The Market Is Signaling That A Scenario Of Sharply Rising Real Rates Is Untenable

By Eric Peters, CIO of One River Asset Management; read this post after first reading “The Most Important Question For The Market Is Identifying The Driver Behind Record Low Negative Real Rates“

Un-Orthodoxy

“Rising inflation and growing government debt may not seem like the natural ingredients to lower longer-term real yields,” explained Marcel, our Head of Research, our investment team thinking through the opportunities that arise when the vast majority of people dismiss perplexing market movements as being illogical when in fact, they may reflect a paradigm shift. “Yet here we are – longer-term real yields set a historic low last week. It is not that the market has given up the idea of orthodoxy. To the contrary, inflation is imposing orthodoxy on people’s behavior. Despite low interest rates, high asset prices, and record job openings, consumers believe it is the worst time to buy a car ever and the least attractive time to purchase a home since 1982. Demand is strong. Supply is constrained. Prices gains are required to ration demand. This is orthodoxy, just not the variety we are accustomed to.”

“But where is the bond market orthodoxy?” asked Marcel. “It is tempting to blame it on the Fed. After all, the Fed has been the dominant buyer of government bonds for the past 18 months, and asset purchases are set to end next June. But the issues are far more dynamic than linear demand-and-supply accounting. Take the last cycle of Fed quantitative tightening. Bank reserves held at the Fed peaked in 2014 with 5y5y real interest rates nearly 2.00%. Those excess reserves were cut in half through 2019 under the direction of policy. With the Fed no longer reinvesting bond maturities, the market had to absorb another $1.3trln of bond supply over that period. And 5y5y real yields collapsed to 0%, despite lower unemployment and substantial fiscal stimulus. Excessive global capital and the thirst for yield had a lot do with those outcomes and they remain strong today.”

“Norway’s central bank cut policy rates rapidly to the zero lower boundary during the pandemic,” continued Marcel. “It was the first developed central bank to reverse course with a rate hike in August. Longer-term yields rose very slightly as rate hikes were brought forward. But mostly, the curve flattened a lot. 30-year swap yields fell below 10-year rates in Norway, to the most inverted on record. Market forces drove Norway terminal rates lower with the earlier rate hike. These patterns are also evident in the UK. The hawkish pivot from the Bank of England did not lead to a bond market risk premium. Instead, before the first-rate hike occurred the market discounted the peak in policy rates in 2023, with an easing cycle thereafter. It is not driven by policy guidance.”

“The market is signaling something much deeper – the scenario of sharply rising real interest rates is untenable. A material rise in real rates risks a severe, negative impact on broader risk assets. The bond market is telling us this would just bring a rush of capital back to low-risk government bonds. The bigger problem is that fiscal policy sees it as an opportunity. Negative real interest rates are being treated as an invitation to expand mandates and increase spending policies. The orthodoxy that is overwhelming the consumer is not even close to being on the radar of policy officials. The intersection of longer-term fiscal trends and the history of excessive debt remind us that policy orthodoxy is really the only answer in the end. It also predicts a very long period of negative real interest rates.”

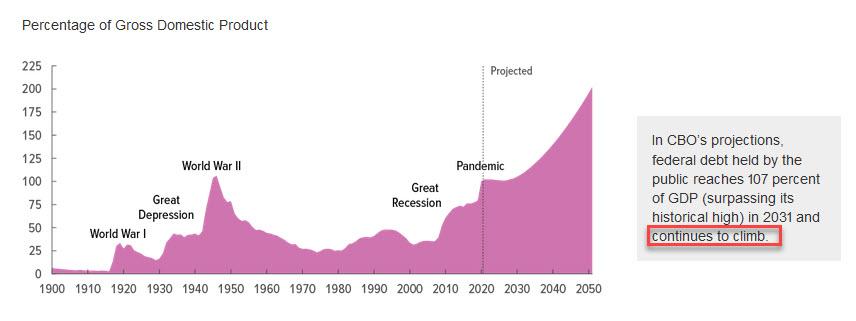

“The US Congressional Budget Office runs a longer-term projection based on current policy, which includes a gentle normalization in real government bond yields. On those projections, Federal debt is more than 200% of GDP in 2051 with an annual budget deficit of 13% of GDP and rising.

The debt interest expense, at 9% of GDP, is substantially greater than spending on social security and Medicare. It is not a plausible outcome. Spending will have to be slower and interest expenses lower. The history of fiscal cycles since 1875, documented by the IMF in 2012, provides the same lesson. How did countries absolve themselves of high government debt? A mix of financial repression and fiscal austerity. Governments used their ‘inflation dividend’ to run budgetary surpluses and real interest rates stayed negative for decades. Austerity comes before higher real rates, not after, and that isn’t near today’s policy deliberations. Get used to negative real rates. It’s normal.”

Tyler Durden

Mon, 11/15/2021 – 08:23

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com