Q3 GDP Revised Slightly Higher But Still Misses Expectations

After the preliminary read of Q3 GDP disappointed bigly last month, when it came in at just 2.0%, missing expectations by a mile, moments ago the BEA disappointed data watchers (or what’s left of them today) again when it reported that its first revision of Q3 GDP data was 2.1%, below the 2.2% expected, if slightly better than the 2.0% initial estimate.

Of note, personal consumption rose a 1.7% annualized in 3Q after rising 12.0% prior quarter; this compares to expectations of 1.6%, or for the initial estimate to be unchanged.

Commenting on the data revision, the BEA said that the update reflects upward revisions to consumer spending, inventory investment, and state and local government that were partly offset by downward revisions to exports, business investment, housing investment, and federal government. Imports, which are a subtraction in the calculation of GDP, were revised down.

Here is a more detailed breakdown:

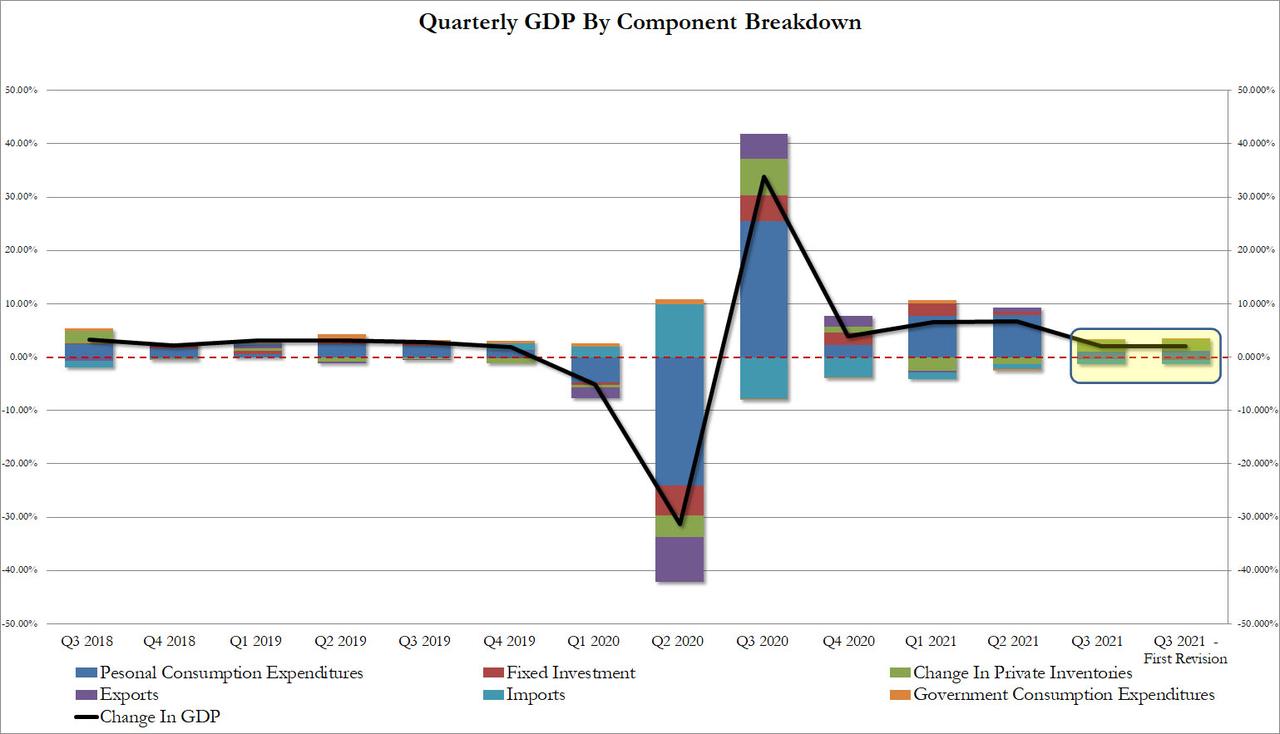

- Personal consumption was revised from 1.09% to 1.18% of the total GDP of 2.11% or just over 50% of the final number.

- Fixed investment subtracted -0.20% from the bottom line number, a deterioration to the initial print of -0.14%

- The change in private inventories added 2.13% according to the latest data, up from 2.07%.

- Net trade (exports less imports) subtracted -1.16% from the bottom line GDP, virtually unchanged from the -1.15% initial print

- Finally, government’s contribution was also flat at 0.16%, unchanged from the 0.14% previously.

Visually:

Drilling further into the data, real disposable personal income – personal income adjusted for taxes and inflation – decreased 4.0% in the third quarter after decreasing 29.1% in the second quarter. Current-dollar DPI increased primarily reflecting an increase in compensation of employees. The increase was partly offset by a decrease in government social benefits related to pandemic relief programs, notably unemployment insurance. Personal saving as a percentage of DPI was 9.6 percent in the third quarter, compared with 10.9 percent (revised) in the second quarter.

On the inflation front, the GDP price index rose 5.9% in 3Q after rising 6.1% prior quarter; this was higher than the 5.7% expected. Meanwhile, Core PCE q/q rose 4.5% in 3Q after rising 6.1% prior quarter; this came in line with expectations.

Finally, looking at corporate profits, the BEA reports that profits increased 4.3% at a quarterly rate in the third quarter after increasing 10.5% in the second quarter. Profits of domestic nonfinancial corporations increased 3.7% after increasing 13.8%. Profits of domestic financial corporations increased 2.5% after increasing 10.9%. Profits from the rest of the world increased 8.7 percent after decreasing 1.3 percent. Corporate profits increased 20.7 percent in the third quarter from one year ago.

Of course, since this data is extremely stale, nobody will care what GDP did in the late summer with all eyes now fixed on Q4 GDP where the Atlanta Fed expects the number to come in above 8%, although we in turn expect this print to drop sharply in the coming weeks.

Tyler Durden

Wed, 11/24/2021 – 08:50

Zero Hedge’s mission is to widen the scope of financial, economic and political information available to the professional investing public, to skeptically examine and, where necessary, attack the flaccid institution that financial journalism has become, to liberate oppressed knowledge, to provide analysis uninhibited by political constraint and to facilitate information’s unending quest for freedom. Visit https://www.zerohedge.com