UK Inflation To Hit 7% By… April?

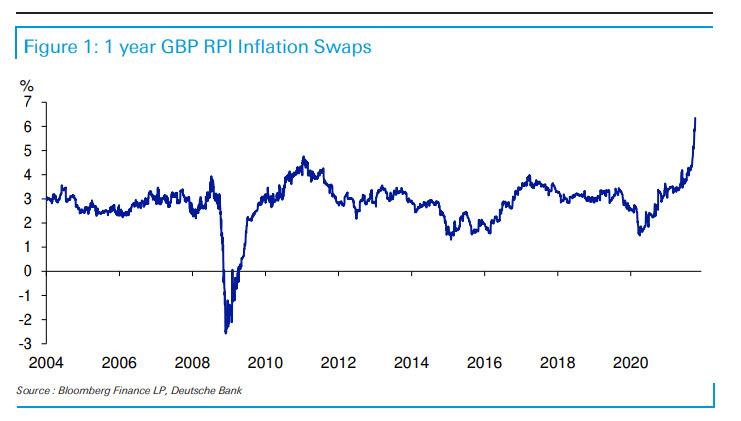

This morning’s most remarkable market observation comes from DB’s chief credit strategist Jim Ried, whose chart of the day shows that the UK may be starting at galloping, runaway inflation of up to 7% as soon as April, the direct result of the insanity taking place in Europe’s energy markets.

Picking up on our obsession with soaring breakevens, this morning Reid points out that the extraordinary moves in natural gas prices have continued to drive global inflation breakevens to multi-year highs, with the stand out feature of the last 24 hours being that index-linked bonds are now implying UK Retail Price Index (RPI) inflation will be 7% in April 2022.

As Reid explains, this is the month the energy regulator Ofgem updates its price cap for utility bills. Typically, the RPI/CPI gap is around 1% but this widens when energy spikes: “Regardless of which inflation gauge is used (and RPI is a flawed measure), it’s fair to say that the cost of living is going up fast. In any case, RPI is used by the UK government to set things like train prices and student loan rates. Some students could in theory be facing 10% interest on their student loans if this continues, 100 times the BoE base rate.”

However, as the Deutsche Banker also notes, “it is likely that the UK government will mitigate a lot of these impacts as many governments around the world are doing for the lower paid in order to offset the rise in energy costs. Expect this to be a recurring theme.”

So going back to Reid’s “Chart of the Day”, it shows the impact that all this has had on 1 year UK RPI swaps. They moved above 6.3% earlier this morning. The 5y, 10y and 5y5y RPI swaps were around c.4.6%, c.4.3% and c.3.95% earlier this morning, which indicates that UK RPI inflation is not necessarily seen as transitory on those metrics.

From a trade perspective, anyone who disagrees with these market forecasts can receive some “pretty big fixed coupons” as long as you’re prepared to pay the eventual realized inflation rate. That said, UK 10 year Gilts at c.1.1% look very unappealing though.

FWIW, DB’s rates strategists recently commented on the apparent inconsistency between nominal and inflation rates: as a reminder since 1971, UK inflation has averaged 5.3%, and only 45 out of 152 countries have averaged less than 5%. So although the last couple of decades have seen much lower inflation than that average, Reid concludes that “it would take a brave person to receive a low fixed income (e.g. government bonds) for any length of time with all the transitory, cyclical and structural inflation in the pipeline.”

Tyler Durden

Thu, 10/07/2021 – 04:15![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com