24,104.15

- Shanghai Composite up 0.9% to 3,568.17

- Sensex up 0.4% to 59,531.35

- Australia S&P/ASX 200 down 0.4% to 7,248.36

- Kospi down 1.9% to 2,962.17

- Brent Futures up 0.7% to $81.86/bbl

- Gold spot down 0.6% to $1,758.11

- U.S. Dollar Index up 0.15% to 93.92

- German 10Y yield fell 1.2 bps to -0.225%

- Euro down 0.2% to $1.1603

Top Overnight News from Bloomberg

- China’s heavily leveraged property firms saw their stocks and bonds tumble after a failure by developer Fantasia Holdings Group Co. to repay notes deepened investor concerns about the sector’s outlook

- A steep surge in inflation in the euro area has started to take its toll on the economy, according to a survey by IHS Markit

- China will strictly prevent bank and insurance funds from being used in speculating commodities in a push to maintain market order and stabilize prices

- The Federal Reserve said that its internal watchdog plans to open an investigation into trading activity by senior U.S. central bank officials, following revelations about transactions in 2020

- Facebook Inc. blamed a global service outage that kept its social media apps offline for much of Monday on a problem with its network configuration, adding that it found no evidence that user data was compromised during the downtime

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were pressured following the tech sell-off in the US and amid several headwinds for global markets including US-China trade frictions, China’s record incursion into Taiwanese airspace and with higher oil prices stoking inflationary concerns. ASX 200 (-0.6%) was dragged lower after the losses in tech rolled over into the region and following somewhat mixed Trade and PMI data releases, but with downside stemmed by resilience in gold miners and the energy sector, after gains in the underlying commodity prices including the rally in oil to a seven-year high. Nikkei 225 (-2.2%) slumped below the 28k level and briefly entered into correction territory as it suffered intraday losses of as much as 3% and with index heavyweights Fast Retailing and SoftBank dominating the list of worst performers, while KOSPI (-1.9%) also fell into a correction with the index at least 10% below the record highs registered earlier this year despite efforts by South Korea’s antitrust regulator to dispel fears of a harsh tech crackdown. Hang Seng (+0.3%) was pressured at the open amid tech woes and default fears after reports that Fantasia Holdings missed payments due yesterday for USD 206mln of bonds, although the Hong Kong benchmark then pared its losses with notable strength seen in Chinese oil majors as they benefit from the rising energy prices. Finally, 10yr JGBs were initially kept afloat by the risk aversion but then reversed course amid the uninspired mood in T-notes and Bund futures, as well as weaker metrics from the 10yr JGB auction which attracted a lower bid to cover despite a decline in accepted prices.

Top Asian News

- Gold Drops After Three-Day Gain as Yields and Dollar Push Higher

- ‘Kishida Shock’ Hits Japan Markets Wary of Redistribution Plan

- China Orders Banks to Ramp Up Funding to Boost Coal Output

- S.Korea’s NPS Could Lose $3.5m From Evergrande Stock Investment

European equities (Euro Stoxx 50 +0.9%; Stoxx 600 +0.7%) have extended on the marginal gains seen at the open as indices attempt to claw back some of yesterday’s losses. Incremental macro newsflow since the close has not provided much cause for optimism and therefore it remains to be seen how durable any recovery will be. Overnight, the APAC session was mostly downbeat as the region contended with the negative US lead, ongoing US-China trade frictions, China’s record incursion into Taiwanese airspace and higher oil prices stoking inflationary concern. Final PMIs for the Eurozone saw the composite revised very modestly higher to 56.02 from 56.1 with IHS Markit noting “the current economic situation in the eurozone is an unwelcome mix of rising price pressures but slower growth”. Stateside, futures are exhibiting gains of a similar magnitude to their European counterparts with the ES +0.2% and no real discernible theme across the US majors as traders await further progress in Washington. Sectors in Europe are mostly higher with clear outperformance in banking names with JP Morgan bullish on the sector; Credit Agricole sits at the top of the CAC after launching a new EUR 500mln share repurchase scheme. To the downside, laggards include Construction & Materials and Autos. Individual movers include Greggs (+8.7%) at the top of the Stoxx 600 after raising its profit outlook for the FY despite concerns over supply chain disruptions and staffing issues. Elsewhere, Infineon (+2.8%) has provided some support for the IT sector after confirming its FY 21 forecasts and being confident about the FY22 outlook. Finally, Melrose (-2.2%) is a notable laggard after the Co. cautioned on the fallout of the global chip shortage which has prompted a surge in client cancellations.

Top European News

- European Banks Have Upside on Capital Returns, Yields, JPM Says

- Romania Edges Toward First Rate Hike Since 2018: Decision Guide

- Romania Approves Partial Compensation for Higher Energy Costs

- Morgan Stanley Expands Diversity-Focused ‘Shark Tank’ to Europe

In FX, the broader Dollar and index remain firmer on the session, with the latter on either side of 94.000 from a 93.804 overnight base, but still within yesterday’s 93.675-94.104 range which marks the first immediate points of support/resistance. State-side, US President Biden spoke with 12 progressive members of Congress in which they agreed to follow through on key priorities, while it was also reported that President Biden told House progressives the spending package needs to be between USD 1.9tln-2.2tln. Biden will meet with moderate House Democrats virtually today. It is also worth keeping an eye on the Fed’s review of trading activities which could lead to a shift in the balance between hawks and doves, following the parting of hawks Rosengren (2022 voter) and Kaplan (2023 voter), who were set to be voters during the projected rate hike period. Ahead, the US ISM Services PMI will likely be the focal point from a state-side data standpoint.

- EUR, GBP – The EUR and GBP continue to diverge. Sterling extends on earlier gains, seemingly a function of the EUR/GBP cross topping out just before its 50 DMA (0.8546) before taking out yesterday’s 0.8529 low on its way towards 0.8500. The Sterling strength has helped Cable regain 1.3600+ status from a 1.3585 low. EUR/USD meanders around 1.1600 in a relatively narrow 1.1591-1.1622 current intraday band – with yesterday’s low at 1.1586 ahead of the 200 WMA at 1.1572. Europe saw the release of final Services and Composite PMIs, which continue to highlight the theme of rising prices and spillover into demand.

- AUD, NZD, CAD – he non-US Dollars see mild losses but trade off worst levels as the Dollar recedes and as market sentiment holds an upside bias. The AUD/NZD cross meanwhile remains in focus amid this week’s RBA/RBNZ central bank standoff. The RBA overnight provided no surprises and did not contain any significant new observations, with the currency experiencing choppiness upon the release. The RBNZ, meanwhile, is poised for a 25bps OCR hike at its announcement at 02:00BST/21:00EDT tomorrow. The AUD/NZD cross resides around session lows near 1.0455, whilst OpEx sees some AUD 2.1bln at strike 1.0410. The Loonie sees an underlying bid from crude prices, with USD/CAD back under its 50 DMA at 1.2600 ahead of Canadian trade data.

- JPY, CHF – The traditional havens are at the foot of the G10 bunch in what is seemingly a risk-influenced move. USD/JPY within a tight 110.88-111.25 band vs yesterday’s 110.50-112.07 range. USD/CHF, meanwhile, has popped above its 21 DMA (0.9250) and trades towards the top of its current 0.9238-70 parameter.

In commodities, WTI and Brent front month futures are choppy but ultimately hold an upside bias in the aftermath of the OPEC+ meeting yesterday. Nonetheless, the benchmarks remain near yesterday’s highs which saw Brent Dec test USD 82.00/bbl to the upside. Brent resides around USD 81.50/bbl at the time of writing whilst WTI Nov hovers just under USD 78/bbl. With OPEC out of the way and until the next meeting, traders will be eyeing developments (if any) regarding the Iranian nuclear talks, alongside the electricity situation in China. Furthermore, traders must be cognizant of potential intervention by governments in a bid to control rising energy prices. As a reminder, the White House held talks with Saudi counterparts before the recent OPEC+ meeting and expressed concern on prices. Aside from that, news flow for the complex has been light during the European morning. Elsewhere, precious metals are softer on the day but spot gold and silver trade off worst levels with the yellow metal still holding into USD 1,750/oz-status and spot silver back above USD 22.50/oz. Over to base metals, LME copper remains pressured in what seems to be a continuation of the lacklustre trade seen during APAC hours amid a lack of demand as China remains on holiday.

US Trade Calendar

- 8:30am: Aug. Trade Balance, est. -$70.8b, prior -$70.1b

- 9:45am: Sept. Markit US Composite PMI, prior 54.5

- 9:45am: Sept. Markit US Services PMI, est. 54.4, prior 54.4

- 10am: Sept. ISM Services Index, est. 59.8, prior 61.7

DB’s Jim Reid concludes the overnight wrap

I’m hoping you all survived without WhatsApp, Instagram and Facebook yesterday after the outage. We actually had to resort to a conversation over dinner last night. It was a bit weird without hearing pings go off every few minutes. Once the conversation dried up we went on Twitter and then watched Netflix so it wasn’t a total disaster for US tech in our household. Oh and I’m writing this on my iPad while looking up a few things on Google.

Tech led the sell-off last night that stretched to both equities and bonds. One of the noticeable features of the recent weakness in equities is that bonds have struggled to rally. This hints at technicals being nowhere near as strong as they were in the summer and also a realisation that bonds aren’t a great haven if the sell-off is partly inflation related. By the close of trade yesterday, the S&P 500 had shed another -1.30%, making it the 3rd time in the last 5 sessions that the index has lost more than 1%, with the latest move now taking it -5.21% beneath its all-time closing high back in early September. However, unlike some of the other declines of the last month, which have been quite obviously connected to a particular concern like Evergrande or the impact of higher yields, the latest selloff looks to be coming from a more generalised set of concerns, with those worries given a fresh impetus by yet another rise in energy prices yesterday as oil hit multi-year highs. In turn, that spike in energy prices has led to renewed fears about inflation accelerating even further than current forecasts are implying, with knock-on implications for central banks and the amount of monetary stimulus we can expect over the coming months.

We’ll start with those moves in energy given the effects they had elsewhere. Yesterday saw Brent Crude oil prices (+2.50%) close above $81/bbl for the first time in nearly 3 years, and this morning it’s up another +0.42%. On top of that, WTI (+2.29%) oil prices hit a 6-year high of its own at $77.62/bbl, which saw its YTD gains rise above +60%. The latest advance for oil has come as the OPEC+ group agreed yesterday that they’d stick to their planned output hike of +400k barrels per day in November, in spite of some speculation that there could be a larger increase in supply. However, it wasn’t just oil moving higher, with European natural gas prices (+2.07%) taking another leg up after their recent surge, which leaves them just shy of their recent peak last Thursday. And what’s also concerning from an inflationary standpoint is that the moves in commodities were broader than simply energy, with metals including copper (+1.17%) seeing sizeable gains as well. Overall, that meant Bloomberg’s Commodity Spot Index (+1.12%) finally exceeded its 2011 high yesterday, and brings the index’s gains since the post-pandemic low in March 2020 to +94.7%.

Against this backdrop, equities took another tumble as the major indices on both sides of the Atlantic moved lower, including the S&P 500 (-1.30%) and Europe’s STOXX 600 (-0.47%). Tech stocks saw the brunt of the declines, with the NASDAQ down -2.14% and the FANG+ index down -3.00%, while Europe’s STOXX Technology Index (-2.39%) fell for a 7th consecutive session. Facebook was one of the bigger laggards yesterday as it fell -4.89% – its worst day since November 2020. The company is dealing with whistleblower allegations that their internal research doesn’t match what executives have been saying about the effect the social media company has on its users. The equal weight S&P 500 was only down -0.63% so the big tech stocks definitely led the way. European equities were less affected than their US counterparts however, having missed out on Friday’s late US equity rally following the European close, with the DAX (-0.79%), the CAC 40 (-0.61%) and the FTSE 100 (-0.23%) all seeing declines of less than 1%. A lower tech weighting probably also helped.

Those concerns about stagflation represented further bad news for sovereign bonds yesterday, as investors moved to upgrade their expectations of future inflation. In Europe, 10yr German breakevens were up by +2.0bps to an 8-year high of 1.72%, while their Italian counterparts hit their highest level in over a decade, at 1.63%. Meanwhile in the US, 10yr breakevens were also up +1.3bps to 2.39%. Those moves in inflation expectations supported higher yields, with those on 10yr Treasuries up +1.7bps to 1.479% by the close of trade, as yields on bunds (+1.0bps), OATs (+1.3bps) and BTPs (+1.8bps) similarly moved higher.

Overnight in Asia, equities have mostly followed the US lower, with the Nikkei (-2.77%), KOSPI (-1.71%), and Australia’s ASX 200 (-0.74%) all losing ground, though the Hang Seng (+0.20%) has recovered slightly thanks to energy stocks, and S&P 500 futures (+0.13%) are also pointing to a modest recovery. Those declines for the Nikkei and the KOSPI leave them just shy of a 10% correction from their recent peaks. In terms of the latest on Evergrande, there are signs that risks are spreading to other property developers, as China’s Fantasia Holdings missed a repayment worth $205.7m on a bond that matured Monday. Unsurprisingly, the developments are continuing to affect China’s HY dollar bond prices, with a Bloomberg index now down by -14.3% since its high back in May. Elsewhere in Asia, we got confirmation shortly after we went to press yesterday from new Japanese PM Fumio Kishida that there’d be a general election on October 31. Interestingly, that will actually be the 3rd general election in a G7 economy in the space of just six weeks, following the votes in Canada and Germany in late September.

Back to the US, and Treasury Secretary Yellen’s estimated deadline to raise the debt ceiling – 18 Oct – is now under 2 weeks away, and during a press conference yesterday President Biden called on Republicans to join with Democrats to raise the debt limit, arguing that over a quarter of the US debt was accumulated during the Trump administration and that it should not be tied to “any new spending being considered. It has nothing to do with my plan for infrastructure or building back better, zero.” Senate Majority Leader Schumer plans to hold a vote this week to lift the debt ceiling, though Republicans are set to block the legislation and are forcing Democrats to use the partisan budget reconciliation process that is currently the vehicle of the Biden “Build Back Better” plan.

Whilst time was running out to deal with the debt ceiling, President Biden also met with progressive House Democrats yesterday to discuss the budget reconciliation package and about potentially limiting the scope of the bill that makes up much of the President’s economic agenda. Press Secretary Psaki said that there is a “recognition that this package is going to be smaller than originally proposed,” but that the President is looking to get it across the goal line. Initial estimates could see the final package closer to $2 trillion over 10 years versus the current $3.5 trillion plans.

Meanwhile on trade, the Biden administration also announced yesterday that they would hold direct talks with Chinese officials in the coming week seeking to enforce prior commitments and start fresh talks to exclude some goods from US tariffs. US Trade Representative Katherine Tai will meet with Chinese Vice Premier Liu He, and is expected to focus on how to add and adjust to the Trump administration’s most recent deal with the Chinese government rather than starting from scratch.

There wasn’t much in the way of data yesterday, though US factory orders in August rose by +1.2% (vs. +1.0% expected), and the previous month’s growth was revised up to +0.7% (vs. +0.4% previously).

To the day ahead now, and the main data highlight will be the services and composite PMIs for September from around the world. We’ll also get the Euro Area PPI reading for August, and from the US there’s the August trade balance and the September ISM Services index. Otherwise, central bank speakers include ECB President Lagarde, the ECB’s Holzmann, and the Fed’s Quarles.

Tyler Durden

Tue, 10/05/2021 – 07:45![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com