Investors Most Overweight US Stocks Since 2013 Despite Dismal Growth Outlook: Fund Manager Survey

A “startling divergence” emerged last month when Bank of America held its latest Fund Manager Survey: according to the poll results, Wall Street professionals were the least bullish since Oct’20 as growth expectations turned negative for the first time since April 2020 on inflation and China pessimism. And yet, despite this economic gloom and doom, which pushed the self-reported allocation to bonds to an all-time low – on expectations of a stagflationary spike in rates – the allocation to stocks was just shy of all time highs!

Fast forward to today when in Michael Hartnett’s latest Fund Manager Survey, which polled 388 panelists with $1.2 trillion in AUM participated, the Bank of America Chief Investment Strategist found that the mood has brightened a bit as the respondents are slightly “more constructive” (cash allocation dropped to 4.4% from 4.7%) than in the “bearish” Oct survey. The slight improvement in sentiment has left clients ending 20‘21 extremely “risk-on” via the biggest Overweight of US stocks since Aug’13, convinced inflation is transitory, and expecting the Fed to remain well behind the curve.

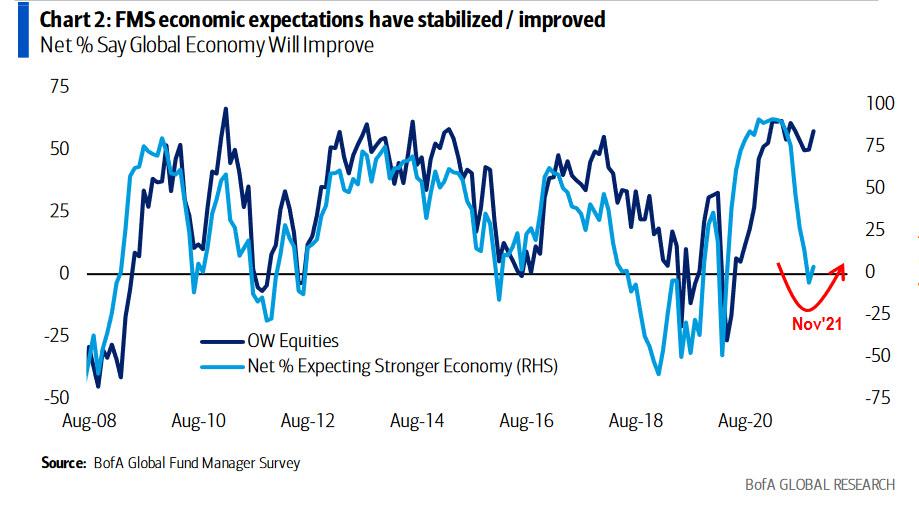

Yet while there may be a tiny improvement in sentiment, the near-record divergence remains: as the chart below shows, while global growth expectations have stabilized /improved to net 3% in Nov’21 (from -6% last month, and still a far cry from the 91% peak in Mar’21) equity levels remain highly elevated at net 52%, a number historically correlated with macro expectations.

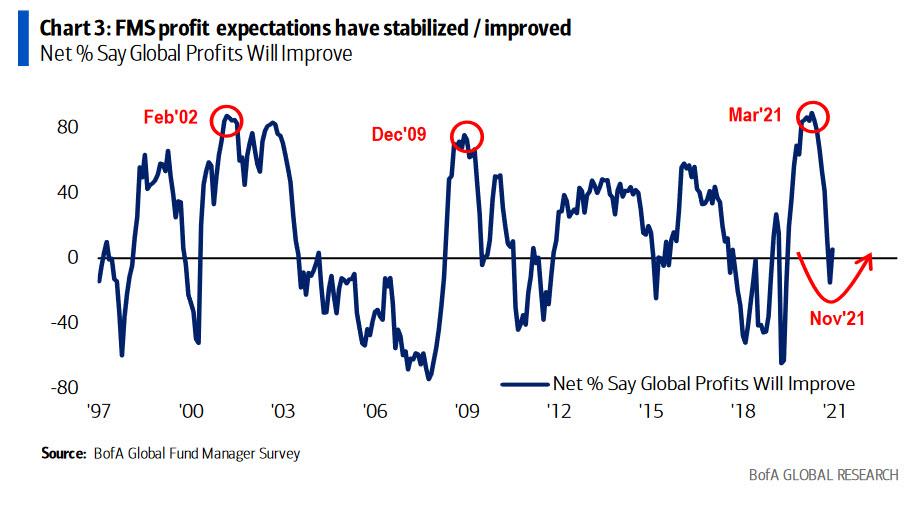

There was also an improvement in global profit expectations to net 6% in Nov’21 (from net-15% last month) off the back of a strong 3Q earnings season. This too is a long way off from the recent top of a 89% peak in Mar’21.

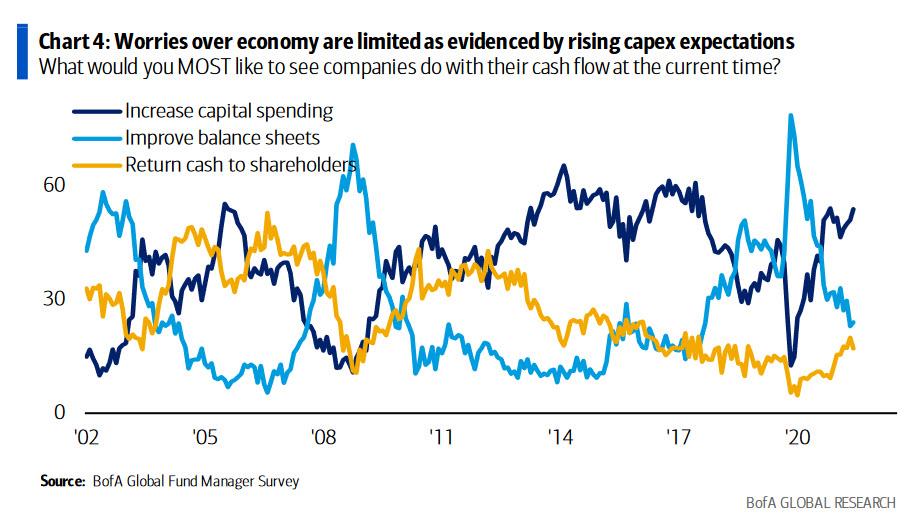

Another indicator of a positive turn in sentiment: the number of investors that want companies to invest their cash flow into capex is a net 54%, close to a 4 year high, and more than the number hoping for balance sheet improvement (24%) and a return of cash to shareholders (17%).

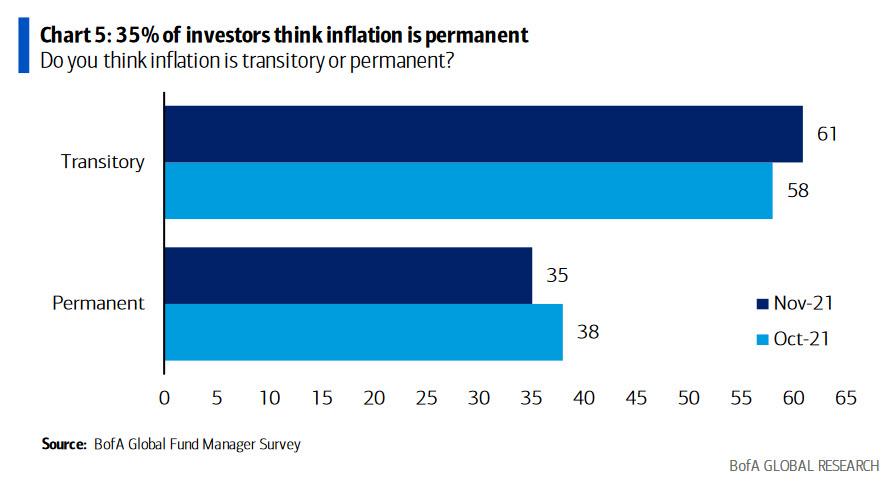

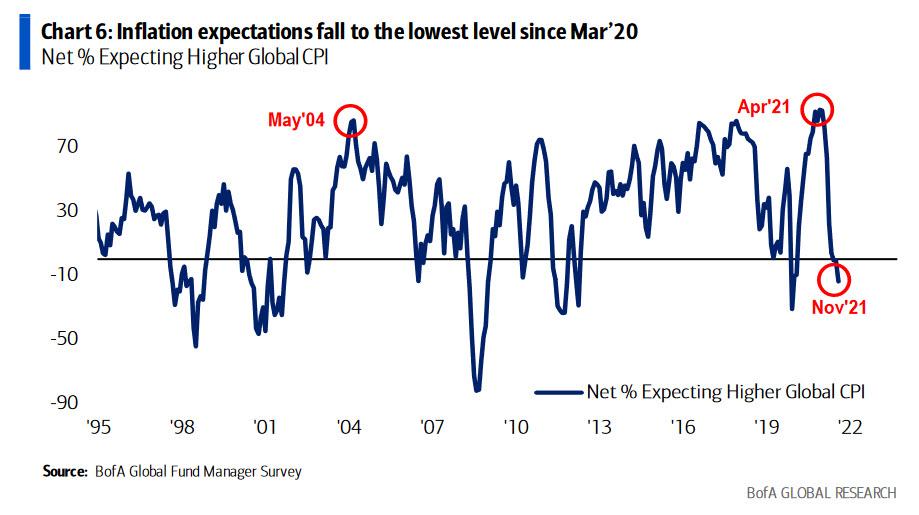

As we have previously discussed, if there is one thing the FMS survey respondents are good at, it is goalseeking a narrative that fits in with their worldview and in the latest FMS we had an example of that with the majority of investors expecting lower inflation despite even the Fed now conceding that that is no longer the case. As the next chart shows, despite worse-than-expected US October inflation data, a majority of FMS investors acknowledge that inflation is a risk but only 35% think it is permanent while 61% think it is transitory…

…while a net 14% of investors now expect global inflation will be lower, the lowest level since the onslaught of COVID-19 in Mar’20. In other words, 51% of investors expect lower inflation while 37% expect higher inflation

This, of course, is a critical variance that is required to justify the overweight outlook on stocks: if inflation expectations were indeed permanent then no amount of mental gymnastics would allow the “financial professionals” to remain as invested in stocks as they are currently. That’s why it is imperative to maintain the fiction that inflation – currently the highest in 30 years – will not persist as the alternative will mean an aggressive tightening cycle that will force everyone to dump their risk exposure.

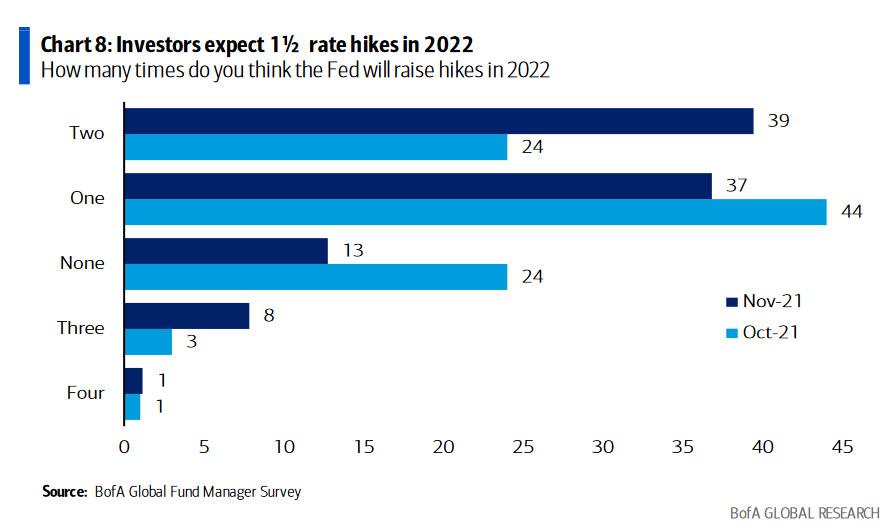

It’s also why FMS investors are now on average expecting 1.5 Fed hikes in 2022 (up from 1.1 last month) but an overall truncated cycle, similar to what we had in 2018. More than that – 39% of investors expect 2 hikes, while 37% expect 1, and 13% expect none. 8 out of 10 investors think the Fed will tighten by 1H23 with the average expectation now for Oct’22. But the punchline is that investors are not expecting the Fed to tighten aggressively (i.e. buy-in for Powell narrative on transitory inflation and modest tapering) because, as noted above, this would ruin the fiction of transitory inflation.

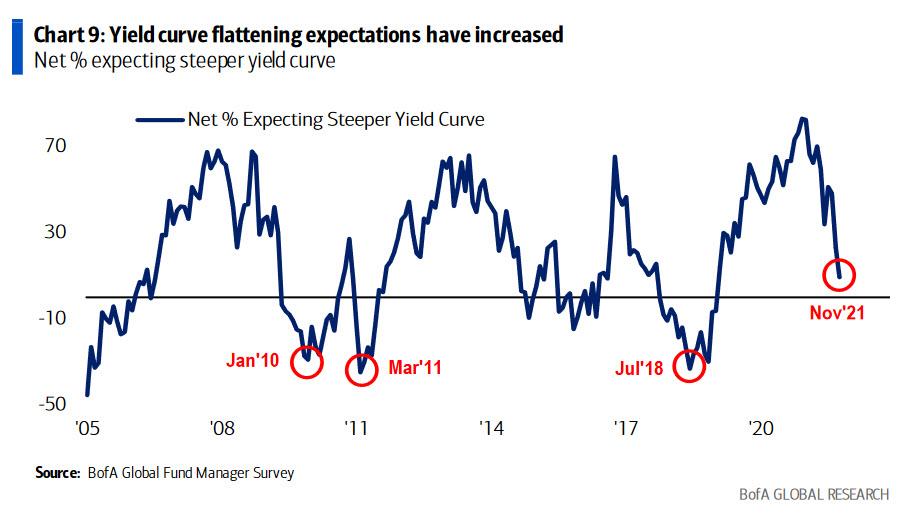

And since most do not believe inflation is permanent, YC flattening expectations have continued to increase. The net % of investors that now expect a steeper yield curve has fallen drastically to now 9%, the lowest level since Feb’19, with rising long-end expectations coming in at net 64% (down from 74%).

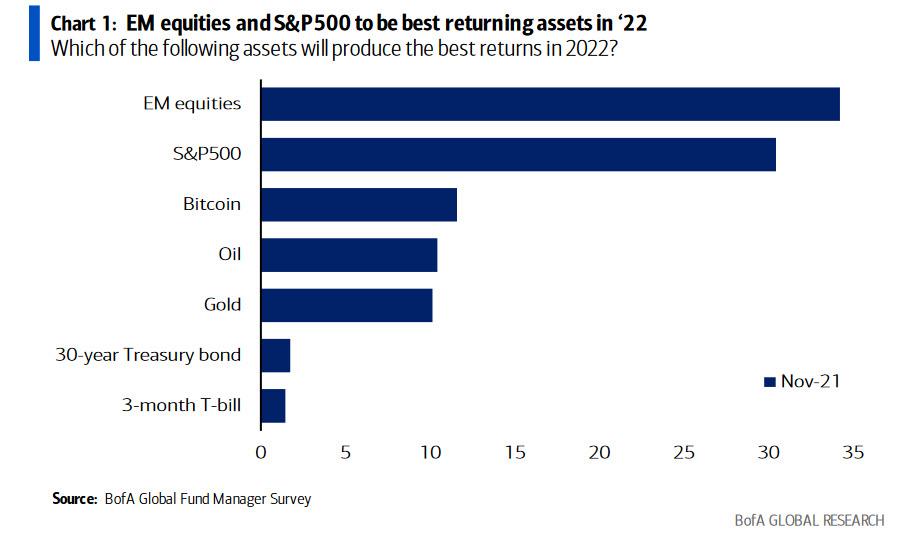

Some other findings from the latest FMC: curiously, or perhaps due to the recent turmoil in China, respondents say EM equities are tipped to be the asset class with the best returns in 2022 by 34% of respondents, followed by S&P 500 (30%), Bitcoin (12%), oil (10%) and gold (10%).

It’s also why Hartnett believes that the FMS Contrarian Trades are playing off survey extremes contrarians would be “long bonds-short stocks,” “long cash, short commodities,” “long EM, short US,” “long utilities, short banks.”

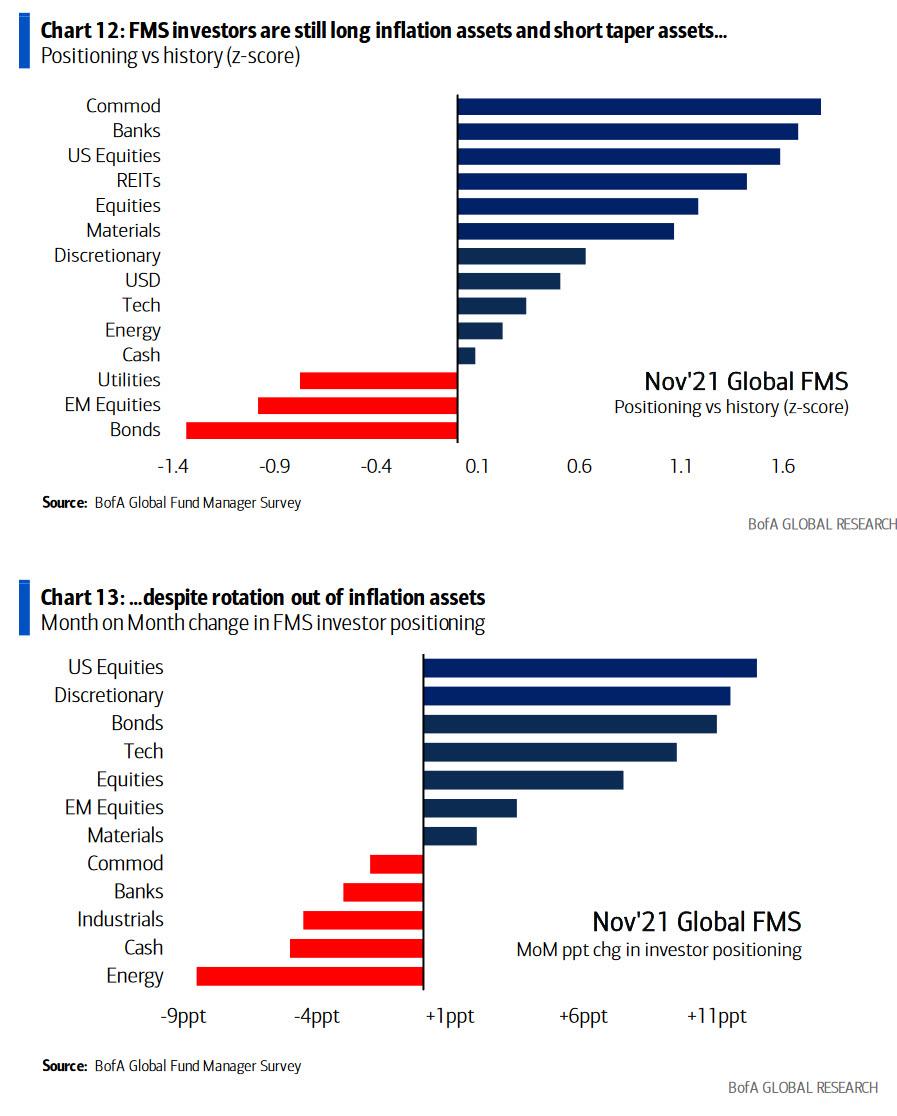

Going back to the survey, many see rotation from cash to U.S. stocks, as well as rotation from energy, industrials and banks to discretionary and tech.

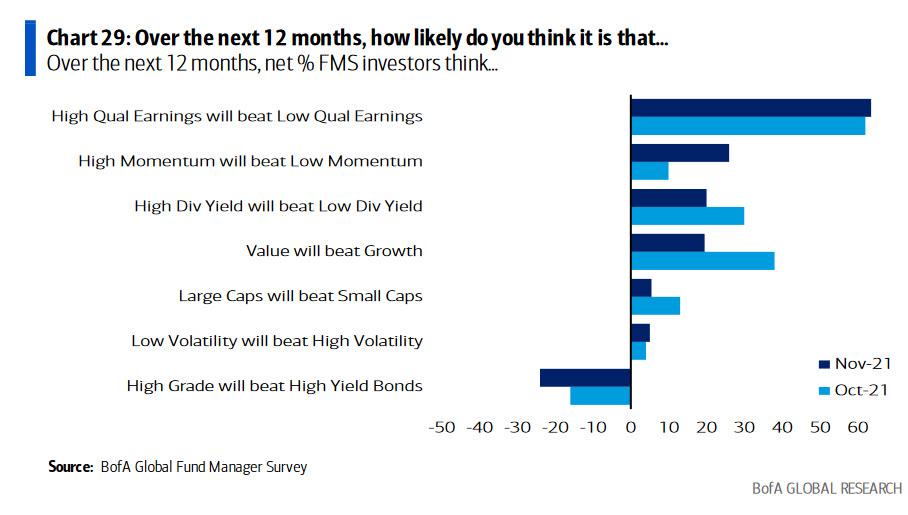

Investors reduced value vs. growth exposure, and increased momentum vs. quality exposure.

Note investors are “very long” equities, particular EU and U.S., as well as banks and tech, while they shun bonds, defensives (utilities, staples), and EM. Looking over the next 12 months, net 26% expect high momentum will beat low momentum, up 16ppt MoM and highest since Jun’21. Net 6% expect large caps will outperform small caps, down 7ppt MoM and lowest since Jun’21. And finally, net 20% expect value will beat growth, down 18ppt MoM.

Amusingly, despite being convinced – or at least so they say – that inflation is only transitory, inflation remains number 1 tail risk for 33% of participants, receding from 48%…

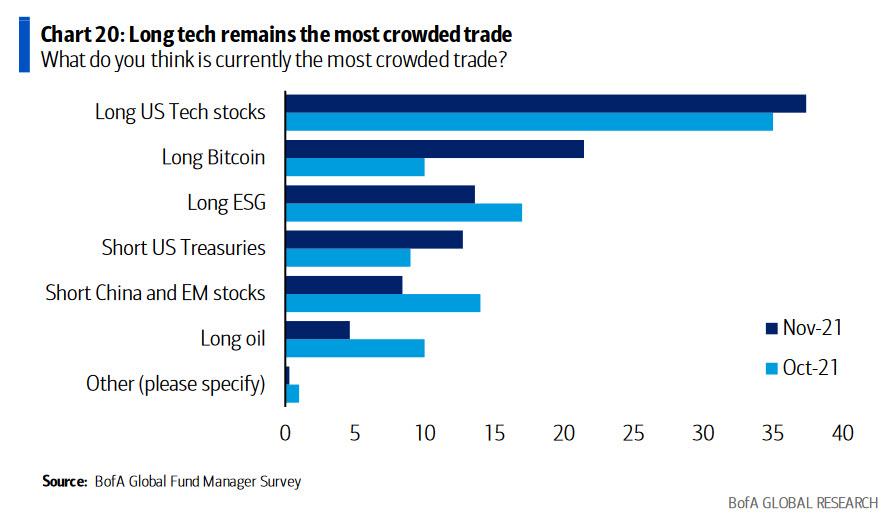

… while long tech, long Bitcoin and long ESG are most crowded trades.

Tyler Durden

Wed, 11/17/2021 – 07:00

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com