ECB Already Preparing Next QE To Address “Market Turmoil” When Emergency QE Ends Next Year

The ECB has not even started tapering and it’s already preparing for the next QE.

According to Bloomberg, the European Central Bank is studying a new bond-buying program “to prevent any market turmoil when emergency purchases get phased out next year.” The plan, according to Bloomberg sources, “would both replace the existing crisis tool and complement an older, open-ended quantitative-easing scheme that’s currently acquiring 20 billion euros ($23.1 billion) in debt every month.”

The reason for setting up a brand new QE Such an initiative would act as an insurance measure in case the scheduled end in March of the 1.85 trillion-euro so-called Pandemic Emergency Purchase Program, known as PEPP, prompts a market selloff of bonds from highly indebted countries such as Italy, according to the officials.

The reason for the new QE is simple: once the old “emergency” QE ends and market “turmoil” emerges, the ECB will have to buy even more debt, and this time without capital key limitations. In other words, the ECB is preparing an even bigger bazooka for when the current one runs out of ammo.

Bloomberg confirms as much: under the plan, the source say that purchases would be conducted selectively, which would circumvent the “capital key” rule applying to both of the existing programs that requires central banks to buy debt in relation to the size of each country’s economy. That rule, a legacy since the ECB’s original QE started in 2015, is intended to assuage concerns that the ECB is financing governments, which is something forbidden by law. Which, of course, the ECB is doing.

According to the report, ECB policy makers are trying to smooth the exit from existing emergency stimulus settings while keeping a lid on investor speculation, now that governments are even more exposed after building up debts to fund massive fiscal support. Specifically, they are eyeing the chaos that engulfed Italian debt at the start of the Covid crisis:

Italian debt has led a selloff in European bonds over the last two weeks, with 10-year yields rising around 25 basis points to 0.89%, the highest since June. The same rate on Spanish debt is 0.47%.

ECB President Christine Lagarde and her colleagues have delayed to December an update to the path of monetary stimulus next year. She said in a Bloomberg TV interview in July that the pandemic program could be followed by a “transition into a new format,” without elaborating.

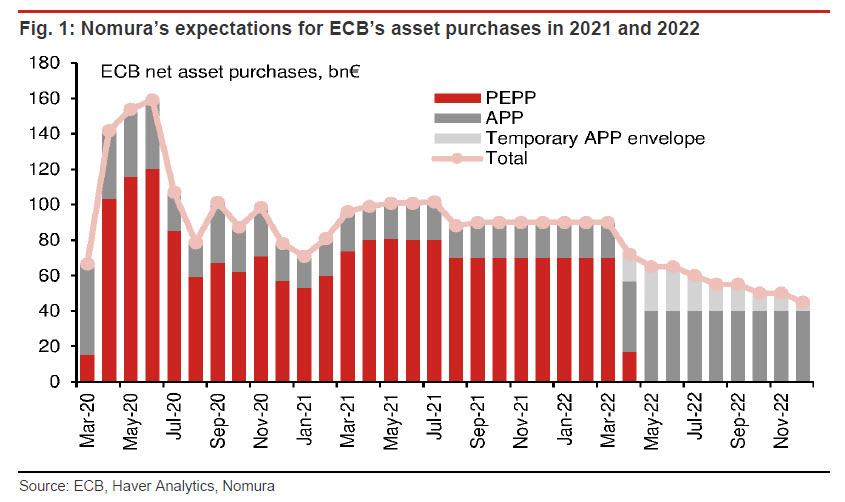

Meanwhile, with the ECB already setting the stage for the next QE, we still have to get to the tapering phase, which as we showed last month will look something like this…. if it ever hits of course.

Tyler Durden

Wed, 10/06/2021 – 15:19![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com