Stocks That Miss Expectations Are Being Hammered By The Most On Record

It was just a quarter ago (and then again, the quarter before that) when we reported that in a market as priced to perfection as this one, where stock prices have massively outrun fair value based on corporate earnings (in some cases by years, but that’s where super generous earnings multiples come in), that investors have no patience for companies that miss, and the result was a furious hammering of all stocks that missed top or bottom-line expectations (and in many cases, companies that beat but did not beat by enough were also punished).

Well, fast forward to this quarter when the same phenomenon is at play: while earnings are expected to (still) come in hot, the market has a familiar warning to companies: miss and you will get punished.

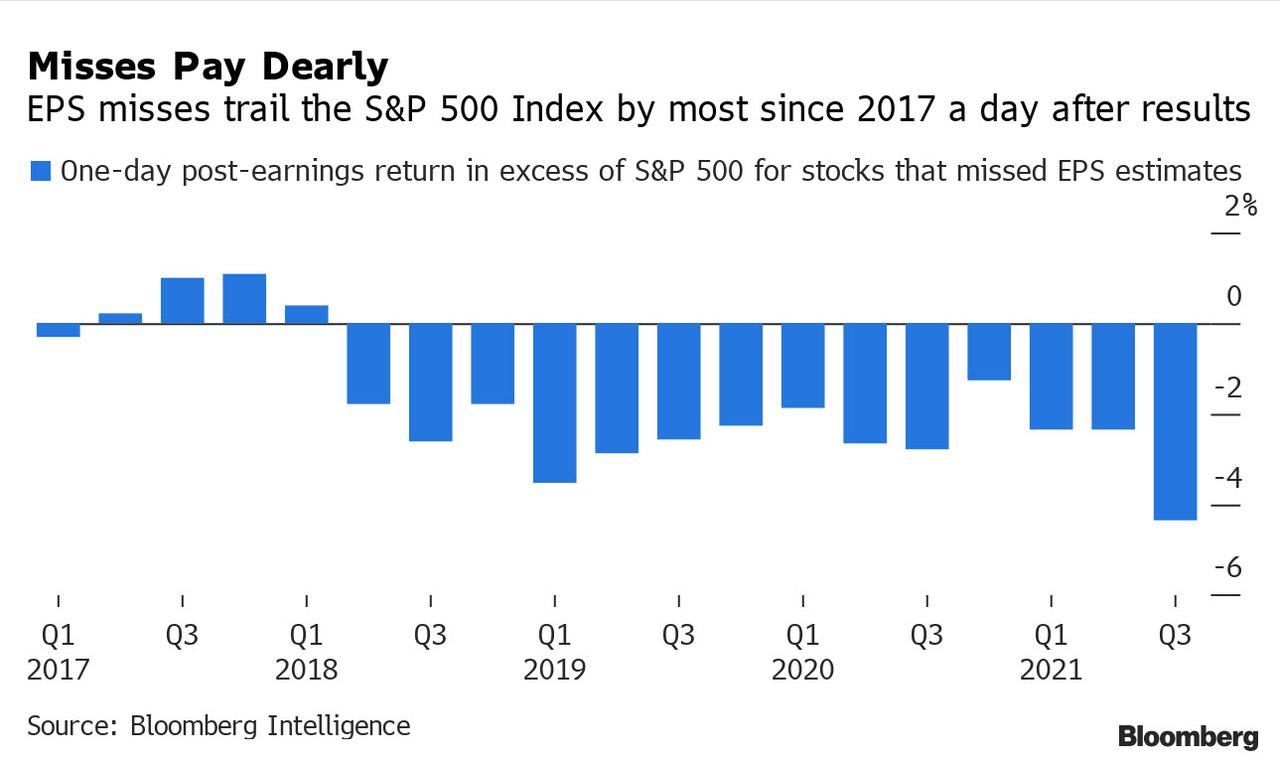

While so far Q3 earnings has come is surprisingly strong – amid whispers that stagflation will hit margins – and 84% of reporting companies have posted earnings that topped expectations, just shy of the best showing ever, similar to last quarter the firms that surpassed profit forecasts got almost nothing to show for it in the market while misses got punished the most since Bloomberg started tracking the data in 2017.

As Bloomberg details looking at recent reports, Procter & Gamble beat on sales and earnings on Tuesday, only to have investors fixate on rising commodity and freight costs. Baker Hughes plunged 5.7% after reporting a third-quarter earnings stumble. And streaming giant Netflix Inc. fell 2.2% on Wednesday as traders looked past a profit and subscriber-growth beat.

On average, companies that beat on profit estimates outperformed the S&P 500 by less than 0.2%.

What about companies that did not beat? Here it was really ugly: shares of firms that missed profit forecasts underperformed the S&P 500 by 4.4% a day after the report, the worst post-earnings reaction since at least 2017, Bloomberg reported.

Combining with our previous observations on this striking phenomenon, this makes Q3 the fourth consecutive quarter in which earnings are not being rewarded and where beats are being severely punished by a market which has been priced to beyond perfection. And while U.S. companies overall have been able to deal with the pandemic-related headaches, analysts want to see whether they can continue to charge more for products without losing business should costs from labor to raw materials continue to go up.

“It is just going to take time to get all those container ships to port and to have enough trucks and truck drivers to take it the last mile to the store shelf or distribution facility,” said Katie Nixon, chief investment officer at Northern Trust Wealth Management. “We hear corroborating evidence from corporate CEOs and, frankly, our own clients — that the current bottlenecks will persist into mid-2022.”

Tyler Durden

Thu, 10/21/2021 – 18:30![]()

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com